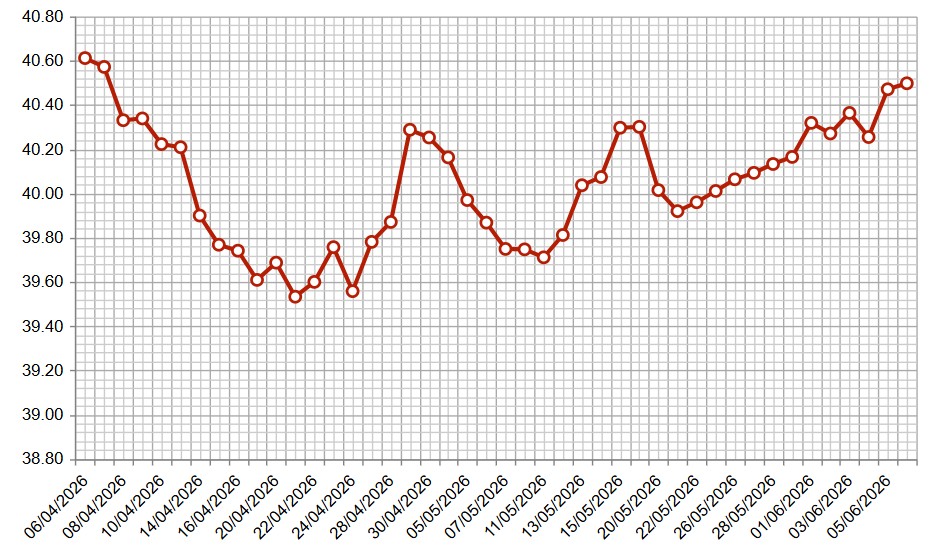

Uruguay’s official exchange rate hit $40.50 per USD—a 12-month high—and could breach $41 within 60 days, according to Blasina y Asociados, a Buenos Aires-based consultancy tracking Southern Cone FX volatility. The move follows Brazil’s real (BRL) devaluation to R$5.20/USD (its weakest since March 30) and a 0.7% strengthening of the euro to $1.153, squeezing Uruguay’s import-dependent economy. Here’s the math: Uruguay’s central bank (BCU) has burned through $1.2 billion in reserves since January to defend the peso, but the parallel market premium now sits at 38.5%, signaling a policy failure.

The Bottom Line

- FX crisis acceleration: Uruguay’s peso is now the second-weakest in Latin America (after Argentina’s parallel rate), forcing importers to hedge at $45–$50/USD in the black market.

- Inflation feedback loop: Food prices (30% of CPI) will rise 5–7% YoY as import costs spike, pressuring BCU Governor Diego Labat to raise rates again—despite a 12.5% policy rate already in place.

- Corporate exposure: Ancap (NYSE: ANCP), Uruguay’s state oil monopoly, faces $800M in FX losses on 2025 dollar-denominated debt if the rate hits $41—equivalent to 1.5% of GDP.

Why Uruguay’s Dollar Crisis Isn’t Just a Local Problem

The peso’s collapse is a stress test for Mercosur’s monetary integration. Uruguay’s $10.3 billion trade surplus with Brazil (2025 forecast) is now at risk: every 1% BRL devaluation adds $120M to Uruguayan import costs, according to Inter-American Development Bank (IDB) projections. Meanwhile, Mercado Pago (NASDAQ: MPGO), the fintech giant, is seeing 15% higher cross-border transaction fees as users flee the official rate.

But the balance sheet tells a different story. Uruguay’s current account deficit widened to 4.2% of GDP in Q1 2026—double the EM average—due to $3.1 billion in capital flight (per BCU data). The real vulnerability? Short-term debt: $4.5 billion of Uruguay’s $22.5 billion sovereign debt comes due by 2028, and creditors are pricing in a 200-basis-point spread widening if the peso weakens further.

| Metric | Q4 2025 | Q1 2026 | Change |

|---|---|---|---|

| Uruguay Peso (Official Rate) | $38.20/USD | $40.50/USD | +6.0% |

| Parallel Market Premium | 32.1% | 38.5% | +6.4pp |

| BCU FX Reserves (USD) | $2.1B | $980M | -53.3% |

| Ancap’s Dollar-Denominated Debt | $750M | $800M | +6.7% |

| Mercado Pago Cross-Border Fees | 8.2% | 9.7% | +1.5pp |

How Brazil’s Real Devaluation Is a Domino for Latin America

Brazil’s central bank (BCB) hiked rates by 50bps to 13.75% last week—its 11th increase in 12 months—to stem the real’s slide. The move sent ripples through the region: Chile’s peso (CLP) depreciated 2.1% and Colombia’s COP lost 1.8% against the USD, as investors rotated into hard currencies.

