{kind=link}

Global Investment Landscape: Navigating Headwinds and the Rise of AI in 2025

A chilling statistic emerged this year: global foreign direct investment (FDI) fell 3% in the first half of 2025, extending a two-year slump. But beneath the surface of this downturn, a critical shift is underway. While geopolitical tensions and economic uncertainty continue to weigh on traditional investment avenues, a surprising bright spot is emerging – artificial intelligence. This isn’t just a technological trend; it’s reshaping where and how capital flows, and understanding this dynamic is crucial for investors and policymakers alike.

The Widening Investment Divide

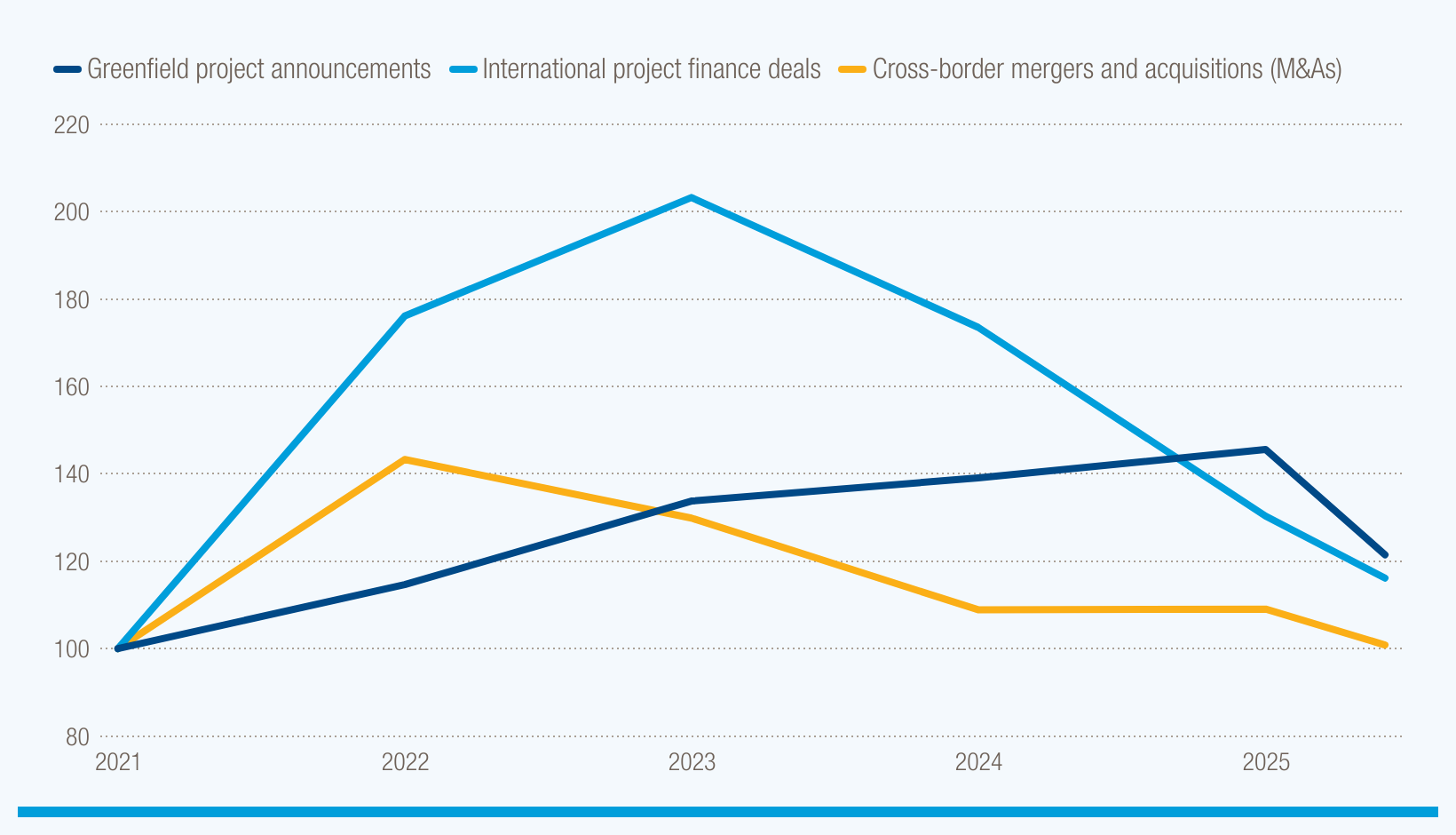

The UN Conference on Trade and Development (UNCTAD) reports that the decline in FDI is largely driven by developed economies, where cross-border mergers and acquisitions (M&As) plummeted 18% to $173 billion. This suggests a growing reluctance among established players to make large-scale, traditional investments. Developing economies, however, present a more nuanced picture. While overall flows remained flat, significant regional variations emerged. Latin America and the Caribbean saw a 12% increase in inflows, and developing Asia experienced a 7% rise. Conversely, Africa faced a substantial 42% drop, highlighting the continent’s vulnerability to global economic headwinds.

