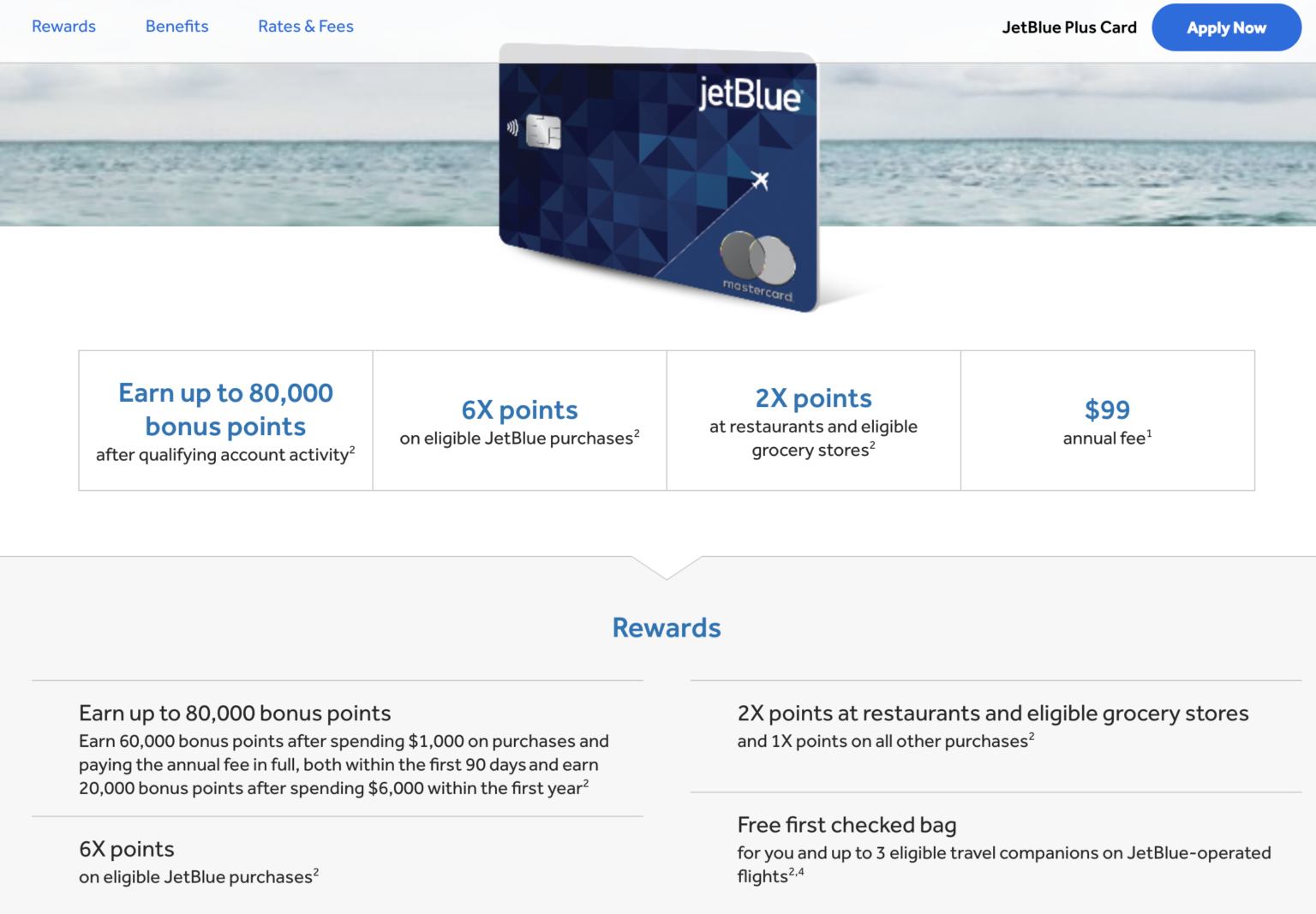

Barclays (NYSE: BCS) has enhanced its JetBlue co-branded credit card rewards program without increasing annual fees. This strategic move aims to bolster consumer loyalty and card utilization amidst a broader economic shift, coinciding with the bank’s downward revision of its auto-dealer sector forecasts as credit quality weakens.

