Dutch energy consumers are seeing a significant reduction in costs as natural gas prices decline in April 2026. Market analysts suggest this price floor presents a strategic window for households and businesses to lock in fixed-rate contracts to hedge against future volatility in the European energy sector.

The current dip in gas prices is not merely a seasonal fluctuation; it is a reflection of shifting geopolitical risk premiums and a stabilizing supply chain across the EU. For the average consumer, the immediate effect is lower monthly bills. For the investor and the business owner, though, this is a question of timing and risk management. The volatility of the Title Transfer Facility (TTF) gas futures—the primary benchmark for European gas—continues to dictate the pricing strategies of major utilities.

The Bottom Line

- Hedging Opportunity: Current price troughs offer a low-cost entry point for fixed-term contracts, mitigating the risk of winter price spikes.

- Inflationary Pressure: Lower energy inputs act as a deflationary force, potentially easing the burden on energy-intensive industrial sectors.

- Market Sentiment: The shift toward fixed contracts indicates a consumer preference for stability over the gamble of variable-rate “spot” pricing.

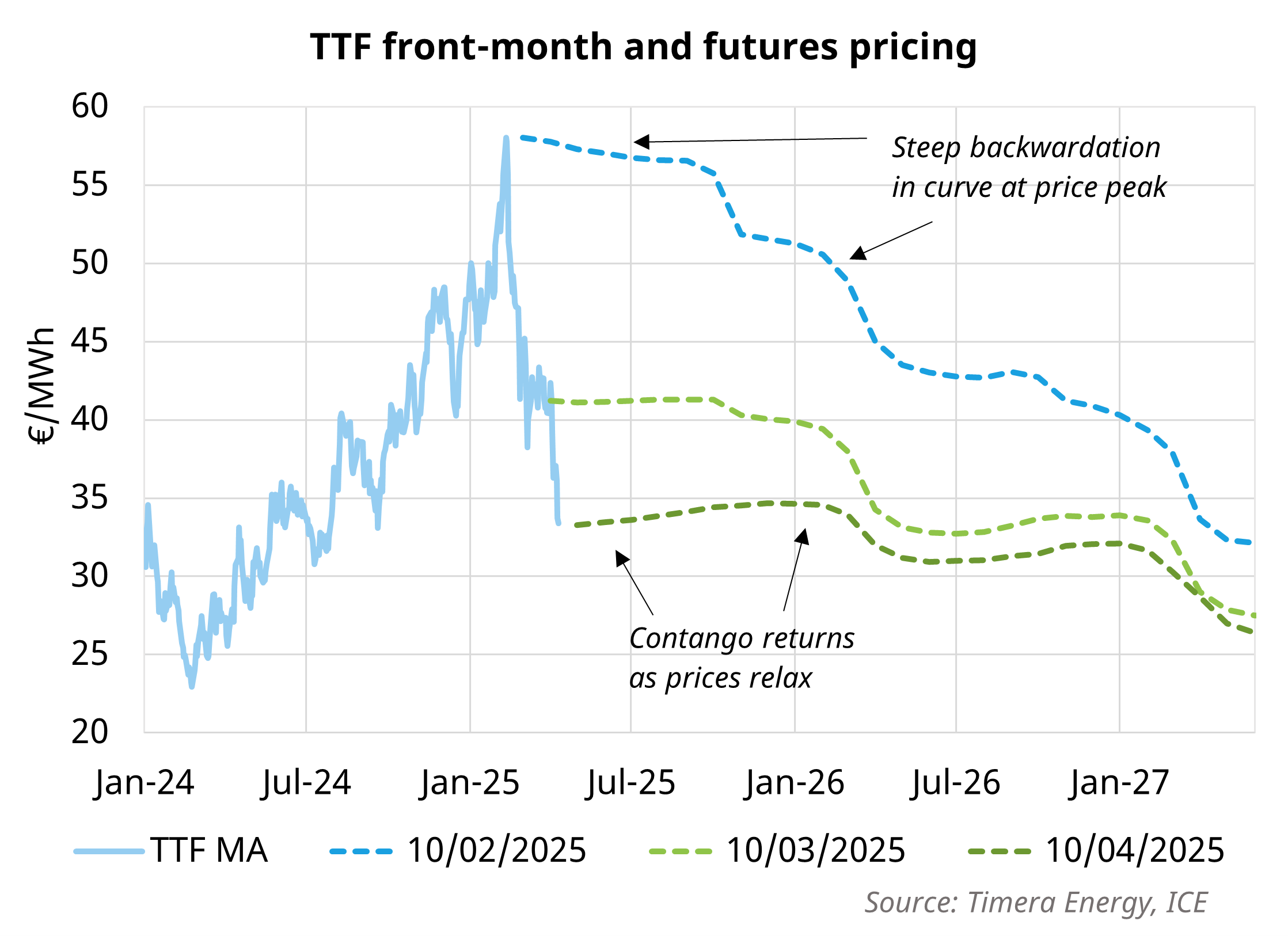

The Mechanics of the TTF Price Floor

To understand why energy providers are slashing rates today, one must look at the Bloomberg Commodity Index and the TTF futures market. When gas prices “bottom out,” utilities reduce their forward-looking risk premiums, allowing them to offer more competitive fixed rates to attract market share.

But the balance sheet tells a different story. While consumers witness a “discount,” providers are managing their own hedge books. If a provider locks in too many customers at a low fixed rate and prices suddenly pivot upward due to a supply shock, the provider faces significant margin compression. Here is the math: a 10% increase in wholesale gas costs without a corresponding hedge can erase the net profit margin of a mid-sized energy retailer almost overnight.

This dynamic is particularly relevant for companies like **Shell (NASDAQ: SHEL)** and **TotalEnergies (NYSE: TTE)**, which operate integrated models. They can absorb wholesale volatility better than “pure-play” retailers who simply buy and resell energy.

Industrial Implications and Macroeconomic Ripple Effects

Energy costs are a primary input for the manufacturing sector. When gas prices decline, the cost of production for chemicals, fertilizers, and glass drops. This creates a ripple effect throughout the supply chain, potentially lowering the Producer Price Index (PPI) and, eventually, the Consumer Price Index (CPI).

