Bitcoin is currently navigating a transition from a speculative asset to a “mature” market instrument, characterized by high volatility and a struggle to maintain its 1.3 trillion USD market capitalization. As of April 6, 2026, the asset faces a critical identity crisis: whether it remains a viable hedge against inflation or a mere speculative tool.

The current market tension isn’t just about price fluctuations. it is about the fundamental shift in who owns the asset. We are seeing a transition from retail “HODLers” to institutional custodians. When the BlackRock (NYSE: BLK)-led ETF wave collided with macroeconomic headwinds, the resulting volatility revealed a stark truth: Bitcoin’s correlation with risk-on assets is higher than its proponents claim. This matters due to the fact that if Bitcoin fails to decouple from the Nasdaq, its value proposition as “digital gold” evaporates.

The Bottom Line

- Institutionalization vs. Volatility: The entry of spot ETFs has stabilized the floor but capped the explosive “moon” growth seen in previous cycles.

- The Inflation Paradox: Despite claims of being a hedge, Bitcoin often trades as a high-beta tech stock, reacting sharply to Federal Reserve interest rate pivots.

- Liquidity Thresholds: Maintaining the 1.3 trillion USD market cap is the psychological line between a “correction” and a “regime shift” in valuation.

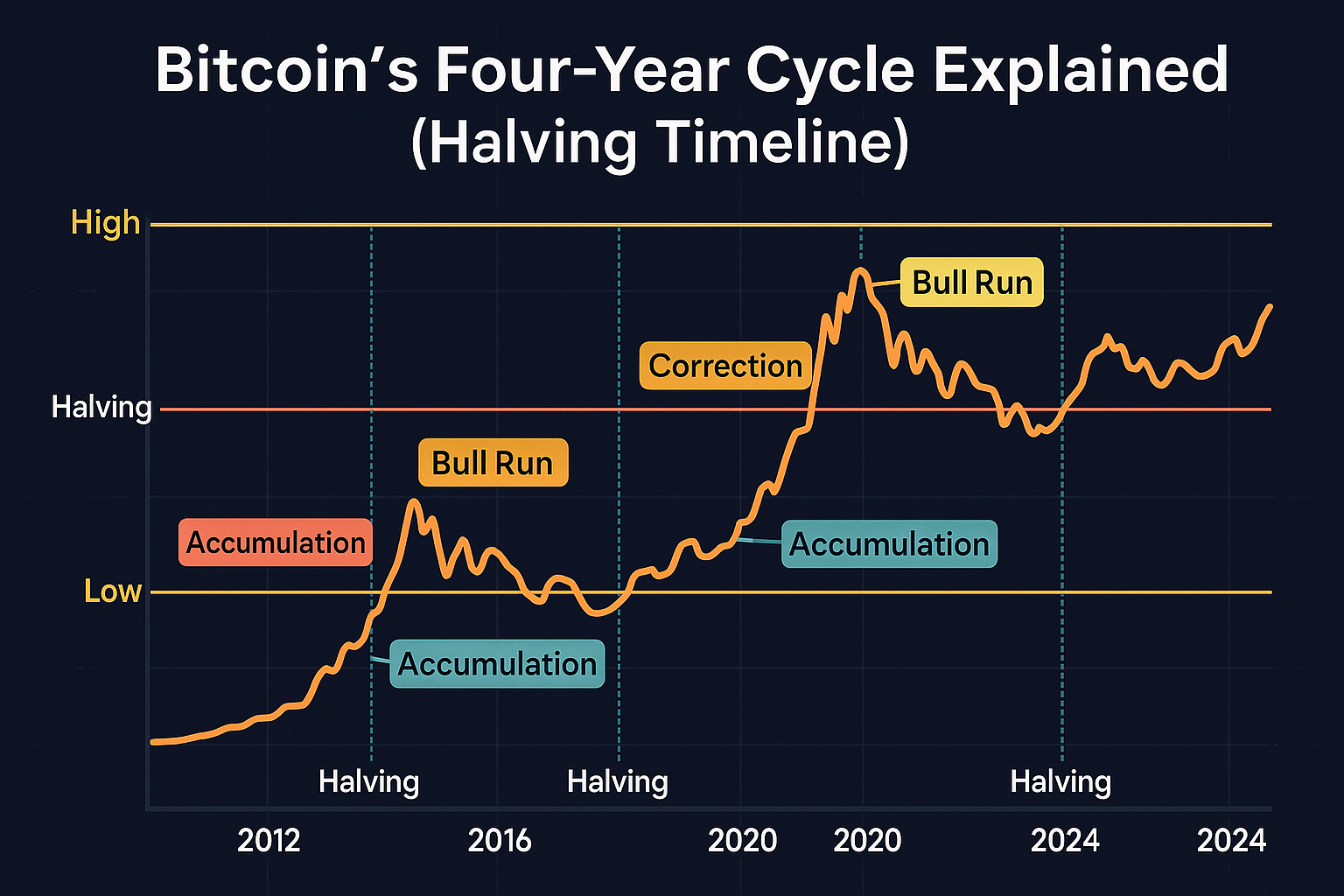

The Liquidity Trap: Why 1.3 Trillion is the Magic Number

Market participants are currently obsessed with the 1.3 trillion USD threshold. But the balance sheet tells a different story. A 45% decline over a six-month window suggests that the “maturity” of the market is actually a period of aggressive deleveraging.

Here is the math: When institutional capital enters via ETFs, the liquidity profile changes. We no longer have fragmented retail buying; we have concentrated institutional flows. This creates “liquidity pockets” where the price can slide rapidly if a few large funds decide to rebalance their portfolios toward safer yields, such as US Treasuries.

The relationship between the SEC (Securities and Exchange Commission) and the crypto ecosystem has shifted from outright hostility to regulatory absorption. This absorption removes the “outlaw premium” that previously drove Bitcoin’s price higher during times of systemic instability.

| Metric | Speculative Phase (Pre-2024) | Mature Phase (2026 Projection) | Market Impact |

|---|---|---|---|

| Primary Holder | Retail / Early Adopters | Institutional Funds / ETFs | Lower Volatility, Higher Floor |

| Correlation to S&P 500 | Low to Moderate | High (Positive Correlation) | Reduced Diversification Benefit |

| Market Cap Stability | Erratic / Exponential | Cyclical / Range-bound | Predictable Institutional Flows |

The Hedge Fallacy and the Macroeconomic Headwind

There is a persistent narrative that Bitcoin is a store of value against global inflation. However, the data from the last few quarters suggests otherwise. In a high-interest-rate environment, the opportunity cost of holding a non-yielding asset like Bitcoin becomes prohibitive.

