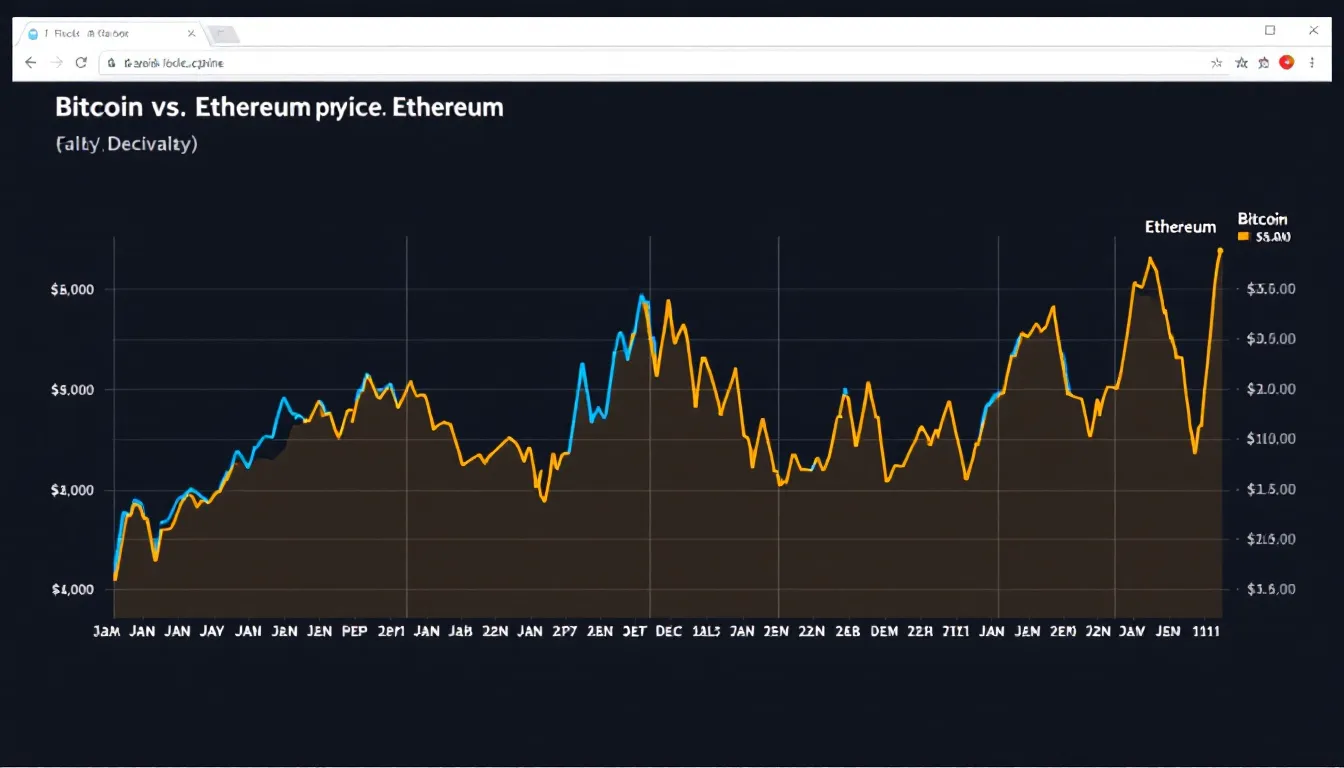

Bitcoin has maintained market dominance for eight years, consolidating its position as the primary digital reserve asset. While Ethereum and XRP persist in the top tier, the vast majority of early cryptocurrencies have collapsed, signaling a systemic transition from speculative retail trading to institutional-grade capital allocation and regulatory scrutiny.

The persistence of Bitcoin is not a fluke of early adoption; it is a manifestation of the “flight to quality” typically seen in mature financial markets. For years, the crypto landscape was characterized by a “rising tide lifts all boats” mentality, where speculative capital flowed indiscriminately into any project promising decentralized utility. Though, as we move through the second quarter of 2026, the market has undergone a brutal pruning process. The disappearance of once-prominent altcoins proves that without a sustainable value proposition or institutional infrastructure, digital assets cannot survive multiple volatility cycles.

The Bottom Line

- Market Consolidation: Bitcoin’s dominance confirms a shift toward “Blue Chip” digital assets, marginalizing speculative altcoins that lack intrinsic utility.

