{kind=link}

Dismissing Doomsday: Why Fears of a Dollar Collapse might potentially be Overblown

Table of Contents

- 1. Dismissing Doomsday: Why Fears of a Dollar Collapse might potentially be Overblown

- 2. The Misconception of ‘printing Money’

- 3. Deficits and Surpluses: Two sides of the Same Coin

- 4. The Dollar’s Resilience and Gold’s Limitations

- 5. Focus on Fundamentals, Not Fear

- 6. Evergreen Insights for Long-Term Investors

- 7. Frequently Asked Questions

- 8. How has the stability of the velocity of money impacted the reliability of the quantity theory of money as a predictor of inflation?

- 9. Evaluating the Money Supply Growth Thesis: Unveiling Critical Flaws in Economic Predictions

- 10. The Past Appeal of Monetary Policy & Money Supply

- 11. The Velocity of Money Problem: A shifting Landscape

- 12. The Role of Global Factors & Disinflationary Pressures

- 13. The Impact of Financial Innovation & Digital Currencies

- 14. Case Study: JapanS Lost Decades & Negative Interest Rates

- 15. Beyond M2: Alternative Inflation Indicators

New York, NY – October 24, 2025 – Prominent financial figures have recently cautioned Investors too flee the US dollar and embrace hard assets like Gold and Bitcoin, citing escalating deficits and increased money printing. However, detailed economic analysis suggests these concerns might be misconstrued, and a collapse of the dollar is far from inevitable.

The Misconception of ‘printing Money’

Recent commentary frequently assumes that a growing money supply automatically devalues the US dollar and fuels inflation, positioning Gold and Bitcoin as safe havens.This reasoning, however, reverses the causal relationship.Modern economies operate on an ‘endogenous money system,’ where banks generate funds in response to economic demands.As clarified by the Bank of england in a 2014 study, broad money growth is driven by commercial banks extending credit when viable opportunities arise, not by direct central bank control.Essentially, loans create deposits.

The United States does not simply ‘print’ money; all money is created through lending. Consequently,money supply growth closely mirrors economic activity. Expanding businesses,increased hiring,and investment lead to credit expansion and a corresponding growth in the money supply. Conversely, a slowing economy and reduced loan demand curtail money supply growth, irrespective of Federal Reserve actions. This was notable after the 2008 financial crisis, where quantitative easing failed to stimulate significant money growth due to banks hoarding reserves.

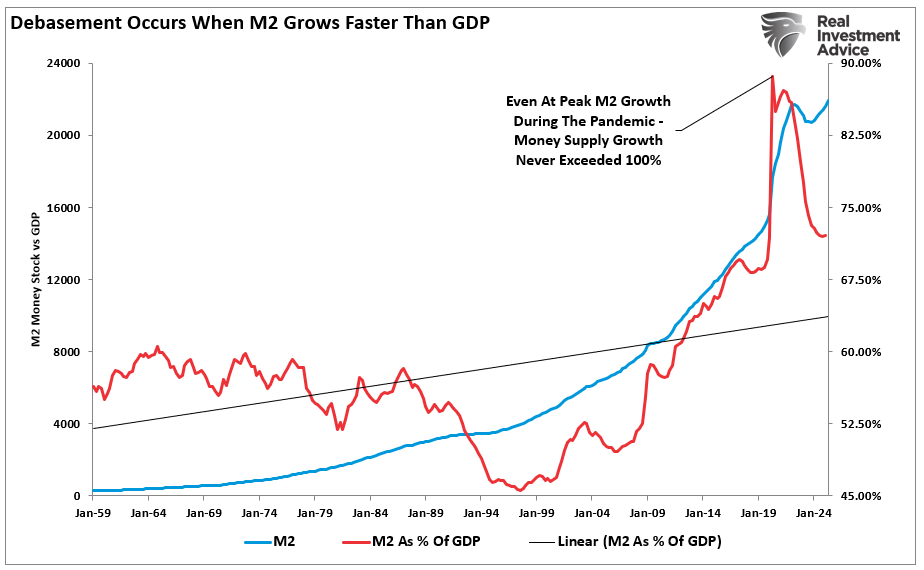

A healthy money supply grows alongside a healthy economy to prevent deflation. Recent data shows that the M2 money supply as a percentage of GDP has been decreasing, not increasing.