But the real danger is the “Speculation Trap.” When Bitcoin is treated as a speculative tool rather than a currency, it becomes hypersensitive to the Consumer Price Index (CPI) prints. If inflation remains sticky, the Federal Reserve keeps rates high, and the “digital gold” narrative fails because investors prefer the guaranteed 4-5% yield of a T-bill over the uncertainty of a volatile coin.

“The transition of Bitcoin from a fringe experiment to a Wall Street product is a double-edged sword. While it provides legitimacy and liquidity, it strips the asset of its volatility-driven allure, forcing it to compete on the same fundamentals as any other financial instrument.”

This shift impacts the broader economy by altering how venture capital flows into the Fintech sector. Companies like Coinbase (NASDAQ: COIN) are no longer just “crypto exchanges” but are becoming integrated financial infrastructure providers. Their revenue streams are shifting from volatile trading fees to steady custodial fees—a classic sign of market maturation.

The Institutional Pivot: From Hype to Hedge Funds

We are seeing a strategic realignment. The “shock of numbers” mentioned in recent reports isn’t just about price drops; it’s about the realization that Bitcoin’s growth is now tethered to global liquidity cycles. When the Bloomberg Terminal shows a liquidity crunch in the Eurodollar market, Bitcoin usually feels the pain first.

Here is the reality: The “brilliance” of the investment is no longer in the 100x gains. It is now in the 2-5% portfolio allocation used to capture “convexity”—the idea that a slight amount of exposure can provide outsized returns without risking the entire portfolio.

This puts Bitcoin in direct competition with gold and other commodities. However, unlike gold, Bitcoin lacks a central bank’s reserve backing. Its only “reserve” is the collective belief in the network’s security and the scarcity of its 21 million coin limit. As the Reuters financial data indicates, this belief is currently being tested by the reality of a slowing global economy.

The Trajectory: Convergence or Collapse?

Looking ahead toward the close of the current fiscal year, Bitcoin is unlikely to return to its “wild west” days. Instead, we are entering an era of convergence. We will see Bitcoin integrated into standard 60/40 portfolios, not as a replacement for equity, but as a high-volatility diversifier.

For the business owner and the investor, the takeaway is clear: Stop treating Bitcoin as a lottery ticket and start treating it as a volatile financial instrument. The “glow” of the investment hasn’t disappeared, but it has changed from a blinding neon light to a steady, institutional flicker. The winners of the next cycle will not be those who “bought the dip,” but those who understand the macroeconomic triggers that drive institutional liquidity.

The final verdict? Bitcoin isn’t losing its investment appeal; it is losing its anonymity. And in the world of high finance, anonymity is expensive, but transparency is where the real scale happens.