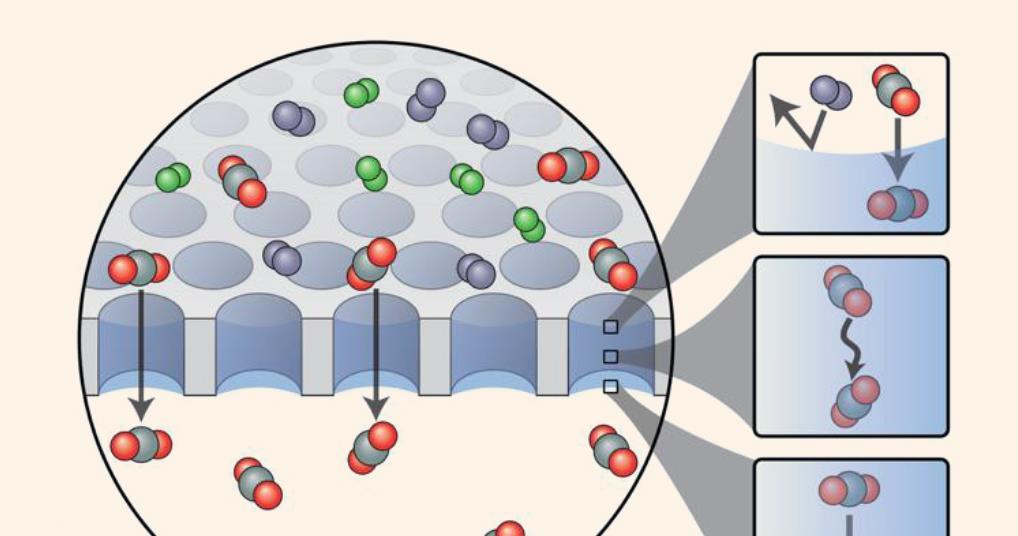

Researchers have developed a water-based membrane that selectively filters carbon dioxide from gas mixtures, potentially reducing the energy cost of carbon capture. This breakthrough addresses the “energy penalty” of traditional amine scrubbing, offering a scalable path for industrial decarbonization and enhancing the viability of carbon-to-value supply chains.

For the institutional investor, the chemistry is secondary to the cost per ton. The primary barrier to widespread Carbon Capture and Storage (CCS) adoption has not been the ability to capture CO2, but the prohibitive operational expenditure (OPEX) required to regenerate chemical solvents. By utilizing a water-based membrane that allows CO2 to wave through while blocking other gases, the industry moves from energy-intensive thermal regeneration toward a more efficient physical separation process.

The Bottom Line

- OPEX Compression: The transition from solvent-based to membrane-based capture reduces the energy penalty, directly improving the EBITDA margins of heavy industrial emitters.

- Regulatory Arbitrage: This technology enhances the profitability of the US 45Q tax credits and the EU Emissions Trading System (ETS), making carbon capture a profit center rather than a compliance cost.

- Market Disruption: Traditional chemical providers face a systemic threat as modular, membrane-based systems lower the barrier to entry for mid-sized industrial plants.

The Capex Shift from Chemical Plants to Modular Membranes

Current carbon capture infrastructure relies heavily on amine scrubbing, a process that requires massive amounts of steam to release captured CO2. This creates a parasitic load on power plants, often consuming 20% to 30% of the facility’s total energy output. Here is the math: when energy costs rise, the cost per ton of sequestered carbon increases proportionally, eroding the incentive for adoption.

The new water-based membrane approach fundamentally alters this equation. Instead of a chemical reaction that must be reversed with heat, the membrane acts as a selective filter. This allows for a modular deployment strategy. Rather than building a bespoke, multi-billion dollar chemical plant, companies like Occidental Petroleum (NYSE: OXY) can integrate these membranes into existing flue gas streams with significantly lower initial capital expenditure (CAPEX).

