Kinsale Capital Group (NASDAQ: KNSL) will release its first-quarter 2026 financial results on April 30, 2026. The announcement will detail the company’s performance within the excess and surplus (E&S) insurance market, specifically focusing on premium growth, combined ratios, and underwriting profitability amid shifting macroeconomic volatility.

For the institutional investor, the date of an earnings call is less about the calendar and more about the confirmation of a thesis. Kinsale operates as a high-efficiency engine in a sector often bogged down by legacy systems and bloated expense ratios. As the market prepares for the April 30 release, the focus is not merely on the top-line revenue, but on whether Kinsale can maintain its industry-leading combined ratio while scaling its book of business in a potentially softening E&S market.

The Bottom Line

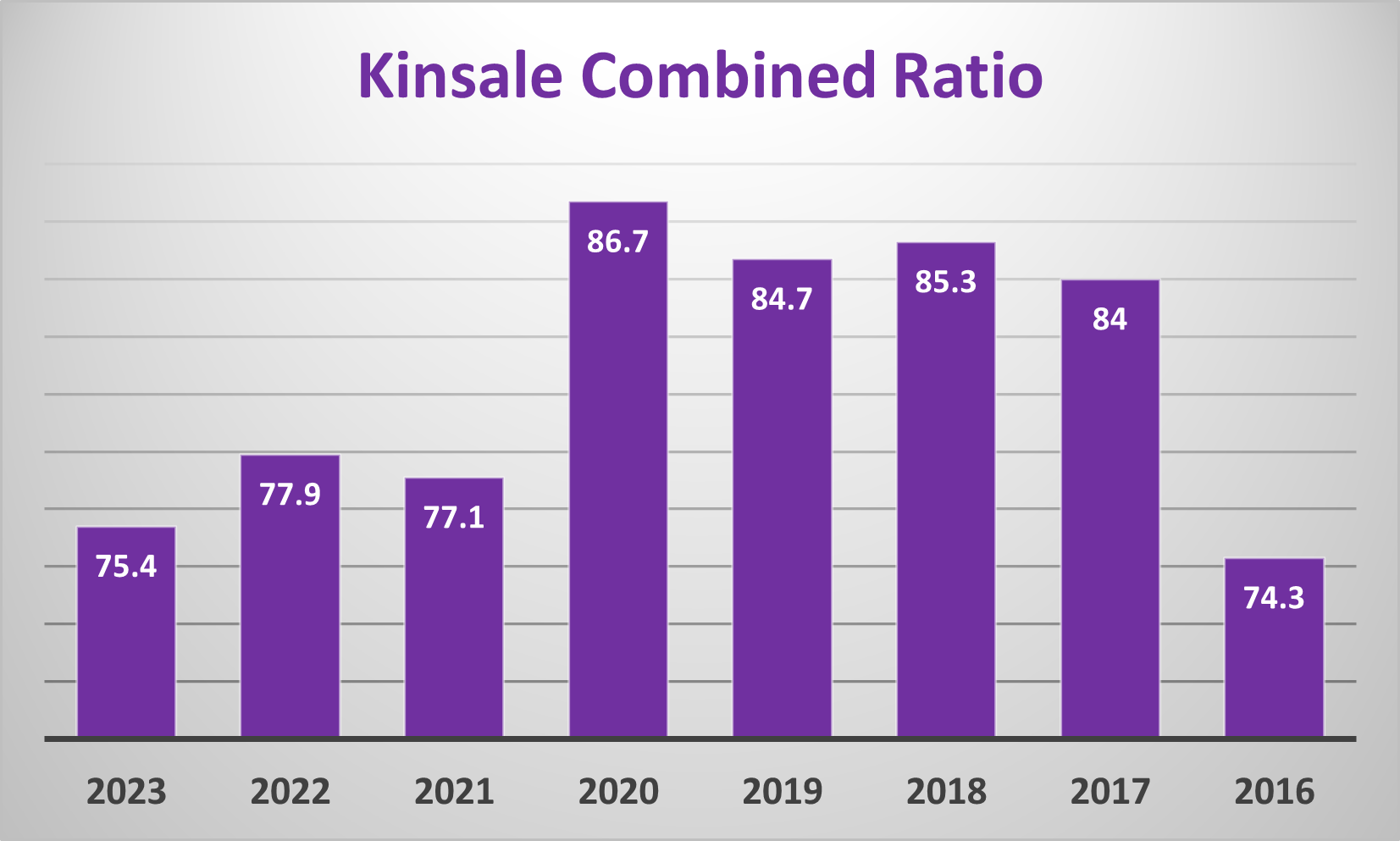

- Underwriting Discipline: Investors are hunting for a combined ratio consistently below 80%, a metric that separates Kinsale from its slower-moving peers.