However, the “fixed contract” advice is not without risk. If a consumer locks in a contract today and prices continue to decline throughout 2026, they will be paying a premium over the spot price. But in the current macroeconomic climate, the cost of “insurance” (the slightly higher fixed rate) is generally viewed as preferable to the risk of a 2022-style energy crisis.

“The transition from volatile spot pricing to structured fixed contracts is a signal of market maturity. Investors are no longer betting on a permanent decline in energy costs, but are instead pricing in a ‘latest normal’ of managed volatility.”

— Analysis attributed to institutional energy strategists monitoring the EU energy transition.

Comparative Analysis: April 2026 Energy Trends

The following data represents the estimated impact of the current price shift on various contract types based on market trends observed in the first half of April 2026.

| Contract Type | Estimated Price Change (YoY) | Risk Profile | Strategic Recommendation |

|---|---|---|---|

| Variable (Spot) | -12.4% | High | Avoid for long-term budgeting |

| Fixed (1-Year) | -8.2% | Low | Optimal for risk-averse users |

| Fixed (3-Year) | -4.1% | Medium | Hedge against long-term volatility |

The Regulatory Shadow: ACER and the EU Market

The European Union’s Agency for the Cooperation of Energy Regulators (ACER) continues to monitor how utilities pass through wholesale savings to the finish consumer. There is persistent tension between the need for utilities to remain solvent and the political pressure to ensure “fair” pricing for citizens.

If regulators determine that providers are lagging in passing down price drops, we could see a wave of mandated tariff adjustments. This creates a precarious environment for utility stocks. For instance, if a regulatory body forces a price ceiling, the EBITDA of the affected energy firms will capture a direct hit, potentially leading to a downward revision of forward guidance.

the push toward renewables is fundamentally changing the demand curve for natural gas. As more industrial players shift to hydrogen or electrification, the long-term demand for gas may structurally decline, which would keep prices lower but make the infrastructure “stranded assets.”

Strategic Outlook: The Path Forward

For the business owner, the decision to move to a fixed contract is a decision about capital allocation. By fixing energy costs, a company removes a variable from its operational expenditure (OpEx), allowing for more accurate forecasting and better margins on their own products.

Looking ahead to the close of Q2 2026, keep a close eye on Reuters Commodity reports. Any sign of renewed instability in the East Mediterranean or unexpected outages in Norwegian pipelines will cause the “fixed rate” window to slam shut rapidly.

The pragmatic play is clear: the current price dip is a tactical advantage. Those who wait for the “absolute bottom” often find themselves buying back in at the peak of a sudden recovery. In the world of energy trading, certainty is the most valuable commodity of all.