But the balance sheet tells a different story when we look at the “Valley of Death” for new materials. While the laboratory results are promising, the transition to industrial scale requires durability. Membranes must withstand contaminants like sulfur oxides and nitrogen oxides without degrading. If the membrane requires replacement every six months, the OPEX savings are neutralized by maintenance costs.

How 45Q Tax Credits Drive the Adoption Curve

In the United States, the Inflation Reduction Act significantly boosted the 45Q tax credit, providing up to $85 per tonne for CO2 captured and sequestered in saline aquifers. For a company like ExxonMobil (NYSE: XOM), the goal is to bring the cost of capture below this $85 threshold to generate a net positive cash flow from decarbonization.

Current amine-based systems often hover near or above this cost, depending on the gas concentration. A membrane that reduces energy consumption by even 15% could shift a project from a marginal break-even to a high-margin asset. This makes the technology highly attractive to infrastructure funds and private equity firms specializing in the energy transition.

“The scalability of carbon capture is no longer a question of chemistry, but a question of energy economics. Any technology that meaningfully reduces the parasitic load on the host plant will see rapid institutional adoption.”

This sentiment is echoed across the sector. As the International Energy Agency (IEA) notes, the deployment of CCS must accelerate sevenfold to meet 2050 net-zero targets. The bottleneck is not the desire to capture carbon, but the cost of doing so.

Competitive Pressure on Industrial Gas Giants

The emergence of highly selective membranes puts immediate pressure on the incumbents of the industrial gas sector, specifically Linde (NYSE: LIN) and Air Liquide (EPA: AI). These firms have built extensive moats around traditional gas separation and purification technologies. A shift toward water-based membranes could commoditize the capture process, stripping away the high-margin service contracts associated with solvent management.

To maintain market share, these giants are likely to pursue a strategy of aggressive M&A, acquiring the startups that hold the patents for these membrane technologies. We are entering a cycle where the intellectual property (IP) surrounding membrane permeability will be as valuable as the physical assets of the plants themselves.

The following table compares the economic profile of traditional capture versus the projected membrane-based approach:

| Metric | Amine Scrubbing (Traditional) | Water-based Membrane (Projected) | Market Impact |

|---|---|---|---|

| Energy Intensity | High (Thermal) | Low (Pressure-driven) | Lower OPEX |

| Infrastructure | Centralized/Large Scale | Modular/Scalable | Lower CAPEX |

| Waste Stream | Chemical Sludge | Minimal/Water-based | Lower Regulatory Risk |

| Cost per Ton | $60 – $120 | $30 – $70 | Increased 45Q Profit |

Macroeconomic Headwinds and the Path to Profitability

Despite the technical breakthrough, the broader macroeconomic environment remains a challenge. With interest rates remaining elevated in the first half of 2026, the cost of financing large-scale carbon capture projects is higher than it was during the 2020-2022 cycle. This makes the “modular” aspect of membrane technology even more critical, as it allows for incremental investment rather than massive, front-loaded debt.

the volatility of the EU Emissions Trading System (ETS) prices creates uncertainty. If carbon prices dip, the incentive to invest in capture technology weakens. However, the long-term trajectory remains bullish. As regulatory bodies like the SEC move toward mandatory climate-related disclosures, the pressure to reduce Scope 1 emissions will transition from a voluntary ESG goal to a fiduciary requirement.

The real winner in this scenario is not necessarily the company that discovers the membrane, but the one that can integrate it into a vertically integrated carbon-to-value chain. Whether that is converting CO2 into synthetic aviation fuels or utilizing it for enhanced oil recovery, the ability to capture carbon cheaply is the prerequisite for the entire carbon economy.

As markets open on Monday, expect a cautious but positive reaction from the industrial tech sector. The focus will shift from “can we capture carbon” to “how cheaply can we do it.” The water-based membrane has provided a definitive answer to the latter, shifting the competitive landscape in favor of those who can scale modular hardware over those who rely on legacy chemical processes.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.