- Institutional Validation: The integration of spot ETFs by firms like BlackRock (NYSE: BLK) has created a structural floor for Bitcoin, decoupling it from the broader “crypto-casino” volatility.

- Utility Divergence: Ethereum and XRP survived by pivoting toward specific enterprise functions—smart contracts and cross-border settlements—while others remained purely speculative.

The Institutional Filter: Why the “Great Shakeout” Occurred

The disappearance of dozens of top-tier cryptocurrencies over the last eight years is a textbook example of market Darwinism. In the early 2010s, the barrier to entry for launching a token was negligible. Today, the barrier is regulatory compliance and liquidity.

Here is the math: the arrival of institutional capital requires transparency and custody solutions that 99% of early altcoins could not provide. When BlackRock (NYSE: BLK) and Fidelity (Private) entered the fray, they didn’t look for the “next big thing”; they looked for the asset with the most established liquidity and the clearest regulatory status. This created a feedback loop: institutional inflows drove Bitcoin’s price, which attracted more institutions, further starving smaller projects of the liquidity they needed to survive.

But the balance sheet tells a different story for the survivors. Ethereum transitioned to Proof of Stake, reducing its energy footprint and attracting ESG-conscious funds. XRP focused on the plumbing of global finance, attempting to bridge the gap between legacy banking and blockchain. The assets that vanished lacked this strategic pivot.

“The era of speculative mania in digital assets has been replaced by a demand for verifiable utility. Investors are no longer buying a whitepaper; they are buying a cash-flow equivalent or a systemic necessity.”

The Macro Correlation: Digital Gold vs. Speculative Beta

As markets open this Monday in April 2026, the correlation between Bitcoin and traditional “safe haven” assets has tightened. Bitcoin is no longer trading as a high-beta tech stock; it is behaving more like a digital version of gold, reacting to central bank policies and geopolitical instability.

The impact on the broader economy is evident in how corporate treasuries are managed. MicroStrategy (NASDAQ: MSTR) pioneered the strategy of using Bitcoin as a primary treasury reserve, a move that was once viewed as reckless but is now analyzed as a hedge against currency debasement. This shift has forced other C-suite executives to reconsider their exposure to fiat volatility.

To understand the current hierarchy, we must look at the distribution of market value among the survivors compared to the extinct assets.

| Asset | Primary Value Driver | Institutional Support | Market Status (2026) |

|---|---|---|---|

| Bitcoin | Store of Value / Digital Gold | High (Spot ETFs, Treasuries) | Dominant Reserve |

| Ethereum | Smart Contract Infrastructure | Medium-High (Staking/DeFi) | Utility Standard |

| XRP | Cross-Border Liquidity | Medium (Banking Partnerships) | Niche Infrastructure |

| Legacy Alts | Speculative Hype | Negligible | Defunct/Illiquid |

The Regulatory Moat and the SEC’s Long Game

The survival of the “Big Three” is inextricably linked to the U.S. Securities and Exchange Commission (SEC)‘s evolving stance on what constitutes a security. For years, the SEC fought a war of attrition against the crypto industry, but the result was an unintended “regulatory moat.”

By aggressively pursuing projects that functioned as unregistered securities, the SEC effectively cleared the field of competitors that lacked the legal capital to fight back. Bitcoin, having no central issuer, remained largely untouchable. Ethereum and XRP, through protracted legal battles and structural changes, managed to carve out a recognized legal status.

This regulatory clarity has allowed Bloomberg and other financial data providers to integrate these assets into professional terminals with confidence. The “disappeared” cryptos were not just victims of bad tech; they were victims of a regulatory environment that demanded a level of compliance they could not afford.

The Trajectory: A Bifurcated Future

Looking ahead, the market is splitting into two distinct categories: institutional assets and retail gambles. The probability of a fresh asset entering the top five is now statistically low. The network effects surrounding Bitcoin are too powerful, and the infrastructure built around Ethereum is too deeply embedded in the DeFi ecosystem.

For the business owner or investor, the lesson is clear: the “lottery ticket” phase of cryptocurrency is over. The current market rewards stability, liquidity, and regulatory alignment. As we analyze the Reuters data on global capital flows, the focus has shifted from “which coin will moon” to “how does this asset fit into a diversified 60/40 portfolio.”

The consolidation we see today is the final stage of the asset class’s adolescence. Bitcoin’s eight-year reign is not a sign of stagnation, but a sign of maturity. The market has finally decided what it values: scarcity, security, and systemic integration.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.