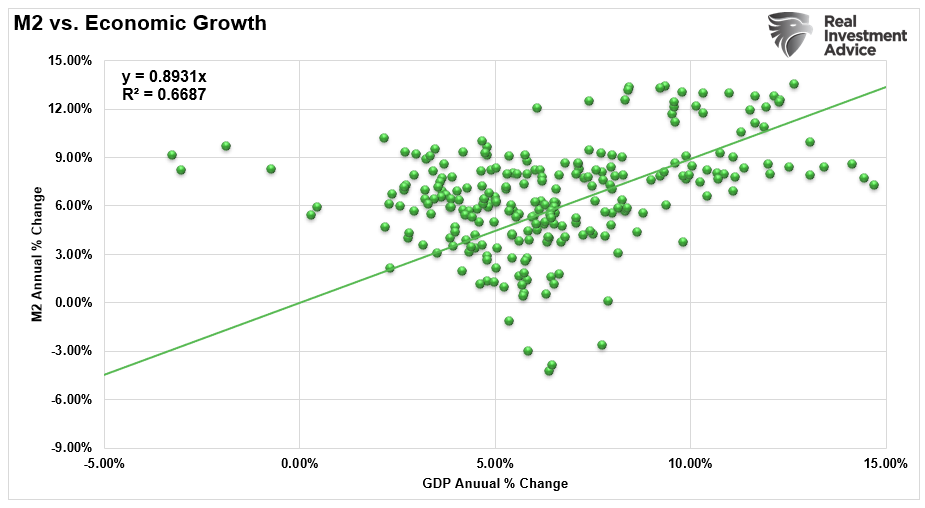

The correlation between M2 growth and the overall economy is remarkably strong, as illustrated below.

Deficits and Surpluses: Two sides of the Same Coin

The narrative surrounding government deficits often overlooks a crucial accounting principle: one sector’s deficit is invariably another’s surplus. When the government runs a deficit, those dollars ultimately become net financial assets in the private sector. This dynamic played out vividly during 2020 and 2021, when unprecedented government spending and stimulus checks pushed household savings rates to a record 33%, bolstering private wealth and fueling subsequent economic recovery.

Government deficits aren’t necessarily detrimental; rather, they fund spending that becomes income for households and businesses, promoting economic activity. Furthermore, amidst recessions, deficits can stabilize the economy by providing liquidity and balance sheet relief to the private sector. US Treasury bonds, often dismissed as “worthless paper,” are among the most sought-after safe assets globally.They underpin global finance, serving as collateral, offering security, and providing yield, thus reinforcing, rather than eroding, the dollar’s international role.

| Sector | 2023 Balance (trillions of USD) |

|---|---|

| Government | -2.0 |

| Private Sector | +2.0 |

| Foreign Sector | 0.0 |

Did You Know? The United States dollar is used in approximately 88% of global foreign exchange transactions, 58% of international reserves, and 54% of global trade, demonstrating its continued dominance.

