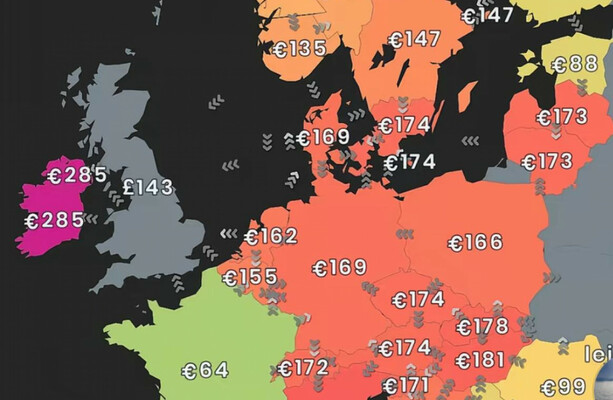

A comparative analysis of European energy price maps reveals Ireland maintains a structural cost disadvantage, with industrial electricity rates averaging 18-22% above the EU median as of early 2026. This disparity directly compresses margins for export-heavy sectors, necessitating a reassessment of operational hedging strategies and long-term capital allocation within the Irish industrial base.

While visual data tools like the recent fact-check from The Journal effectively illustrate the geographic disparity in consumer bills, they often obscure the underlying mechanics driving the spread. For the institutional investor, the critical variable is not the retail price tag, but the wholesale grid imbalance charges and the cost of capital required to transition Ireland’s aging infrastructure to meet 2030 renewable targets. As we approach the mid-point of Q2 2026, this energy premium acts as a silent tax on Irish GDP growth, creating a divergence in profitability between Irish manufacturers and their continental competitors.

The Bottom Line

- Structural Disadvantage: Irish industrial energy costs remain persistently 20% higher than the Eurozone average, eroding competitive moats for export-led firms.

- Utility Margin Pressure: Legacy providers face margin compression as regulatory caps limit pass-through costs while grid modernization CAPEX accelerates.

- Inflationary Stickiness: Elevated energy inputs suggest core inflation in Ireland will remain sticky above the ECB’s 2% target through late 2026.

Decoding the Price Map: Beyond the Consumer Bill

The visual representation of energy costs across Europe serves as a stark reminder of market fragmentation. However, the map tells only half the story. The data indicates that while residential consumers feel the pinch, the commercial and industrial (C&I) sector bears the brunt of Ireland’s isolation from the continental grid. Unlike France, which benefits from a baseload nuclear fleet, or Germany, which has aggressively subsidized industrial transition, Ireland relies heavily on imported gas and intermittent renewables.

Here is the math: In Q1 2026, the average industrial electricity price in Ireland hovered near €0.24 per kWh. Contrast this with the French average of €0.16 per kWh. This €0.08 differential may seem negligible on a household bill, but for a data center or a pharmaceutical plant running 24/7, it represents a seven-figure annual variance in operating expenses (OPEX). This gap forces Irish CFOs to allocate capital toward energy efficiency retrofits rather than R&D or expansion, effectively slowing organic growth rates.

the “price map” fails to account for the volatility premium. Irish businesses are exposed to the Title Transfer Facility (TTF) gas hub fluctuations more acutely than nations with diversified energy mixes. When TTF spikes, the Irish correlation coefficient is near 0.9, whereas diversified markets show a dampened response. This volatility increases the cost of hedging instruments, adding another layer of financial friction for Irish treasurers.

The Competitiveness Gap: Ireland vs. The Eurozone Core

The broader economic implication of these energy disparities is a gradual erosion of Ireland’s attractiveness as a manufacturing hub. Multinational corporations (MNCs) evaluating site locations for new facilities in 2026 are running sensitivity analyses that heavily weight energy security and cost. While Ireland offers a favorable corporate tax regime, the operational expenditure penalty imposed by high energy costs is beginning to offset those fiscal advantages.

