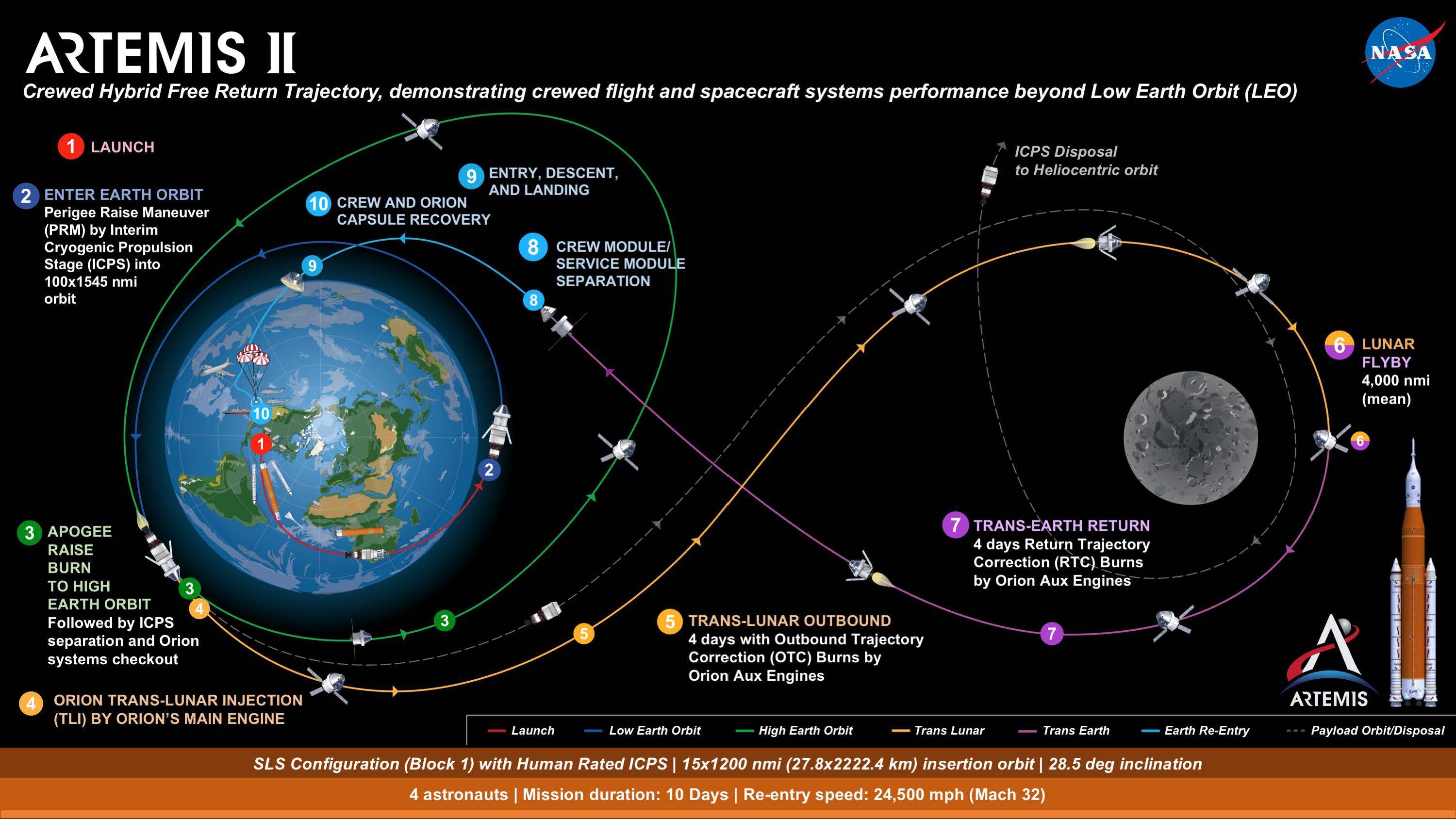

NASA’s Artemis II mission has successfully placed four astronauts on a lunar flyby, marking the first crewed journey to the moon’s vicinity since 1972. The mission validates the Orion spacecraft and SLS rocket, signaling a transition toward a sustainable, commercialized lunar economy and permanent human presence.

While the headlines focus on the “majestic” views and record-breaking distances, the institutional market sees this as a critical de-risking event. This is not a voyage of discovery; it is a stress test for the industrial base of the “New Space” economy. For investors, the success of Artemis II confirms the viability of the government-led architecture that underpins billions of dollars in contracts for prime aerospace contractors.

The Bottom Line

- Industrial Validation: The successful lunar loop secures the long-term funding trajectory for the Space Launch System (SLS) and Orion, benefiting Lockheed Martin (NYSE: LMT) and Boeing (NYSE: BA).

- Market Expansion: The mission transitions the lunar economy from theoretical R&D to operational logistics, opening a multi-billion dollar window for lunar cargo and habitat providers.