The Dollar’s Resilience and Gold’s Limitations

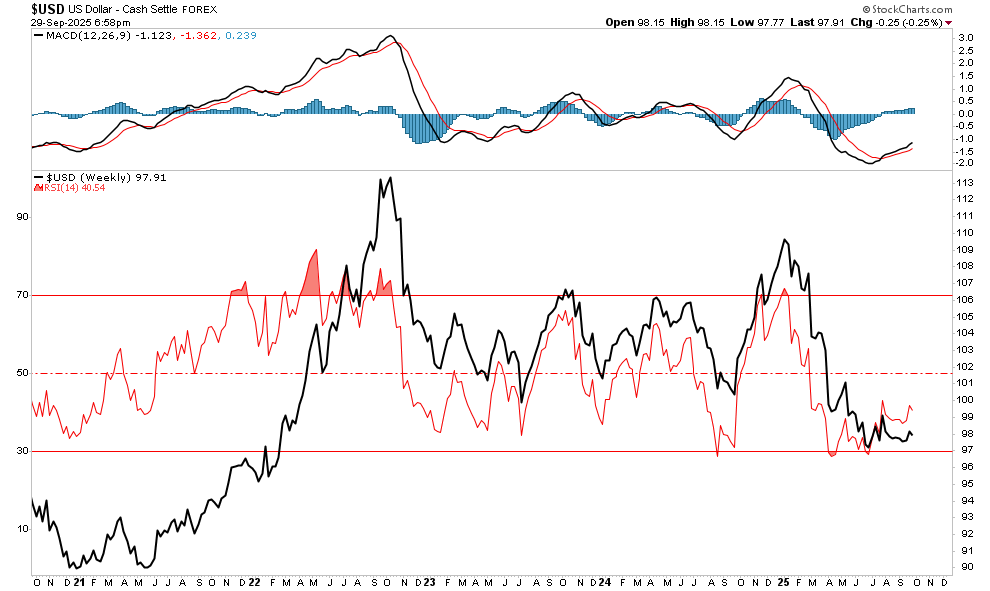

Even if deficits and rising money supply were inflationary, the argument for gold’s surge hinges on the dollar’s performance. Gold is priced in US dollars, and historically, it weakens when the dollar strengthens and real interest rates increase. The opportunity cost of holding gold, which doesn’t yield income, increases with rising real rates because investors can earn a return elsewhere. A stronger dollar also makes gold more expensive for international buyers, curbing demand.

Factors that could propel the US dollar include stronger US economic growth compared to Europe and Asia, a comparatively hawkish Federal Reserve stance, and a flight to safety during global economic uncertainty. The technical indicators also suggest a possible rally with the US Dollar Index having reversed from extreme overbought conditions in 2022, and large speculative short positions are at levels that could lead to cover-driven rallies.

Such a dollar rally would likely reverse gold prices, as gold and the dollar share a negative correlation.

pro Tip: Monitor real interest rates and the US dollar index alongside gold prices for a more accurate assessment of the precious metal’s potential.

Focus on Fundamentals, Not Fear

Calls to rush into Gold, Silver, and Bitcoin are attention-grabbing, but they oversimplify financial realities. Money supply growth reflects economic expansion, deficits fuel private sector savings, and gold’s prospects are tied to the dollar and real rates. Investors should prioritize basic analysis over fear-driven narratives. The US dollar remains the world’s reserve currency, supported by strong capital markets and legal frameworks. Unless another currency emerges as a viable choice, the dollar is poised to remain central to the global financial system.

What role do you believe the US dollar will play in the global economy over the next decade? Are alternative assets a sound long-term investment strategy, or are they overhyped?

Evergreen Insights for Long-Term Investors

- Track Key Indicators: Monitor the interplay between economic growth, money supply, and real interest rates.

- Diversify Strategically: Utilize Gold, Silver, and Bitcoin as diversifying tools, not core holdings.

- Assess Debt Sustainability: Evaluate whether fiscal policies support long-term, sustainable economic growth.

Frequently Asked Questions

- what is the primary driver of money supply growth? Money supply growth is primarily driven by economic activity and lending practices, not simply by central bank actions.

- Are government deficits always harmful? Government deficits can be beneficial by funding economic activity and supporting private sector savings.

- How does the US dollar impact gold prices? Gold prices typically weaken when the US dollar strengthens and real interest rates rise.

- What is the endogenous money system? This is a system where banks create money in response to economic demand, rather than being dictated by central banks.

- What is the importance of M2 as a percentage of GDP? This metric helps assess whether money supply growth is aligned with economic output.

- Is a US dollar collapse likely? While concerns exist, a complete collapse of the dollar appears unlikely given its continued dominance in global finance.

Share this article with your network and let us know your thoughts in the comments below!

How has the stability of the velocity of money impacted the reliability of the quantity theory of money as a predictor of inflation?

