Oil Prices Surge to $120 Amid Iran Blockade Fears

The price of Brent crude oil spiked briefly above $120 a barrel today, a level not seen in months, following unconfirmed reports of an expanded naval presence in the Persian ... Read More

Saturday Edition

Stay updated with Archyde – your source for breaking news, global headlines, economy, entertainment, health, technology, and sports. Fresh stories daily.

The price of Brent crude oil spiked briefly above $120 a barrel today, a level not seen in months, following unconfirmed reports of an expanded naval presence in the Persian ... Read More

Continuous Coverage

Françoise Matthey’s newly published “L’Effacée” (The Erased One) resurrects the story of a young Alsatian woman whose life…

The air in Beirut feels thicker these days, not with humidity, but with anticipation. Israel’s rhetoric regarding Lebanon…

Real Madrid narrowly defeated Hapoel Jerusalem 82-79 in the opening game of their EuroLeague playoff series, a match…

Three companies – Uralungal Infrastructure Projects, RDS Projects and SREI Infrastructure Finance – have been shortlisted to demolish…

Chilean television is bracing for a dramatic showdown. This weekend, on Mega’s long-running drama *Reunión de Superados* (RDS),…

The Earth’s Rotation Slowdown: A Complex Interplay of Glacial Melt, Mantle Dynamics, and Human Influence Recent reports from…

Global Affairs

Thousands of Boca Juniors fans have descended upon Brazil ahead of their Copa Libertadores clash with Cruzeiro this…

Markets And Money

Jerome Powell intends to continue serving as a governor on the Federal Reserve Board after his current term…

Digital Culture

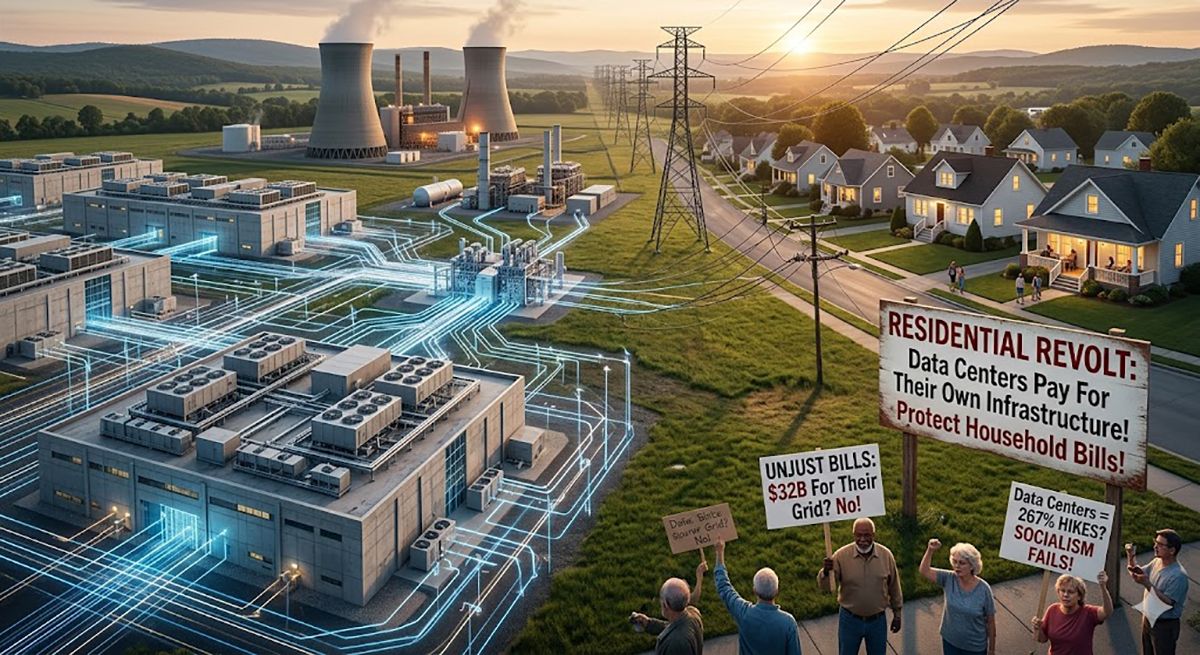

The Power Grid Under Strain: AI Data Centers and the Rising Cost of Electricity Across the United States,…

Science And Wellbeing

Ancient ‘Kraken’ Discoveries Reshape Understanding of Marine Apex Predators Recent paleontological findings, published this week, reveal evidence of…

Screen And Sound

Netflix is poised to dominate May 2026 with a slate of high-profile releases, including the action thriller Extraction…

Fixtures And Form

Max Verstappen’s commitment to Red Bull Racing remains steadfast despite the upcoming departure of his long-time race engineer,…