- Geopolitical Hedge: The mission accelerates the “Space Race 2.0,” ensuring that US government spending on space remains a non-discretionary budgetary item to counter China’s lunar ambitions.

The Infrastructure Play: De-risking the Prime Contractors

The financial architecture of the Artemis program is a hybrid of traditional cost-plus contracting and modern fixed-price milestones. The successful orbit of Artemis II provides a critical “proof of concept” for the Orion capsule’s life support and heat shield systems. Here is the math: any failure at this stage would have triggered a systemic review of the SLS program, potentially threatening the multi-year revenue streams of the prime contractors.

Lockheed Martin (NYSE: LMT), as the lead contractor for the Orion spacecraft, stands to benefit most from this operational success. By hitting these milestones, they solidify their position as the indispensable provider of crewed deep-space transport. However, the balance sheet tells a different story regarding efficiency. The SLS remains an expensive legacy system compared to the reusable models championed by private entities.

But the market is not pricing in efficiency; it is pricing in reliability. For institutional portfolios, the “guaranteed” nature of NASA contracts provides a low-beta hedge against volatility in other sectors. We are seeing a shift where the government acts as the “anchor tenant,” creating a stable environment for secondary commercial markets to emerge.

Bridging the Gap: From Exploration to the Lunar Economy

The “Information Gap” in current reporting is the failure to connect this mission to the broader macro-economic trend of In-Situ Resource Utilization (ISRU). The goal is not to visit the moon, but to mine it. The focus on “mysterious craters” mentioned by the crew is less about geology and more about the identification of water ice—the “oil” of the solar system.

Water ice can be converted into liquid hydrogen and oxygen for rocket fuel. If this infrastructure is established, the cost of deep-space transport decreases by an estimated 60-80% because payloads no longer need to carry all their fuel from Earth’s gravity well. This fundamentally alters the valuation of companies involved in lunar logistics and orbital refueling.

“The transition from exploration to exploitation is where the real alpha lies. We are moving from a period of government-funded science to a period of infrastructure-led commercialization. The lunar surface is effectively the new ‘frontier land’ for industrial conglomerates.”

This shift is already impacting the supply chain. We are seeing increased capital allocation toward specialized materials and robotics. Northrop Grumman (NYSE: NOC) is positioning itself as a leader in the Gateway—the planned lunar orbiting station—which will serve as the primary logistics hub for all lunar activity. This makes the Gateway a critical piece of “real estate” in the space economy.

Comparing the Space Industrial Base

To understand the market distribution, we must look at how the primary players are positioned within the Artemis ecosystem. The following table summarizes the strategic roles and financial exposure of the key public entities involved.

| Company | Primary Role | Revenue Driver | Market Risk Profile |

|---|---|---|---|

| Lockheed Martin (LMT) | Orion Spacecraft | High-margin gov contracts | Low (Diversified Defense) |

| Boeing (BA) | SLS Core Stage | Fixed-price milestones | High (Operational Headwinds) |

| Northrop Grumman (NOC) | Gateway Modules | Long-term infrastructure | Medium (Execution Risk) |

| SpaceX (Private) | HLS (Starship) | Commercial/Gov Hybrid | Medium (Technical Iteration) |

The Geopolitical Hedge and Capital Flows

We cannot analyze Artemis II in a vacuum. The mission is a direct response to the China National Space Administration’s (CNSA) timeline for crewed lunar landings. This creates a “spending floor.” Regardless of shifts in US domestic policy or short-term budget cuts, the strategic necessity of maintaining lunar primacy ensures a steady flow of capital into the aerospace sector.

Here is the friction: the tension between the legacy “cost-plus” model of Boeing (NYSE: BA) and the “disruptive” model of SpaceX. While Artemis II uses the SLS, the eventual landing depends on Starship. This creates a precarious dependency where the US government is tethered to a private entity for the final mile of the mission.

For the savvy investor, the play is not in the launch vehicles themselves, but in the “picks and shovels” of the lunar economy. This includes satellite communications, autonomous mining equipment, and radiation-shielding materials. These are the sectors where we expect to see significant M&A activity as larger defense firms acquire agile startups to fill technical gaps.

For further analysis on government procurement trends, refer to the latest SEC filings of the prime contractors or the budgetary breakdowns provided by Reuters and Bloomberg.

Future Market Trajectory

As Artemis II returns and the data is analyzed, the market will pivot its attention to Artemis III—the actual landing. The success of this loop mission has effectively shifted the probability of a 2026 landing from a “coin flip” to a “high-probability event.”

Expect an increase in forward guidance for the space segments of Lockheed Martin and Northrop Grumman in the coming quarters. The “Space Economy” is no longer a speculative venture for VC firms; it is becoming a core pillar of the industrial economy. The trajectory is clear: the moon is no longer a destination, but a strategic asset.

Investors should monitor the Wall Street Journal’s coverage of the upcoming NASA budget hearings, as the allocation for the “Lunar Gateway” will be the primary indicator of how quickly the commercial lunar economy will scale.