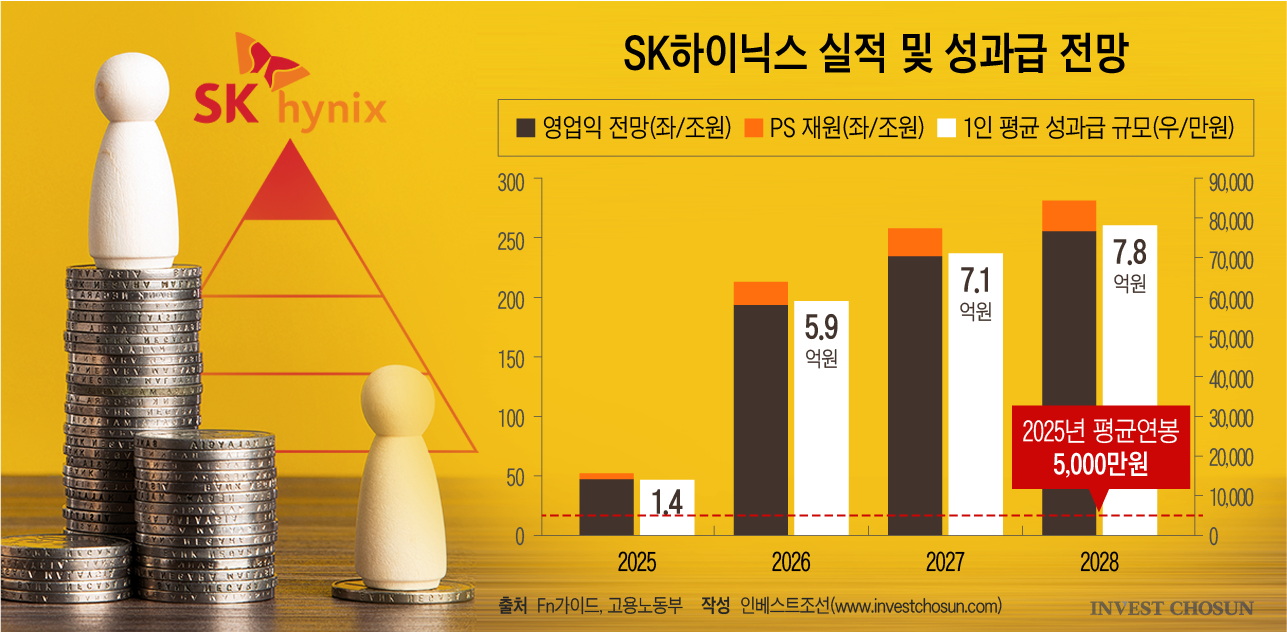

SK hynix (KRX: 000660) is creating a new high-income class in South Korea as projected operating profits of 200 trillion KRW trigger massive profit-sharing (PS) payouts. With a potential 20 trillion KRW pool for 33,000 employees, average annual compensation could reach 1 billion KRW, signaling an unprecedented HBM-driven windfall.

This is not merely a story of corporate generosity; it is a manifestation of the “AI Arms Race.” As the primary supplier of High Bandwidth Memory (HBM) to NVIDIA (NASDAQ: NVDA), SK hynix has transitioned from a cyclical commodity vendor to a critical infrastructure gatekeeper. The resulting capital concentration within its workforce reflects the extreme pricing power currently held by HBM leaders.

The Bottom Line

- HBM Hegemony: Profitability is decoupled from traditional DRAM cycles, driven by the structural demand for AI accelerators.

- Labor Market Distortion: Extreme compensation spikes create a “talent vacuum,” forcing competitors like Samsung Electronics (KRX: 005930) to aggressively hike wages to prevent brain drain.

- Macroeconomic Ripple: A new “super-earner” class is emerging, likely inflating luxury real estate and high-finish consumption in the Icheon and Yongin corridors.

The HBM Premium and the Erosion of the DRAM Cycle

For decades, the semiconductor industry operated on a volatile “boom-bust” cycle. But the generative AI era has rewritten the playbook. Here is the math: HBM3E carries significantly higher margins than standard DDR5 memory due to the complexity of TSV (Through-Silicon Via) stacking and the scarcity of qualified yield.

But the balance sheet tells a different story regarding sustainability. While the 200 trillion KRW operating profit target is staggering, it relies on a persistent demand for AI GPUs. If Microsoft (NASDAQ: MSFT) or Alphabet (NASDAQ: GOOGL) scale back their Capex, the “new income class” could face a sharp correction.

Current market data suggests a massive divergence in valuation between HBM leaders and laggards. While SK hynix captures the upside, the broader memory market remains sensitive to global macroeconomic headwinds and interest rate volatility.

| Metric (Projected/Current) | SK hynix (HBM Focus) | Industry Average (DRAM) | Impact Factor |

|---|---|---|---|

| Operating Profit Target | 200 Trillion KRW | Variable/Cyclical | AI Infrastructure Demand |

| PS Pool Estimate | 20 Trillion KRW | Standard Bonus | High Margin HBM3E |

| Employee Base | ~33,000 | Varies by Firm | Concentrated Wealth |

| Key Client Exposure | NVIDIA | Diversified | Single-point Dependency |

The Strategic Talent War: Samsung vs. SK hynix

This compensation surge creates a critical strategic vulnerability for Samsung Electronics (KRX: 005930). In the semiconductor world, the “yield” is determined by the engineers. When a competitor offers a 1 billion KRW package, the cost of talent retention skyrockets across the entire ecosystem.

We are seeing a shift in the power dynamic. Historically, Samsung was the undisputed prestige employer in Korea. Now, SK hynix is the “growth stock” of the labor market. This forces Samsung to either match these astronomical payouts—compressing their own margins—or risk a systemic loss of their top 1% of engineering talent.

“The semiconductor industry is no longer just about fabrication capacity; it is a war for the few thousand engineers globally who can optimize HBM yields. Compensation is the primary weapon in this attrition war.”

This labor shift is not limited to Korea. It mirrors the “AI talent war” seen in Silicon Valley, where specialized AI researchers command multi-million dollar signing bonuses. The “SK hynix effect” is simply the Korean localized version of this global phenomenon.

Macroeconomic Implications: The ‘HBM Bubble’ or a New Baseline?

When 33,000 individuals suddenly see their income jump to the 1 billion KRW level, the local economy reacts. We expect to see a “wealth effect” that drives inflation in specific sectors. High-end real estate in Gyeonggi province is already reflecting this anticipation.

However, the risk is the “golden handcuff” syndrome. Employees become accustomed to an unsustainable baseline of income. If the AI hype cycle cools or if Intel (NASDAQ: INTC) or AMD (NASDAQ: AMD) successfully diversify their memory sourcing, the profit-sharing pool will evaporate.

From a corporate governance perspective, the decision to distribute 20 trillion KRW in bonuses rather than reinvesting it into R&D or share buybacks is a bold move. It secures loyalty in the short term but increases the fixed cost of labor for the long term. For a deeper look at semiconductor valuations, refer to Wall Street Journal’s tech analysis.

The Trajectory: Beyond the Bonus

As we move through April 2026, the market is watching whether this “new income class” is a temporary spike or a permanent structural shift. The real indicator will be the Q3 guidance. If SK hynix maintains its dominance in the HBM4 transition, the 1 billion KRW salary becomes the new benchmark for the elite technical class.

For investors, the play is clear: watch the Capex of the “Hyperscalers.” As long as the cloud giants are building data centers, the SK hynix engineers will remain the highest-paid laborers in the country. But the moment the ROI on AI infrastructure is questioned, the party ends.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.