Evaluating the Money Supply Growth Thesis: Unveiling Critical Flaws in Economic Predictions

The Past Appeal of Monetary Policy & Money Supply

For decades, the relationship between money supply growth and inflation has been a cornerstone of economic thought. The quantity theory of money, popularized by Milton Friedman, posited a direct correlation: increasing the money supply leads to rising prices. This idea gained traction, especially during the inflationary periods of the 1970s, and became a key tenet for many central banks.Understanding monetary aggregates – M0,M1,M2,and M3 – was crucial for forecasting economic trends. However, the post-2008 financial crisis and the subsequent era of quantitative easing (QE) have thrown this thesis into serious doubt. The simple equation of exchange (MV=PQ, where M is money supply, V is velocity of money, P is price level, and Q is real output) doesn’t always hold.

The Velocity of Money Problem: A shifting Landscape

The core flaw in relying solely on money supply growth as a predictor of inflation lies in the instability of the velocity of money (V). Velocity represents how quickly money changes hands in the economy.

* Pre-2008: velocity was relatively stable, allowing central banks to reasonably predict inflation based on money supply changes.

* Post-2008: Velocity plummeted. Despite massive increases in the money supply through QE programs – designed to stimulate the economy – inflation remained stubbornly low. This was as banks hoarded reserves rather of lending, and consumers and businesses saved rather than spent.

* The COVID-19 Pandemic: A temporary surge in velocity occurred with stimulus checks, but this proved short-lived.

This demonstrates that simply increasing the money supply doesn’t automatically translate into inflation if money isn’t circulating actively. Monetary velocity is now a far more complex and unpredictable variable.

The Role of Global Factors & Disinflationary Pressures

Focusing solely on domestic money supply growth ignores the notable impact of globalization and structural disinflationary forces.

* Global Supply Chains: The integration of global supply chains, particularly with the rise of China, created downward pressure on prices. Cheap imports dampened inflationary pressures, even with expanding monetary policy.

* Technological Disruption: Technological advancements, particularly in areas like computing and interaction, have led to increased productivity and lower costs, contributing to disinflation.

* Demographic Shifts: Aging populations in many developed countries have led to lower consumption and investment, further suppressing demand-pull inflation.

* Debt Levels: High levels of private and public debt can act as a drag on economic activity, limiting the inflationary impact of money supply increases.

These factors demonstrate that inflation is a global phenomenon influenced by forces beyond the control of any single central bank or monetary policy.

The Impact of Financial Innovation & Digital Currencies

The evolution of the financial system itself complicates the relationship between money supply and inflation.

* Shadow Banking: The growth of the shadow banking system – non-bank financial intermediaries – creates credit outside the traditional banking system,making it harder to accurately measure the money supply.

* Digital Currencies: The emergence of cryptocurrencies and central bank digital currencies (CBDCs) introduces new forms of money and payment systems, possibly altering the velocity of money and the effectiveness of monetary policy.

* Fintech Lending: Online lending platforms and other fintech innovations are disrupting traditional banking, further blurring the lines of credit creation and money supply.

These innovations require a re-evaluation of how we define and measure monetary aggregates in the 21st century.

Case Study: JapanS Lost Decades & Negative Interest Rates

Japan provides a compelling case study of the limitations of the money supply growth thesis. For decades, the Bank of Japan has pursued aggressive monetary easing, including zero and negative interest rates and massive asset purchases, yet Japan has struggled with deflation and stagnant growth. This demonstrates that even extremely expansionary monetary policy can fail to generate inflation in the face of structural economic problems and low demand. The experience highlights the importance of considering factors beyond money supply when assessing inflationary risks.

Beyond M2: Alternative Inflation Indicators

Given the flaws in relying solely on money supply growth,economists are increasingly turning to alternative indicators to gauge inflationary pressures.

* Producer Price Index (PPI): Measures the change in prices received by domestic producers, providing an early warning signal of potential inflation.

* Core Inflation: Excludes volatile food and energy prices, offering a more stable measure of underlying inflationary trends.

* Inflation Expectations: Surveys of consumers and businesses reveal their expectations for future inflation, which can influence actual price-setting behavior.

* Wage Growth: Rising wages can indicate increasing demand and potential inflationary pressures.

* Supply Chain Bottlenecks: Monitoring disruptions in global supply chains can provide insights into potential price increases.

These indicators offer a more nuanced and complete view of the inflationary