{kind=link}

South Korea’s Household Debt Climbs to Record High: What You Need to Know

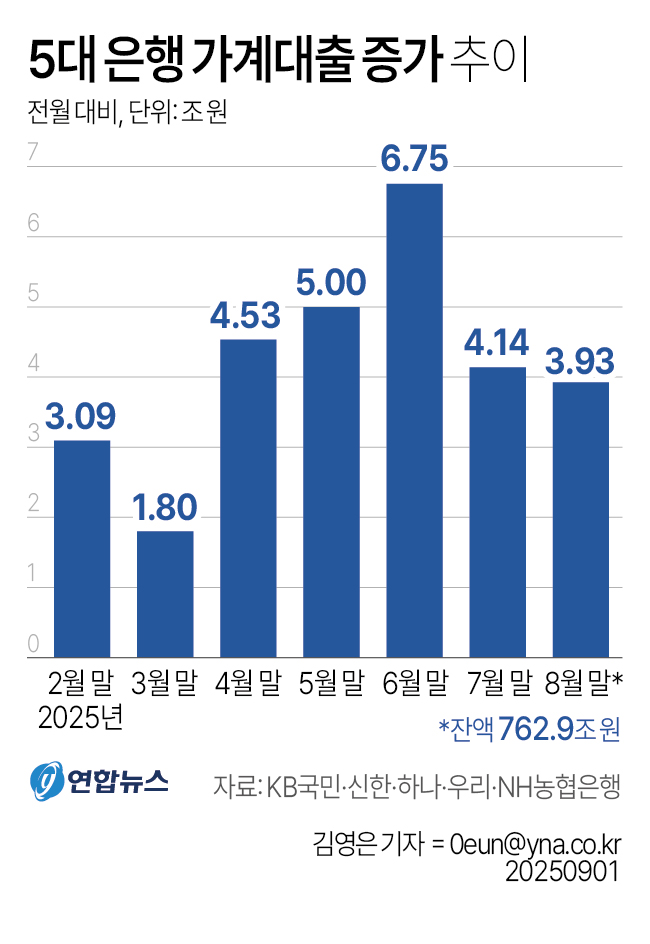

Seoul, South Korea – September 1, 2025 – Breaking news reveals a significant increase in South Korea’s household debt, reaching ₩762.89 trillion (approximately $575 billion USD) as of the end of July. This represents a rise of ₩3.95 trillion from the previous month, raising concerns about financial stability and consumer spending power. This is a developing story, and Archyde is committed to providing up-to-the-minute coverage and insightful analysis.

Image: Placeholder – Illustrative image of South Korean Won currency.

The Numbers: A Deep Dive into the Debt Increase

According to data released by the financial sector and reported by Yonhap News, the combined household loans across the five major banks have surged to a record level. This increase isn’t just a statistical anomaly; it reflects a complex interplay of factors impacting South Korean households. While the exact breakdown across different loan types (mortgages, personal loans, etc.) hasn’t been fully detailed yet, the overall trend is undeniably upward. This news is particularly relevant for those following finance news and economic trends.

Why is Household Debt Rising in South Korea?

Several factors contribute to this growing debt burden. Historically low interest rates, maintained for an extended period to stimulate economic growth, encouraged borrowing. However, with global inflation and rising interest rates becoming a reality, the cost of servicing these debts is increasing, putting a strain on household finances. Furthermore, South Korea’s competitive housing market, characterized by high property prices, has driven up mortgage debt. The cultural emphasis on homeownership also plays a role, with many families prioritizing securing a home even if it means taking on significant debt.

The Broader Economic Implications: What Does This Mean for South Korea?

A high level of household debt can have several negative consequences for the South Korean economy. It can dampen consumer spending, as households allocate more of their income to debt repayment. This, in turn, can slow economic growth. It also increases the vulnerability of the financial system to shocks, such as a sudden rise in interest rates or a downturn in the housing market. The Bank of Korea is closely monitoring the situation and may consider implementing measures to curb excessive borrowing and manage the risks associated with high household debt. Understanding these dynamics is crucial for anyone interested in global markets and investing.

Historical Context: South Korea’s Debt Journey

South Korea’s household debt has been on a generally upward trajectory for the past two decades, fueled by economic growth and changing societal norms. The 1997 Asian Financial Crisis prompted a period of financial reform, but also led to increased borrowing as individuals sought to rebuild their financial security. The global financial crisis of 2008 and the subsequent period of low interest rates further contributed to the rise in household debt. This current surge is occurring against a backdrop of global economic uncertainty, making it particularly concerning.

What Can Consumers Do? Practical Tips for Managing Debt

For South Korean consumers facing increasing debt burdens, several strategies can help. Refinancing existing loans to secure lower interest rates is one option. Budgeting and reducing discretionary spending can free up funds for debt repayment. Seeking financial counseling from reputable organizations can provide personalized advice and support. It’s also important to be aware of government programs designed to assist borrowers in financial difficulty. Archyde will continue to provide resources and information to help consumers navigate these challenging economic times. We are dedicated to providing breaking news and insightful analysis.

The escalating household debt in South Korea is a complex issue with far-reaching implications. As the Bank of Korea and the government grapple with managing this challenge, it’s crucial for consumers to be proactive in managing their finances and for investors to closely monitor the situation. Archyde will remain at the forefront of this story, delivering timely updates and expert analysis to keep you informed.