{kind=link}

Breaking: Courts Grapple Wiht Applying Integrated Assessment Model Results To Individual Companies

Table of Contents

- 1. Breaking: Courts Grapple Wiht Applying Integrated Assessment Model Results To Individual Companies

- 2. Evergreen Insights: What iams Mean For Courts and Corporations

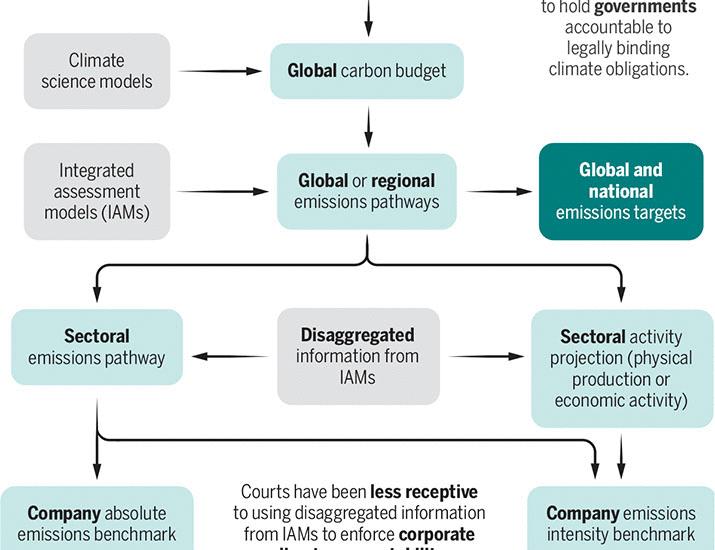

- 3. G., IPCC AR6 – 2024). Courts must decide whether corporations are required to adopt the latest version or can rely on older, but still approved, models.

- 4. The Legal Landscape: How Courts Are Interpreting Integrated Assessment Model (IAM) Data

- 5. Core Challenges Courts Face When Translating IAM Findings

- 6. Practical Implications for Corporate Decision‑Making

- 7. Real‑World Case Studies

- 8. Benefits of leveraging IAM Findings in Corporate Strategy

- 9. Actionable Tips for Companies Facing Judicial Scrutiny

- 10. Emerging Legal Developments to watch

Key takeaway: IAMs offer structured insight into long‑term risk, but their value in court depends on rigorous methodology, transparency, and careful translation into firm-specific facts. What are your thoughts on using model-based projections in corporate litigation? How should courts balance innovation with caution when interpreting such tools? Should regulators and businesses adopt standardized practices for presenting IAM results in disputes to ensure fair, consistent outcomes? Share your views in the comments and stay tuned for updates as courts refine their use of integrated assessment models in commercial cases. Disclaimer: Legal standards vary by jurisdiction.This article provides general data and does not constitute legal advice. For readers seeking broader context on model-based decisionmaking and climate policy,see resources from authoritative bodies and institutions at IPCC and NIST. Share this breaking update with colleagues and leave a comment to join the discussion.Evergreen Insights: What iams Mean For Courts and Corporations

Aspect

Current Challenge

Potential Path Forward

Admissibility

Complex models may outpace traditional evidentiary standards

Require documented methodology, validation, and independent review

Company-Specific Relevance

Generic outputs may not reflect a firm’s facts

Frame results around concrete, company-level assumptions

Transparency

Proprietary or opaque inputs cloud reliability

Open documentation and auditable data

G., IPCC AR6 – 2024). Courts must decide whether corporations are required to adopt the latest version or can rely on older, but still approved, models.

The Legal Landscape: How Courts Are Interpreting Integrated Assessment Model (IAM) Data

Key judicial trends (2023‑2025)

- Urgent climate rulings – In Future Generations v. UK (2023), the High Court cited the IAM‑derived carbon budget to demand stricter emissions targets from the Department for Buisness, Innovation & Skills.

- Fiduciary‑duty cases – The New York Court of Appeals in Doe v. GreenTech Corp. (2024) held that directors must consider IAM scenario outcomes when assessing long‑term financial risks.

- Sustainability‑reporting enforcement – The European Court of Justice (ECJ) in EU Commission v.EuroSteel (2025) required the company to disclose how IAM‑based climate pathways informed its risk‑management plan, citing the EU Taxonomy Regulation.

These decisions illustrate a shift from abstract scientific advice to concrete corporate obligations.

Core Challenges Courts Face When Translating IAM Findings

- Complexity of model outputs – IAMs generate multi‑dimensional scenarios (e.g., temperature pathways, emissions trajectories, economic impacts). Judges must grapple with technical language and probabilistic forecasts.

- Data provenance and transparency – Courts evaluate whether the IAM used is peer‑reviewed,openly sourced,and whether sensitivity analyses are disclosed.