This isn’t just a perk update for frequent flyers; it is a calculated defensive maneuver. By improving rewards without hiking fees, Barclays is attempting to maintain its deposit base and transaction volume in a high-interest-rate environment where consumers are increasingly sensitive to “fee creep.” Though, the simultaneous slashing of auto-dealer projections reveals a deeper anxiety: the bank is bracing for a spike in defaults within the automotive lending space.

The Bottom Line

- Customer Retention: Barclays is leveraging “value-adds” to prevent churn as consumers migrate toward high-yield alternatives.

- Sector Divergence: While the consumer credit arm pushes growth, the commercial auto-dealer outlook is turning bearish.

- Risk Management: Lowered projections for auto-dealers suggest an anticipated contraction in credit availability or an increase in non-performing loans (NPLs).

The Psychology of the Fee-Free Reward Pivot

In the current macroeconomic climate, the “fee hike” is a dangerous catalyst for customer attrition. For Barclays (NYSE: BCS), increasing the annual fee on the JetBlue card would have likely triggered a wave of cancellations, especially as consumers scrutinize their monthly subscriptions.

But the balance sheet tells a different story. By enhancing rewards, the bank incentivizes higher spend (interchange revenue) without the negative PR of a price increase. Here is the math: the cost of the rewards is an acquisition and retention expense, which is significantly cheaper than the cost of replacing a lost high-net-worth customer.

This strategy mirrors the broader trend seen across the financial services sector, where banks are shifting from explicit fees to implicit monetization through increased transaction volume.

The Auto-Dealer Warning Sign

While the JetBlue news is a positive marketing play, the reduction in auto-dealer forecasts is the real story for institutional investors. The automotive sector is currently a canary in the coal mine for broader economic distress. High interest rates have squeezed dealer margins and increased the cost of floor-plan financing.

When a systemic player like Barclays lowers its guidance for this sector, it suggests a tightening of credit standards. We are seeing a transition from a growth phase to a risk-mitigation phase. This likely impacts the valuation of automotive lenders and the liquidity of mid-sized dealerships.

To understand the scale of this risk, we must look at the current credit landscape. The following table outlines the divergent trajectories within the Barclays portfolio based on recent strategic shifts.

| Segment | Strategic Action | Expected Impact | Risk Profile |

|---|---|---|---|

| Consumer Credit (JetBlue) | Rewards Enhancement | Increased Wallet Share | Low/Moderate |

| Auto-Dealer Lending | Guidance Reduction | Lower Revenue Growth | High (Credit Risk) |

| Corporate Banking | Risk Tightening | Margin Compression | Moderate |

Connecting the Dots: Macroeconomic Headwinds

The disconnect between “better rewards” and “worse dealer forecasts” is a classic symptom of a bifurcated economy. High-income consumers (the target for JetBlue rewards) remain resilient, while the middle-market commercial sector (auto dealers) is feeling the weight of monetary tightening.

This divergence creates a volatility gap. If the auto-dealer sector experiences a systemic correction, the gains made in consumer credit retention may be offset by loan-loss provisions. This represents why the market is watching Barclays (NYSE: BCS) closely as they navigate the transition toward the end of Q2.

“The current credit cycle is not behaving linearly. We are seeing pockets of extreme resilience in premium consumer spending while the commercial middle-market is facing a liquidity crunch that hasn’t been seen since the early 2020s.”

This sentiment is echoed by analysts at The Wall Street Journal, who note that banks are currently playing a game of “whack-a-mole,” solving for consumer churn while simultaneously hedging against commercial defaults.

The Strategic Path Forward for Investors

For those tracking the financial sector, the takeaway is clear: do not be distracted by the “sugar” of consumer rewards. The real alpha lies in the commercial guidance. The reduction in auto-dealer projections is a leading indicator of a cooling economy.

As we move toward the close of the current quarter, the focus will shift to the SEC (Securities and Exchange Commission) filings and the subsequent earnings calls. Investors should look for specific data on the “Cost of Risk” (CoR) and whether the auto-dealer downturn is an isolated incident or a systemic contagion.

In short, Barclays is attempting to maintain its “front-end” growth while quietly bracing for “back-end” losses. It is a pragmatic, if cautious, approach to a volatile 2026 market.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.