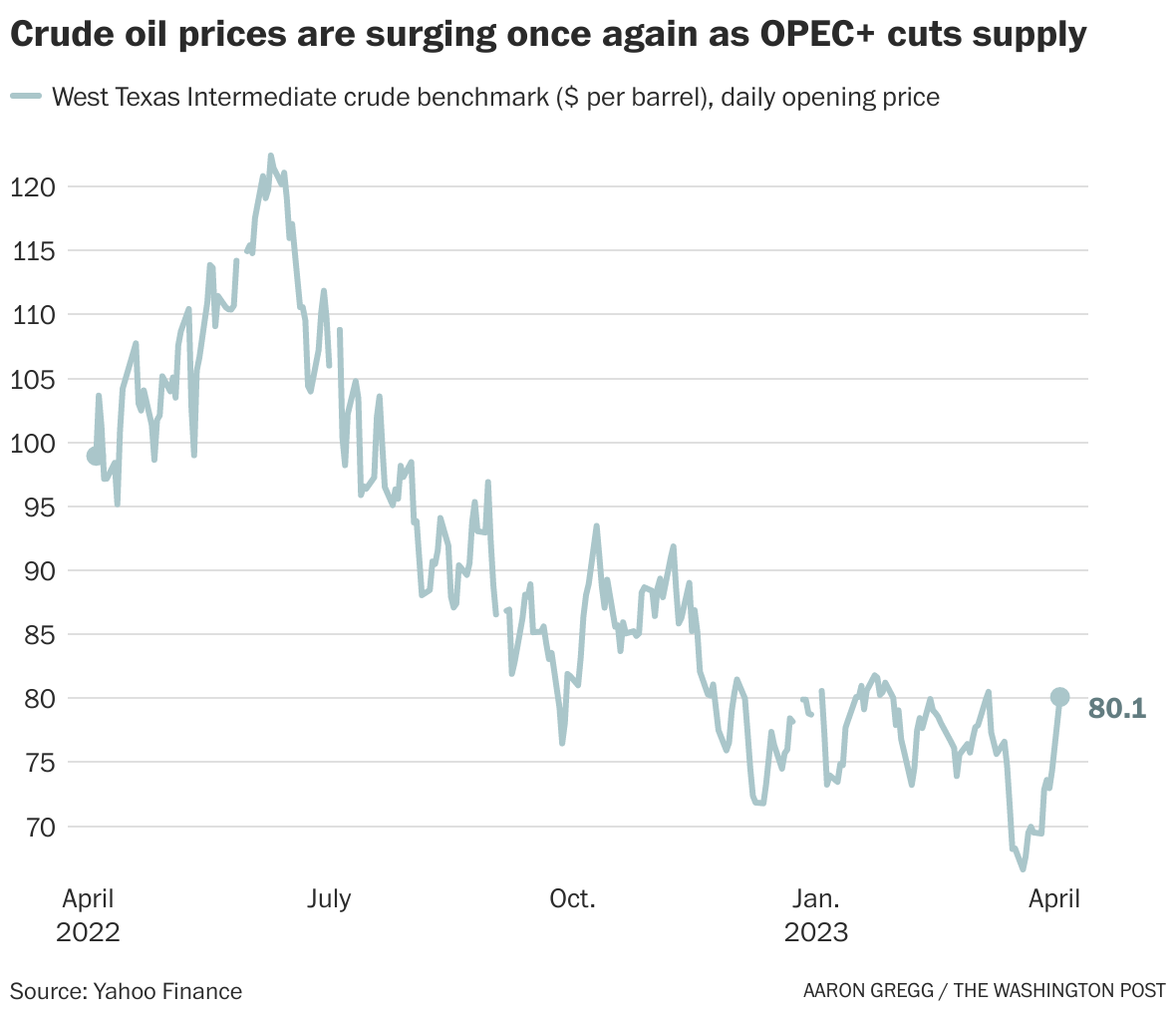

Oil Prices Surge 3% Despite UAE’s OPEC Exit—WTI Nears $100 Again

On April 28, 2026, West Texas Intermediate (**WTI**) crude surged 3% to reclaim the $100-per-barrel threshold, defying expectations after the United Arab Emirates (UAE) announced its exit from OPEC. The ... Read More