Netflix (NASDAQ: NFLX) premieres “BTS: The Return” tonight at 12:00 AM PT, targeting subscriber retention amid plateauing growth. **HYBE Co., Ltd. (KRX: 352820)** monetizes intellectual property through licensing, diversifying revenue beyond touring. This release tests the efficacy of high-cost content in reducing churn rates for streaming giants.

The release of “BTS: The Return” is not merely a cultural event. it is a calculated capital allocation decision. In the current fiscal environment, content spend must yield measurable returns in subscriber lifetime value (LTV). Netflix (NASDAQ: NFLX) faces pressure to justify programming budgets as interest rates stabilize but competition intensifies from Disney (NYSE: DIS) and Amazon (NASDAQ: AMZN). The documentary serves as a retention tool rather than a primary acquisition driver, aiming to stabilize the user base during a traditionally soft Q2 period.

The Bottom Line

- Capital Efficiency: Licensing existing IP is generally more capital-efficient than producing original scripted series, improving near-term free cash flow.

- Market Correlation: Positive reception may correlate with a short-term bullish sentiment for HYBE Co., Ltd. (KRX: 352820) stock, though liquidity remains lower than US tech peers.

- Churn Mitigation: Eventized content reduces monthly cancellation rates, a key metric for Wall Street valuation models in the streaming sector.

The Economics of Idol Licensing Versus Original Production

Streaming platforms constantly weigh the cost of original production against licensing established intellectual property. Producing a scripted series often requires significant upfront capital with uncertain ROI. Conversely, licensing a documentary about an established act like BTS shifts the risk profile. The production costs are largely sunk by the artist’s label, while the streaming platform pays a licensing fee.

