Dalton Snapchat Video Explained

On May 26, 2026, a video linked to “Dalton” and the Avian & Exotic Philly Vet sparked scrutiny over Snapchat’s content moderation systems, revealing gaps in AI-driven video analysis and ... Read More

Saturday Edition

Stay updated with Archyde – your source for breaking news, global headlines, economy, entertainment, health, technology, and sports. Fresh stories daily.

On May 26, 2026, a video linked to “Dalton” and the Avian & Exotic Philly Vet sparked scrutiny over Snapchat’s content moderation systems, revealing gaps in AI-driven video analysis and ... Read More

Continuous Coverage

UK consumers face sustained price inflation through mid-2026 as core CPI remains sticky at 3.8% YoY, driven by…

High above the Pir Panjal range, where the air thins and the sky stretches into an unbroken blue,…

Roxy Horner’s candid account of wedding-day anxiety highlights the global prevalence of anxiety disorders, affecting 264 million people…

Shamrock Rovers stunned Bohs with a 97th-minute winner at Dalymount, sparking chaos in a Premier Division derby. The…

Wordle’s May 25, 2026, puzzle (#1801) dropped late Tuesday night with a fiery twist: the answer was BLAZE,…

Pope Francis issues a scathing critique of AI ethics, sparking market volatility in tech sectors. The encyclical questions…

Global Affairs

Brazilian President Luiz Inácio Lula da Silva, 78, began radiation therapy this week after an early-stage skin cancer…

Markets And Money

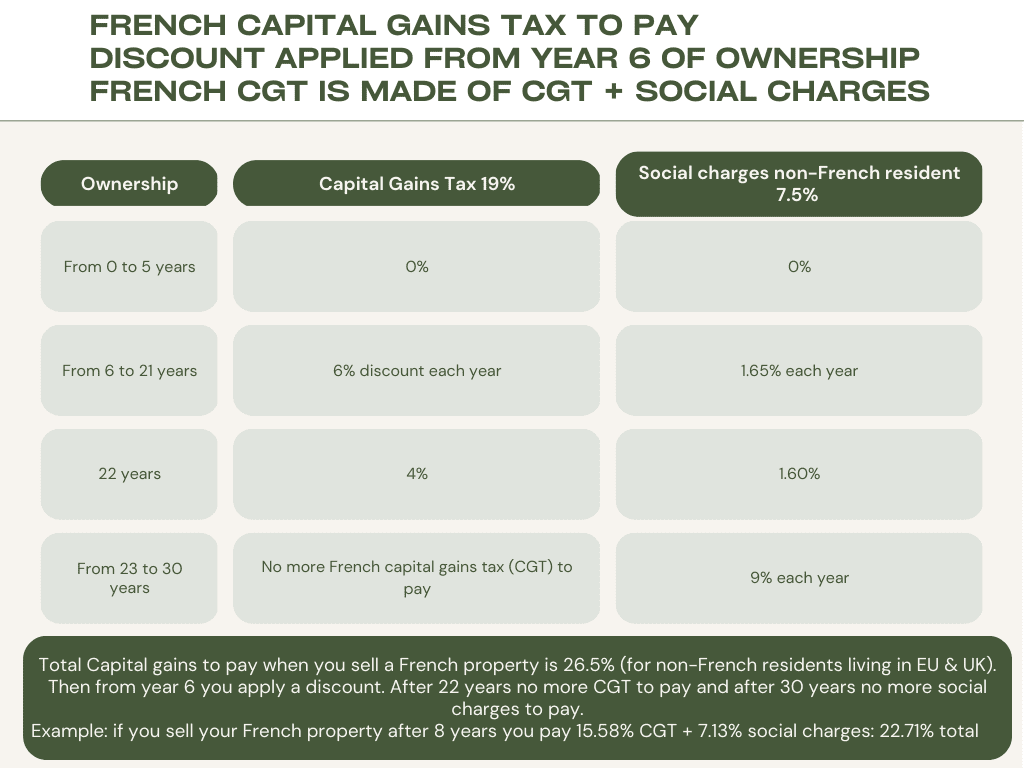

France’s newly enacted capital gains tax law—approved in late April—is already under fire as lawmakers scramble to amend…

Digital Culture

Bill Gates once called the Mac “the future of computing,” but Apple’s true rival was always Microsoft, as…

Science And Wellbeing

Emergency Care Workforce Expansion in Buhuși Addresses Regional Health Needs Spitalul din Buhuși is recruiting a specialist in…

Screen And Sound

Portugal’s Secret Story is in a state of high-stakes drama as four contestants—Afonso, Leandro, Sara, and Catarina—hang by…

Fixtures And Form

Rapid Vienna Secures European Qualification Amidst Tactical Instability Rapid Vienna salvaged a turbulent 2025/26 campaign by defeating SV…