- Market Cycle Positioning: The Q1 results will signal whether the “hard market” (higher premiums) in E&S insurance is persisting or if pricing power is eroding.

- Investment Income Pivot: With interest rate trajectories shifting in early 2026, the company’s fixed-income portfolio yield will be a critical secondary driver of net income.

The Efficiency Moat and the Combined Ratio Battle

To understand why the April 30 announcement carries weight, one must understand the mechanics of the E&S sector. Unlike standard insurance, E&S providers handle “non-standard” risks—the complex, the dangerous, and the unique. Most firms handle this with manual underwriting and high overhead. Kinsale, however, has built a proprietary technological stack that allows for rapid quoting and lower operational costs.

But the balance sheet tells a different story than the PR narrative. The core metric here is the combined ratio—the sum of incurred losses and expenses divided by earned premiums. A ratio under 100% indicates underwriting profit. While many competitors struggle to stay below 90%, Kinsale has historically operated in a bracket that suggests a significant competitive advantage in cost acquisition.

Here is the math: if Kinsale maintains an expense ratio near 20% while competitors average 30%, they possess a 10-point margin of safety. This allows them to either underprice competitors to gain market share or harvest higher profits on the same risk profile. According to recent SEC filings, the company’s ability to scale without a proportional increase in headcount remains its primary valuation driver.

Benchmarking Against the E&S Heavyweights

Kinsale does not operate in a vacuum. It is locked in a constant struggle for market share with established giants like W.R. Berkley (NYSE: BK) and Markel Group (NYSE: MKL). While the larger firms have more diversified portfolios, Kinsale’s purity of focus on E&S makes it a high-beta play on the specialty insurance cycle.

When markets open on Monday, analysts will be weighing Kinsale’s growth against the broader trend of “social inflation”—the rising cost of insurance claims due to increased litigation and larger jury awards. Here’s the primary headwind facing the industry in 2026. If Kinsale’s loss ratios tick upward by even 1.5%, it could trigger a re-rating of the stock’s P/E multiple.

“The critical question for specialty insurers in 2026 is not how much they can write, but how much of that premium is actually ‘permanent’ capital versus temporary cycle-driven inflation.”

This perspective is echoed by institutional analysts who track the global insurance markets, suggesting that the era of effortless premium hikes is concluding.

Projected Financial Trajectory: Q1 2025 vs. Q1 2026

While the official numbers arrive on April 30, current market data and historical growth trajectories allow for a calculated projection. The following table outlines the key metrics the market will be scrutinizing during the release.

| Metric | Q1 2025 (Actual) | Q1 2026 (Estimated) | Variance (%) |

|---|---|---|---|

| Gross Written Premiums | $740M | $835M | +12.8% |

| Combined Ratio | 76.4% | 78.1% | +1.7% (Increase) |

| Net Income | $112M | $128M | +14.3% |

| Expense Ratio | 18.2% | 18.5% | +0.3% |

Macroeconomic Headwinds and the Interest Rate Pivot

Beyond underwriting, the April 30 release will shed light on Kinsale’s investment strategy. Insurance companies are essentially investment funds that happen to sell insurance. They hold massive “float”—premiums collected but not yet paid out in claims.

For the past few years, rising interest rates provided a tailwind, increasing the yield on the short-term bonds where this float is typically parked. However, as we move through the second quarter of 2026, any signal from the Federal Reserve regarding rate cuts could compress these margins. Investors will look at the “Investment Income” line item to witness if the company has successfully locked in higher yields or if they are facing a revenue dip as older bonds mature.

Let’s look at the broader context. According to Bloomberg’s financial analysis, the specialty insurance sector is currently navigating a delicate balance between maintaining growth and avoiding “adverse selection”—the risk of taking on poor-quality business just to meet growth targets.

The Strategic Outlook for April 30

The absence of immediate conference call details in the initial announcement is standard, but the silence creates a window for speculation. The market is currently pricing Kinsale as a growth engine, but the transition from a “growth company” to a “compounding company” is often volatile.

If the Q1 results reveal a decline in the combined ratio back toward the mid-70s, expect the stock to react positively as it validates the tech-driven moat. Conversely, if the loss ratio expands due to social inflation, the narrative will shift toward whether Kinsale’s underwriting algorithms are still calibrated for the 2026 risk environment.

the April 30 earnings release will be a litmus test for the E&S industry. If the most efficient player in the game shows signs of slowing margins, it is a signal that the hard market has finally peaked. For now, the pragmatic play is to monitor the delta between written premiums and the loss ratio.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.