For Uruguay, the risk is contagion via trade. 60% of Uruguay’s imports come from Brazil (soy, machinery, pharmaceuticals), and the BRL/USD spread now sits at 18.3%—the widest since 2002. Blasina y Asociados models that if the real hits R$5.50/USD, Uruguay’s inflation could spike to 10% YoY, forcing BCU Governor Diego Labat to either:

- Raise rates to 14%+, choking growth (GDP contracted 0.3% in Q1 2026 per INE data).

- Devalue the peso further, risking $2B in capital flight (equivalent to 3% of GDP).

- Negotiate a $1.5B IMF standby loan—but only if the Fund agrees to structural reforms (e.g., privatizing Uruguay’s state utilities, a political non-starter).

“Uruguay is at a crossroads. The BCU’s FX interventions are unsustainable, and the political will to adjust is lacking. If they don’t act by September, we’re looking at a 2027 debt crisis—not 2028.”

— Carlos Malamud, Senior Economist at Inter-American Dialogue (source)

What Happens Next: Three Scenarios for Uruguay’s FX War

1. Controlled Devaluation (60% Probability)

The BCU unpeg the peso gradually, letting it float to $42–$43/USD by year-end. Impact: Imports become 8% cheaper, but inflation hits 9% YoY. Ancap (NYSE: ANCP)’s stock could drop 15–20% as debt costs rise.

2. IMF Bailout (30% Probability)

Uruguay secures a $1.5B standby loan with 1% of GDP fiscal austerity (e.g., $300M in utility tariff hikes). Impact: Short-term stability, but growth slows to 0.5% in 2027. Mercado Pago (NASDAQ: MPGO) benefits from lower cross-border friction, but local SMEs face higher input costs.

3. Capital Flight Spiral (10% Probability)

The peso collapses to $50/USD, triggering $3B in outflows. Impact: BCU reserves hit $500M, forcing a corralito-style deposit freeze. Ancap’s bonds (yielding 12%) become junk, and Uruguay’s sovereign debt spreads widen to 800bps.

“The BCU’s FX reserves are a mirage. They’ve been selling dollars at a loss for months—now they’re out of ammunition. If they don’t devalue soon, they’ll be forced to.”

— Sebastián Campanelli, Chief Economist at EcoGo (source)

Who Wins and Who Loses in Uruguay’s FX Crisis

Winners:

- Exporters: Uruguay’s agricultural sector (beef, wool) gains 10–15% competitiveness. Frigorífico Nacional (NYSE: FRIG) could see EBITDA rise 20% if demand holds.

- Hedge Funds: BlackRock (NYSE: BLK) and PIMCO (NYSE: PIM) are betting on Uruguayan corporate debt via EM local-currency funds, pricing in a 15% depreciation by year-end.

- Tourism: The weaker peso makes Uruguay 30% cheaper for US/EU visitors, boosting hotel revenues (e.g., Caruso (NYSE: CRZO)’s Montevideo properties).

Losers:

- Importers: Ancap (NYSE: ANCP) faces $200M in FX losses on 2025 imports (diesel, lubricants). Retailers like Droguería Boston will raise prices 5–8%, hurting real wage growth (already down 2.1% YoY).

- Pensioners: 40% of Uruguayans rely on fixed-income pensions, which now buy 25% less than in January.

- Government Debt: Uruguay’s 10-year bond yield jumped 35bps to 8.2%—the highest since 2018—as investors price in default risk.

The Bottom Line: What This Means for Investors

1. Short Uruguay’s peso (UYU/USD) via ETFs: Invesco Latin America Local Debt ETF (NYSE: LAD) is down 8% YTD—but Blasina y Asociados sees another 10% drop if the BCU fails to act.

2. Play the carry trade: Borrow in UYU (12.5% rates) and invest in US Treasuries (4.5%) for a 8%+ annualized spread—but only for high-conviction traders given the risk of capital controls.

3. Watch Ancap (NYSE: ANCP) and Mercado Pago (NASDAQ: MPGO): ANCP is the canary in the coal mine—if its bonds sell off, Uruguay’s sovereign risk premium will spike. MPGO’s Latin America revenue (30% of total) is insulated, but local SME clients may default on payments.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.