Bank of America (NYSE: BAC) has lowered its FY27 earnings growth forecast for Nifty 50 companies to 8.5%, citing escalating stagflation risks and crude oil volatility. The revision reflects a cautious outlook on India’s GDP growth amid geopolitical instability in the Middle East and persistent inflationary pressures.

This isn’t just a routine adjustment of spreadsheets. It’s a signal that the premium valuation typically afforded to Indian equities is facing a stress test. When the world’s largest brokerage pivots from optimism to “worst-case scenario” warnings, the market begins to price in a structural shift rather than a temporary dip.

But the balance sheet tells a different story. While the macro-outlook is clouded, the underlying corporate strength of the Nifty 50 remains a point of contention between institutional bears and domestic bulls.

The Bottom Line

- Earnings Compression: Forecasts for Nifty 50 earnings growth have been revised downward to 8.5% for FY27, reflecting a tighter margin environment.

- Stagflation Risk: The combination of stagnant GDP growth and rising input costs—driven by crude oil—threatens corporate EBITDA margins.

- Geopolitical Hedge: A resolution to the Iran-Israel conflict remains the primary catalyst for a valuation rerating and a return to bullish sentiment.

The Crude Oil Paradox and Margin Erosion

India imports approximately 85% of its crude oil requirements, making the Nifty 50 exceptionally sensitive to Brent pricing. When crude spikes, the impact is twofold: it widens the current account deficit and increases operational costs for logistics and manufacturing giants like Reliance Industries (NSE: RELIANCE).

Here is the math: Higher oil prices act as a regressive tax on the Indian consumer. As transport costs rise, discretionary spending drops, hitting the revenues of consumer staples and automotive sectors. This creates the “stagflationary” trap—where inflation rises but economic output slows.

To understand the scale of the risk, we must look at the current macroeconomic positioning compared to historical averages. The Bloomberg Terminal data suggests that for every $10 increase in the price of a barrel of oil, India’s fiscal deficit typically widens by roughly 0.1% to 0.2% of GDP.

| Metric | Previous Forecast (Est.) | BofA Revised Forecast (FY27) | Variance |

|---|---|---|---|

| Nifty 50 Earnings Growth | 11.0% – 12.5% | 8.5% | -2.5% to -4.0% |

| GDP Growth Projection | 6.8% – 7.0% | Lowered (Unspecified) | Negative |

| Brent Crude Sensitivity | Moderate | High (Stagflationary) | Increased Risk |

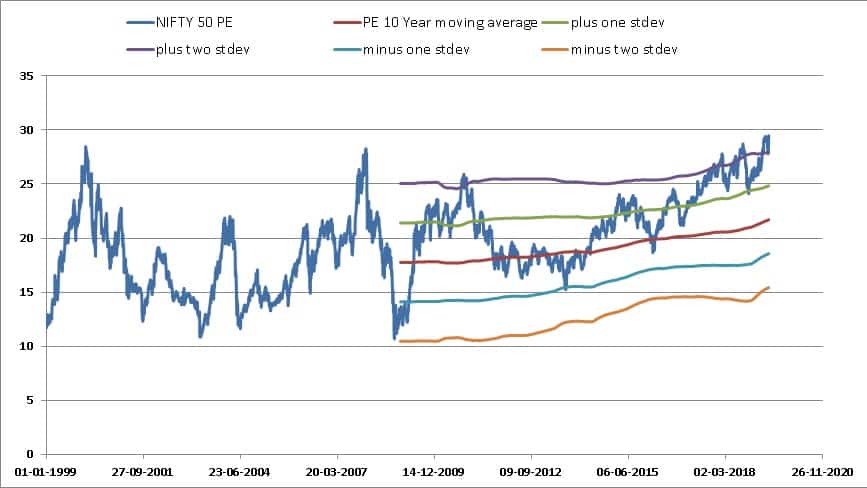

Analyzing the Valuation Gap and PE Ratios

The Nifty 50 has historically traded at a premium compared to other emerging markets. However, that premium is predicated on the assumption of consistent 6%+ GDP growth. If Bank of America (NYSE: BAC) is correct about the slowdown, the Price-to-Earnings (P/E) ratios of top-tier firms may undergo a “multiple contraction.”

Which means investors will no longer pay as much for every rupee of profit. We are seeing this play out in the banking sector, where HDFC Bank (NSE: HDFCBANK) and ICICI Bank (NSE: ICICIBANK) are navigating a complex environment of rising cost of funds and stabilizing net interest margins (NIMs).

But is this a crash or a correction? Most institutional analysts argue it is the latter. The Reuters consensus indicates that domestic institutional investors (DIIs) are providing a significant cushion, offsetting the outflows from Foreign Institutional Investors (FIIs).

“The risk is not necessarily a collapse in earnings, but a plateau. If the cost of capital remains elevated while growth decelerates, the equity risk premium must be adjusted upward, which naturally puts downward pressure on stock prices.”

The Geopolitical Pivot: The Iran Variable

The brokerage’s warning is not an absolute condemnation. There is a clear “exit ramp” identified: the resolution of the conflict in the Middle East. A stabilization of the Strait of Hormuz would immediately lower the risk premium on crude oil, potentially adding 100-200 basis points back to the GDP growth forecast.

This creates a binary outcome for traders. On one hand, the “worst-case scenario” involves a prolonged energy crisis that forces the Reserve Bank of India (RBI) to maintain interest rates higher for longer to combat imported inflation. On the other, a diplomatic breakthrough would trigger a massive relief rally.

For those tracking the Wall Street Journal’s coverage of global energy markets, the correlation is clear: Nifty 50 performance is currently more tied to geopolitical headlines than to internal corporate quarterly reports.

Strategic Implications for Portfolio Allocation

In a stagflationary environment, the “growth at any price” strategy fails. The focus shifts toward companies with high pricing power—those that can pass increased costs onto the consumer without seeing a collapse in volume.

Look for companies with low debt-to-equity ratios and strong free cash flow. The current environment favors “defensive growth”—sectors like specialized pharmaceuticals or high-end IT services that are less sensitive to the immediate price of a barrel of oil but benefit from long-term digital transformation trends.

the Bank of America (NYSE: BAC) report serves as a pragmatic reminder: India’s growth story is robust, but it is not immune to global systemic shocks. The shift to an 8.5% earnings forecast is a call for caution, not a call for exit.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.