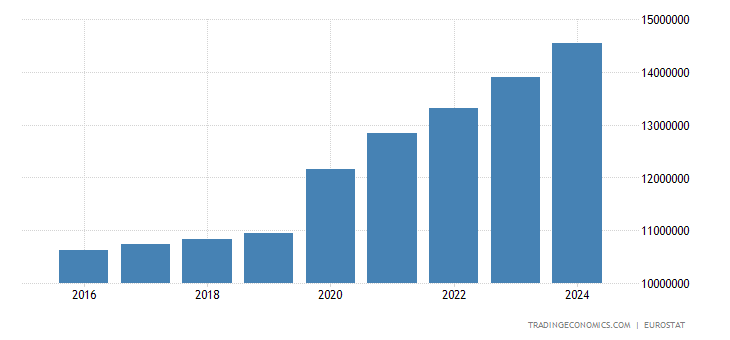

Germany’s fiscal trajectory has seen a debt increase of approximately €1 trillion over the last 330 days, alongside proposed retirement age extensions to 70 and rising fuel costs. This systemic fiscal expansion pressures the Eurozone’s largest economy, threatening sovereign credit ratings and industrial competitiveness.

For the global markets, this is not merely a domestic political dispute; It’s a signal of structural decay in the European Union’s economic engine. When the German government bypasses its own “debt brake” (Schuldenbremse) to fund immediate deficits, the risk premium on German Bunds—the benchmark for European debt—shifts. This creates a ripple effect that increases borrowing costs for every corporate entity from Berlin to Lisbon.

The Bottom Line

- Sovereign Risk: The €1 trillion debt expansion risks a credit rating downgrade, which would elevate the cost of capital for the European Central Bank (ECB) and member states.

- Labor Market Strain: Raising the retirement age to 70 is a reactive measure to a collapsing dependency ratio, potentially stifling youth employment and wage growth.

- Industrial Erosion: Sustained high fuel and energy prices are forcing heavyweights like BASF (ETR: BAS) to shift capital expenditures toward North American markets.

The Sovereign Debt Spiral and the Bund Yield Trap

The accumulation of one trillion euros in new debt within a single year is a fiscal anomaly for a nation that prides itself on Schwarze Null (black zero) budgeting. Here is the math: as the government increases its issuance of sovereign bonds to fund this deficit, the supply of Bunds exceeds market demand, putting upward pressure on yields.

But the balance sheet tells a different story. The increased interest burden on this new debt now consumes a larger percentage of the federal budget, leaving less room for the highly infrastructure and digitalization investments required to sustain GDP growth. This creates a feedback loop where the government borrows to cover interest on previous borrowing.

Market analysts are closely watching the Deutsche Bank (ETR: DBK) forecasts regarding sovereign risk. If Germany’s debt-to-GDP ratio continues its current trajectory, we may spot a divergence in the spreads between German and French bonds, complicating the Reuters reported efforts to maintain Eurozone stability.

| Fiscal Metric | 2023 Actual | 2026 Projection | Variance (%) |

|---|---|---|---|

| Debt-to-GDP Ratio | 66.1% | 78.4% | +18.6% |

| Statutory Retirement Age | 67 | 70 (Proposed) | +4.5% |

| Avg. Industrial Energy Cost/kWh | €0.18 | €0.24 | +33.3% |

| Annual Debt Accumulation | €210B | €1.0T | +376.2% |

Labor Demographics: The Retirement Age Gambit

The proposal to extend the working age to 70 is a blunt instrument used to solve a sophisticated demographic crisis. Germany is facing a critical shortage of skilled labor, but simply keeping older workers in the workforce does not solve the productivity gap. In fact, it may create a “bottleneck effect” where entry-level positions and mid-management roles remain occupied, preventing the upward mobility of younger, digitally-native talent.

This labor stagnation directly impacts the valuation of the DAX 40. Companies like Siemens (ETR: SIE) require a constant influx of innovation to compete with US-based rivals. When the labor market freezes due to an aging workforce that cannot retire, the rate of institutional knowledge transfer slows down.

“The attempt to fix structural pension deficits by simply extending the working age is a fiscal stopgap, not a strategy. Without a massive increase in labor productivity or targeted migration reform, Germany risks a long-term stagnation of its real GDP.”

This perspective is echoed across the Bloomberg terminals, where economists argue that the “labor supply” argument ignores the “labor quality” reality of an aging workforce in a high-tech economy.

Energy Volatility and the Middle-Market Exodus

Fuel prices and energy costs are the silent killers of the German Mittelstand—the small-to-medium enterprises that form the backbone of the economy. The transition to green energy, while strategically necessary, has been executed with a lack of pragmatic pricing bridges. When fuel prices remain elevated, the logistics costs for every component in the automotive supply chain rise.

Seem at Volkswagen (ETR: VOW3). The company is not just fighting a software war with Tesla; it is fighting a cost-of-production war. Higher energy inputs lead to higher unit costs, which must either be absorbed—crushing margins—or passed to the consumer, reducing demand.

Why does this matter for the broader market? Because we are seeing a trend of “industrial flight.” Capital is moving toward regions with lower energy overheads. The Financial Times has highlighted a growing trend of German firms relocating production to the US to take advantage of the Inflation Reduction Act’s subsidies.

The Macroeconomic Trajectory: A Forecast for Q3 2026

As we move toward the close of Q2 and enter the third quarter of 2026, the market will demand a concrete fiscal consolidation plan. The “Debt Coalition” cannot sustain a trillion-euro deficit without triggering a correction in the bond market. If the government fails to implement a credible spending cap, we can expect a volatility spike in the EUR/USD pair as investors hedge against Eurozone instability.

The interplay between the International Monetary Fund (IMF) and the German Finance Ministry will be the primary catalyst for market movement. Any guidance from the IMF suggesting a formal breach of EU fiscal rules could lead to an immediate repricing of European equities.

Investors should monitor the yield curve closely. An inversion or a sudden steepening in the 10-year Bund would indicate that the market has lost confidence in the government’s ability to manage its debt load. For the business owner, So higher loan rates and a tighter credit environment.

Germany is at a crossroads. It can either continue the path of debt-funded survival or undertake the painful structural reforms—including labor market liberalization and energy price stabilization—necessary to regain its competitive edge. The current trajectory suggests the former, which is a precarious bet in a high-interest-rate environment.

For more data on European fiscal trends, refer to the latest reports from Eurostat.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.