Supply Chain Disruptions and Manufacturing’s Struggles

High borrowing costs and persistent economic uncertainty are squeezing investment in key sectors. Greenfield projects – companies building new operations abroad – fell 17% in number, with a particularly sharp 29% decline in supply-chain-intensive manufacturing like textiles, electronics, and automotive. The ongoing efforts to “de-risk” supply chains, while strategically sound for many nations, are creating significant short-term disruption and investment hesitancy. International project finance, vital for infrastructure development, also suffered, with deal numbers down 11% and value declining by 8%.

“The current investment climate is characterized by a paradox: a desire for stability clashing with the inherent instability of the global geopolitical landscape. Companies are prioritizing resilience over rapid expansion, leading to a more cautious approach to foreign investment.” – Dr. Anya Sharma, Global Investment Strategist.

The AI Anomaly: A Surge in Greenfield Investment

Despite the overall downturn, a remarkable trend is bucking the negative momentum: investment in artificial intelligence (AI) and the digital economy is surging. The United States, for example, recorded a staggering $237 billion in new greenfield projects in the first half of 2025 – nearly matching the entire year 2024 and four times the average for the past decade. Over half of this value ($103 billion) was directed towards semiconductors, and another $27 billion went into data centers. This demonstrates a clear prioritization of technologies deemed essential for future economic competitiveness.

Global FDI is being reshaped by the demand for AI infrastructure. This isn’t simply about tech companies investing in themselves; it’s about a broader recognition that AI is a foundational technology impacting nearly every industry.

Key Takeaway: The rise of AI is not just a technological shift; it’s a fundamental re-allocation of global capital, creating new investment hotspots and potentially leaving traditional sectors behind.

Sustainable Development Goals Face Investment Drought

Unfortunately, the positive momentum of AI investment isn’t extending to all critical areas. Investment in sectors aligned with the Sustainable Development Goals (SDGs) continues to decline. SDG-related projects in developing countries were down 10% in number and 7% in value in early 2025. Least Developed Countries (LDCs) are particularly vulnerable, with projects on track to fall another 5% this year, potentially reaching their lowest level since 2015.

Infrastructure and Renewable Energy Lag Behind

Investment in infrastructure remains weak across developing economies, with internationally financed projects lagging 25% below the decade average. Greenfield infrastructure activity has declined by 31% in value and 25% in number, particularly in Latin America and the Caribbean. Renewable energy, a cornerstone of SDG 7 (Affordable and Clean Energy), is also facing headwinds, with global project finance falling 9% in number and 10% in value. Even in developing economies, renewable energy projects declined by 23%, and in LDCs, by 31%.

Did you know? Investment in water and sanitation has plummeted, with a 40% decrease globally and *no* new projects initiated in Africa or LDCs. This highlights a critical gap in funding for essential services.

Looking Ahead: Navigating a Complex Landscape

The global investment climate is expected to remain challenging for the remainder of 2025. Geopolitical tensions, regional conflicts, economic fragmentation, and supply chain de-risking will continue to exert downward pressure on investment flows. However, there are glimmers of hope. Easing financial conditions, a potential rebound in M&A activity in the third quarter, and increased overseas spending by sovereign wealth funds could provide a modest boost by year-end.

Pro Tip: Investors should prioritize diversification and focus on sectors demonstrating resilience in the face of global uncertainty. Consider opportunities in AI-related technologies, but also carefully assess the risks associated with emerging markets and geopolitical hotspots.

The Role of Emerging Markets

While Africa is currently facing significant investment challenges, other emerging markets, particularly in Asia and Latin America, are showing signs of resilience. These regions offer potential opportunities for investors willing to navigate the associated risks. The key will be identifying countries with stable political environments, sound economic policies, and a commitment to fostering a favorable investment climate.

Frequently Asked Questions

What is “de-risking” in the context of supply chains?

De-risking refers to efforts by companies and governments to reduce their reliance on single suppliers or countries, particularly those perceived as politically unstable or economically vulnerable. This often involves diversifying supply chains, nearshoring production, or investing in domestic manufacturing capabilities.

How is AI driving investment in semiconductors?

AI algorithms require massive computational power, which is heavily reliant on advanced semiconductors. The demand for AI is fueling a surge in investment in semiconductor manufacturing, research, and development, as companies race to secure a competitive edge in this critical technology.

What can be done to address the decline in SDG-related investment?

Addressing this decline requires a concerted effort from governments, international organizations, and the private sector. This includes increasing development aid, creating innovative financing mechanisms, and fostering a more favorable regulatory environment for SDG-related investments.

The future of global investment is being shaped by a complex interplay of forces. While headwinds persist, the rise of AI presents a unique opportunity for growth and innovation. Successfully navigating this landscape will require a strategic approach, a willingness to adapt, and a keen understanding of the evolving global dynamics. What are your predictions for the future of FDI? Share your thoughts in the comments below!