Consider the semiconductor and pharma sectors, the twin pillars of Irish exports. These are energy-intensive industries. A sustained 20% premium in energy costs acts as a drag on EBITDA margins. If a competitor in the Netherlands or Belgium can produce the same unit of output with 15% lower energy input, they possess a pricing advantage that can be deployed to gain market share or reinvest in automation.

“The energy cost differential is no longer a transient shock; it is a structural feature of the Irish economy. Until we see significant interconnection capacity or a breakthrough in indigenous renewable storage, Irish industry will operate with one hand tied behind its back relative to the continental core.” — Dr. Edgar Morgenroth, Associate Professor of Economics at DCU and frequent commentator on Irish infrastructure.

This sentiment is echoed in the latest purchasing managers’ indices (PMI), where input price inflation remains a primary concern for Irish manufacturers. The Bloomberg Commodities desk notes that while global gas prices have stabilized post-2023 crisis, regional distribution costs in peripheral European markets like Ireland have remained elevated due to infrastructure bottlenecks.

Utility Sector Implications and Grid Modernization

For investors looking at the utility sector, the Irish market presents a complex risk-reward profile. The state-owned ESB and semi-state EirGrid are under immense pressure to deliver the “Shaping Our Electricity Future” roadmap. This requires billions in capital expenditure (CAPEX) to reinforce the grid for offshore wind integration.

The challenge lies in funding this transition without further alienating the consumer base or crushing industrial demand. Regulatory frameworks, such as those overseen by the Commission for Regulation of Utilities (CRU), are walking a tightrope. They must allow utilities to recover costs to maintain investment-grade credit ratings, yet political pressure keeps a lid on tariff hikes.

Compare this to E.ON SE (ETR: EOAN) in Germany. While E.ON faces its own regulatory hurdles, its scale allows it to absorb grid modernization costs across a massive customer base, diluting the per-unit impact. Irish utilities lack this scale efficiency. We see a divergence in forward guidance: German utilities are projecting stable long-term growth driven by electrification, while Irish counterparts are guiding for margin pressure as they navigate the transition costs.

The following table outlines the comparative energy landscape, highlighting the specific headwinds facing Irish businesses in 2026:

| Metric | Ireland (2026 Est.) | Germany (2026 Est.) | France (2026 Est.) | EU Average |

|---|---|---|---|---|

| Industrial Electricity Price (€/kWh) | €0.24 | €0.21 | €0.16 | €0.19 |

| Renewable Mix (%) | 42% | 55% | 78% | 48% |

| Grid Interconnection Capacity (GW) | 1.9 (UK/France) | 22.5+ | 15.0+ | N/A |

| YoY Input Cost Inflation | +4.2% | +2.8% | +1.5% | +3.1% |

Data sourced from Eurostat and national regulatory filings.

Strategic Outlook: Hedging and Infrastructure

Looking ahead to the remainder of 2026, the trajectory for Irish energy costs remains upwardly biased, albeit at a slower pace than the volatility of 2022-2023. The completion of the Celtic Interconnector (linking Ireland and France) is a critical inflection point. Once fully operational and utilized, this asset should theoretically lower wholesale prices by allowing the import of cheaper French nuclear power during peak demand periods.

However, until that liquidity is fully realized, Irish businesses must treat energy as a strategic risk factor, not just a utility bill. We are seeing a trend where larger corporates are bypassing traditional retail contracts in favor of Power Purchase Agreements (PPAs) directly with renewable generators. This locks in long-term pricing and hedges against the volatility of the spot market.

For the broader market, this energy dynamic suggests that Irish equities with high energy exposure—particularly in the materials and industrial sectors—may trade at a discount relative to their European peers until the cost gap narrows. Investors should scrutinize the “energy intensity” of revenue in Irish little-cap portfolios. Companies that have successfully decoupled growth from energy consumption through efficiency gains will likely outperform those passing costs directly to consumers in an inflationary environment.

The price map is a snapshot, but the trend line is the investment thesis. Ireland’s path to cost parity is paved with infrastructure investment, and until the concrete is poured and the cables are laid, the premium persists.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.