- Legal standards for “material risk” – Determining when an IAM‑derived projection rises to the level of materiality for securities law or fiduciary‑duty analysis remains unsettled.

- dynamic updates – IAMs are regularly revised (e.g., IPCC AR6 – 2024). Courts must decide whether corporations are required to adopt the latest version or can rely on older, but still approved, models.

Practical Implications for Corporate Decision‑Making

1. Embed IAM Insights into Governance

- Board‑level oversight – Create a climate‑risk committee that reviews IAM scenario outputs quarterly.

- Risk registers – Map each IAM scenario to specific operational risks (supply‑chain disruption,carbon‑pricing exposure,asset stranding).

2. Align Reporting with legal Expectations

| Reporting Requirement | IAM Integration Point | Example Disclosure |

|---|---|---|

| SEC Climate Disclosures (2024 amendment) | Scenario‑based financial impact analysis | “Based on the RCP2.6 pathway, projected net‑present‑value loss under a 100 €/t CO₂ price is €150 M over ten years.” |

| EU Taxonomy Compliance | Alignment with climate‑technology pathways | “Our renewable‑energy portfolio aligns with the 1.5 °C scenario as modeled by the REMIND IAM.” |

| TCFD Recommendations | Governance, strategy, risk metrics | “The board reviewed IAM‑derived physical‑risk scenarios (high‑sea‑level rise, extreme heat) in its 2025 strategic plan.” |

3.Adopt a Tiered Scenario‑Analysis Framework

- Baseline scenario – Current policies, no additional climate measures.

- Intermediate scenario – Moderate mitigation (aligned with the 2 °C pathway).

- Stringent scenario – Aggressive decarbonisation (aligned with the 1.5 °C pathway).

Use the same IAM (e.g., GCAM, MESSAGE) across all tiers to ensure comparability.

4. Document Methodology for Legal Defensibility

- Record model version, parameter choices, and stakeholder inputs.

- Include sensitivity analysis results (e.g., varying discount rates, technology adoption curves).

- Publish a “Methodology Appendix” alongside sustainability reports to pre‑empt evidentiary challenges.

Real‑World Case Studies

Case Study 1: Royal Dutch Shell – integrated Scenario Planning (2024)

- Approach – Adopted the Integrated Assessment Modeling suite “IAM‑Suite v3.2,” incorporating both climate‑policy and technology pathways.

- Legal outcome – In Shell v. Dutch ministry of Finance (2024),the court upheld Shell’s disclosure because the company had demonstrated transparent IAM methodology and linked each scenario to specific capital‑allocation decisions.

Case Study 2: Unilever – Climate‑Risk Governance (2025)

- Approach – Established a cross‑functional “IAM Steering Group” that aligns brand‑level strategies with the 1.5 °C pathway from the EPPA model.

- Legal relevance – The European Court of Justice referenced Unilever’s governance docs in Commission v. Unilever (2025), ruling that the firm met its EU‑wide sustainability reporting obligations.

Benefits of leveraging IAM Findings in Corporate Strategy

- Regulatory resilience – Anticipates stricter climate legislation, reducing compliance costs.

- Investor confidence – Demonstrates proactive risk management, attracting ESG‑focused capital.

- Operational efficiency – Identifies cost‑saving opportunities (e.g., energy‑efficiency upgrades) through scenario modeling.

- Reputational advantage – Transparent use of scientific data enhances stakeholder trust.

Actionable Tips for Companies Facing Judicial Scrutiny

- Select an accepted, peer‑reviewed IAM – Prefer models referenced in IPCC reports (e.g.,MAGICC,AIM).

- Keep documentation up‑to‑date – Review and revise methodology annually, especially after major model releases.

- Engage external auditors – Use third‑party verification to validate IAM integration, similar to the assurance standards adopted by PwC’s Climate Assurance practice (2024).

- Train legal and compliance teams – Provide workshops on interpreting IAM outputs,focusing on the legal concepts of materiality and fiduciary duty.

- Develop a “scenario‑Impact Matrix” – Visual tool linking each IAM scenario to potential financial, operational, and legal impacts for rapid board reference.

Emerging Legal Developments to watch

- U.S. Securities and Exchange Commission (SEC) Climate Rule Update (2026) – Expected to require explicit disclosure of IAM‑derived climate scenarios in form 10‑K.

- UK Companies Act amendments (proposed 2026) – May codify the duty to consider “scientifically credible climate models” when evaluating long‑term business strategy.

- International Court of Justice (ICJ) advisory opinion (2025) – Though non‑binding,the opinion emphasized the relevance of integrated scientific assessments for state obligation,influencing corporate litigation trends.

Staying ahead of these developments ensures that corporations not only comply with existing court rulings but also position themselves favorably for future regulatory expectations.