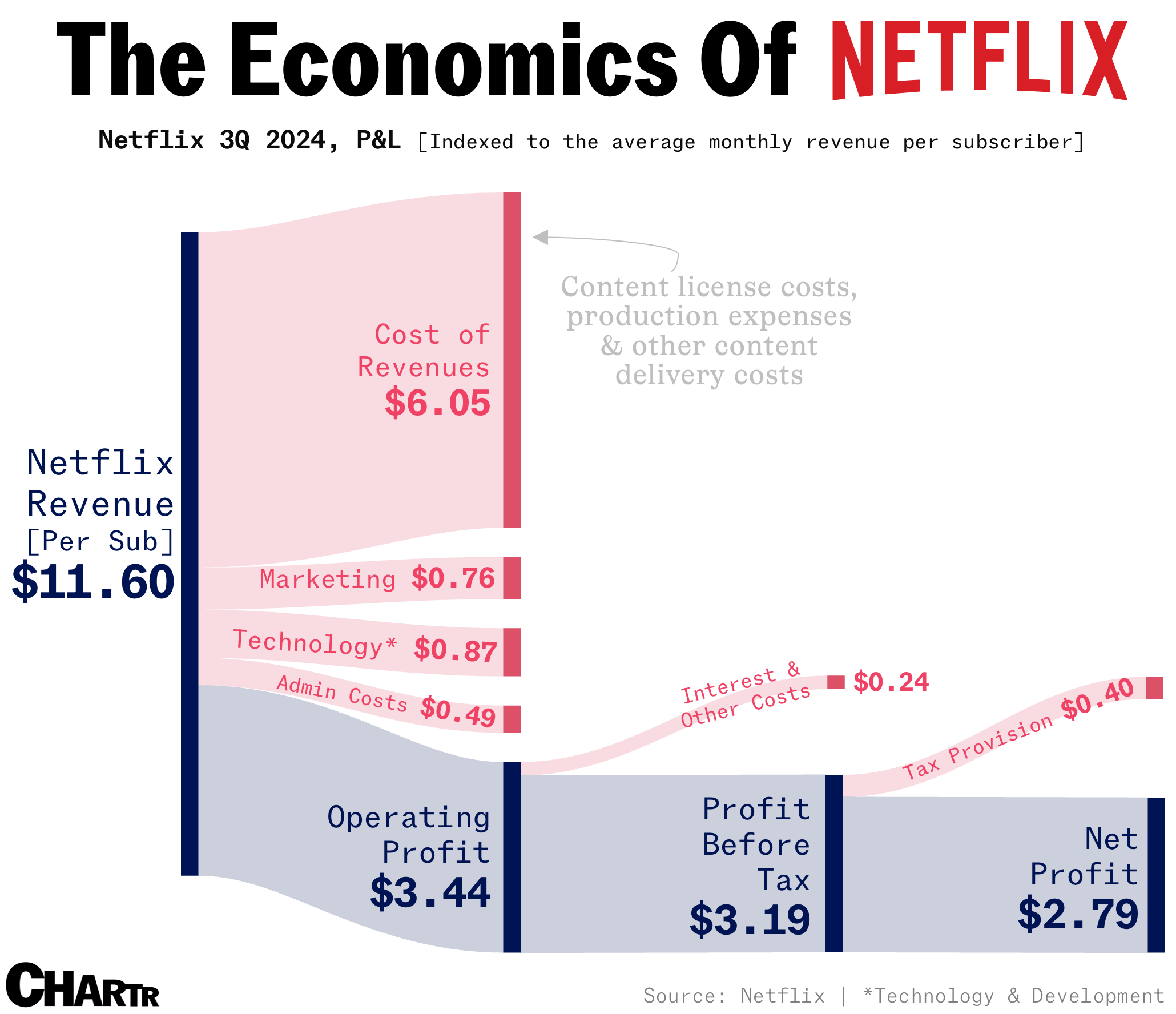

Here is the math on why this matters for the balance sheet. Original scripted dramas can cost upwards of $10 million per episode. A documentary licensing deal typically operates on a different margin structure. This allows Netflix (NASDAQ: NFLX) to deploy capital elsewhere, perhaps in infrastructure or localized content production in emerging markets. Netflix SEC Filings consistently highlight the importance of managing content amortization to maintain healthy operating margins.

But the balance sheet tells a different story regarding long-term value. Original content remains on the platform indefinitely, building a permanent library. Licensed content often has expiration dates. If “BTS: The Return” drives significant engagement, the negotiation leverage shifts to **HYBE Co., Ltd. (KRX: 352820)** for future renewals. This dynamic creates a recurring liability for the streamer if the asset proves indispensable to subscriber retention.

Subscriber Retention Metrics and Market Sentiment

Wall Street analysts focus heavily on churn rates when evaluating streaming equities. High churn erodes the lifetime value of a customer, making customer acquisition costs (CAC) unsustainable. Eventized releases like this documentary create spikes in engagement that suppress cancellation requests. Bloomberg Market Data indicates that platforms with consistent engagement spikes tend to trade at higher multiples relative to their revenue growth.

However, one-off events do not solve structural retention issues. The market demands a consistent pipeline of hit content. If “BTS: The Return” fails to move the needle on weekly active users, the stock reaction will be muted. Investors are looking for evidence that the platform can convert casual viewers into long-term subscribers. This requires a broader strategy than relying on legacy music acts.

Consider the broader macroeconomic context. Consumer discretionary spending remains under pressure in many regions. Streaming services are among the first subscriptions consumers cancel during budget tightening. Content that commands cultural relevance, like BTS, acts as a defensive moat. It makes the service experience essential rather than optional. Wall Street Journal Market Data often reflects this sentiment in media sector analysis.

HYBE’s Valuation Multiplier and Revenue Diversification

For **HYBE Co., Ltd. (KRX: 352820)**, this release represents revenue diversification. Historically, K-Pop labels rely heavily on physical album sales and touring. Licensing deals provide high-margin revenue with minimal incremental cost. This improves the company’s overall EBITDA margins. Investors in the Korean market watch these deals closely as indicators of global brand strength.

The relationship between the label and the platform is symbiotic but tense. Netflix needs the content to retain users; HYBE needs the platform to maintain global visibility during the group’s hiatus or military service periods. This interdependence stabilizes revenue forecasts for both entities. HYBE Investor Relations data typically breaks down revenue by segment, allowing analysts to track the growth of licensing versus performance.

Expert analysis suggests that IP monetization is the future of music conglomerates.

“The value of a music catalog or artist brand is no longer just in royalties; it is in the ability to drive engagement across video, gaming, and social platforms,”

said a senior media analyst at a major investment bank during a recent sector review. This shift allows companies like HYBE to decouple growth from the physical limitations of touring schedules.

| Metric | Streaming Giant Avg. | Music Label Licensing | Impact on Deal |

|---|---|---|---|

| Content Cost | High (Production) | Medium (Licensing Fee) | Lower Risk for Streamer |

| Revenue Type | Subscription (Recurring) | License Fee (One-off/Royalalty) | Immediate Cash Flow for Label |

| Retention Value | High (If Exclusive) | Medium (Time-Limited) | Short-term Churn Reduction |

Future Market Trajectory and Investment Implications

Looking ahead, the success of “BTS: The Return” will influence future licensing deals across the industry. If engagement metrics exceed expectations, we may see a surge in similar documentaries from competitors like Amazon (NASDAQ: AMZN) Prime Video or Apple (NASDAQ: AAPL) TV+. This could drive up licensing costs for music labels, improving their margins but increasing content costs for streamers.

Investors should monitor the subsequent earnings calls for both Netflix (NASDAQ: NFLX) and **HYBE Co., Ltd. (KRX: 352820)**. Guidance updates regarding content spend and IP revenue will provide clarity on whether this model is scalable. The market rewards predictability. If this release demonstrates a reliable formula for engagement without bloating the budget, it sets a new benchmark for media valuation.

the transaction underscores the convergence of music and video streaming. The silos are breaking down. Capital is flowing to where attention resides. For the disciplined investor, the signal is clear: intellectual property that commands cross-platform attention holds the highest premium in the current economic cycle. Reuters Market Analysis supports this view on cross-sector media consolidation.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.