Global equity markets, led by Asian indices, are advancing on April 10, 2026, as investors anticipate diplomatic breakthroughs in upcoming US-Iran talks. While oil prices remain volatile due to ceasefire uncertainty, the broader market is pricing in a reduction of geopolitical risk and improved trade stability.

This market movement is not a simple reaction to diplomatic headlines. It represents a complex recalibration of the “geopolitical risk premium.” For months, the energy sector has acted as a volatility engine, dragging down industrial margins. Now, the market is attempting to decouple equity growth from energy instability, betting that a diplomatic resolution will lower the cost of capital and stabilize global supply chains.

The Bottom Line

- Geopolitical De-risking: Markets are pricing in a “peace dividend,” shifting capital from safe-haven assets back into growth-oriented equities.

- Inflationary Signals: The first rise in Chinese factory gate costs in four years suggests a pivot from deflation to producer-price inflation (PPI), potentially complicating central bank pivots.

- Energy Divergence: A disconnect has emerged where stocks rise on optimism while oil prices tick upward due to skepticism over the actual durability of a ceasefire.

The Disconnect Between Brent Crude and Equity Indices

On the surface, the current market behavior seems contradictory. Typically, rising energy costs act as a tax on consumers and a drag on corporate earnings. Yet, as we move into the second quarter of 2026, we are seeing a divergence. Oil prices are ticking upward—driven by doubts regarding the Iran ceasefire—while stocks are climbing.

Here is the math: the market is no longer fearing a total supply shock, but rather managing a “managed volatility” scenario. Investors are focusing on the potential for normalized trade routes in the Strait of Hormuz. If the US-Iran talks yield a framework for stability, the long-term reduction in insurance premiums for maritime shipping will outweigh the short-term increase in per-barrel costs.

This shift directly benefits logistics giants and global retailers. For instance, Amazon (NASDAQ: AMZN) and Walmart (NYSE: WMT) are highly sensitive to the “landed cost” of goods. A stabilized Middle East reduces the volatility of fuel surcharges, allowing for more predictable forward guidance on operating margins.

But the balance sheet tells a different story for energy majors. Companies like Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX) discover themselves in a precarious position. While higher oil prices boost immediate top-line revenue, the “optimism” driving the broader stock market is based on the eventual stabilization (and potential lowering) of energy prices.

| Metric | Current Trend (April 2026) | Market Impact | Risk Level |

|---|---|---|---|

| Brent Crude Oil | Increasing (+1.2% WoW) | Upward pressure on PPI | Moderate |

| Asian Equities | Increasing (Best week since 2022) | Increased Risk Appetite | Low |

| China Factory Gate Costs | Increasing (1st time in 4 years) | Imported Inflation | High |

| US Treasury Yields | Stabilizing | Lower Discount Rates | Moderate |

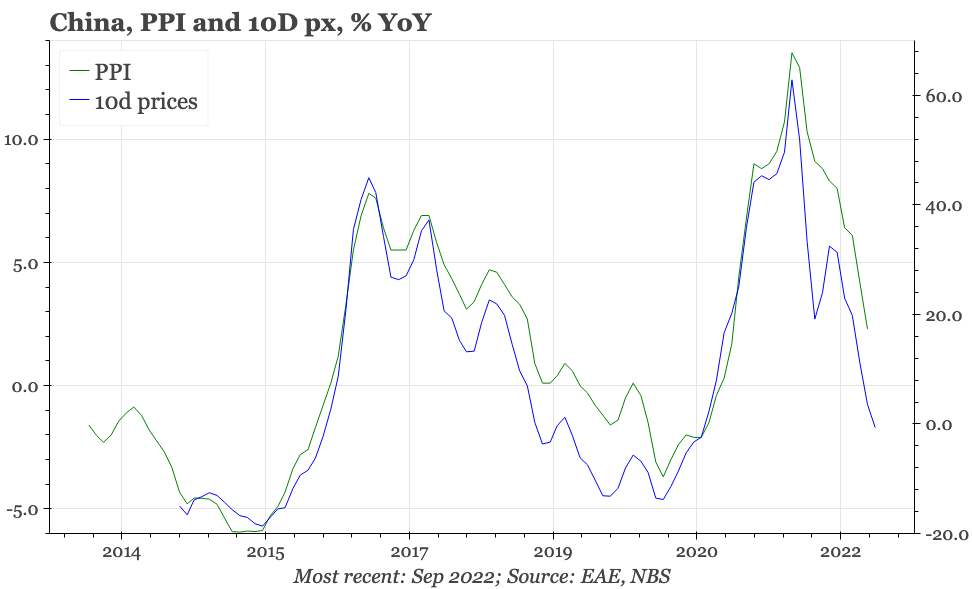

China’s PPI Pivot and the Global Inflation Loop

While the US-Iran talks capture the headlines, the more systemic risk is emerging from East Asia. The report that Chinese factory gate costs have increased for the first time in four years is a critical macroeconomic signal. For years, China has exported deflation to the rest of the world by keeping producer prices low.

When the People’s Bank of China (PBOC) oversees a rise in producer prices, it creates a ripple effect. This is not “healthy” demand-pull inflation. it is cost-push inflation. As the cost of raw materials and intermediate goods rises in China, global firms—from electronics manufacturers to automotive giants—will face higher Input costs.

This puts the Federal Reserve in a demanding position. If imported inflation rises due to Chinese PPI, the Fed may be forced to maintain higher interest rates for longer to combat the “second wave” of inflation, regardless of how well the US-Iran talks proceed.

“The market is currently ignoring the producer price signals from China in favor of the geopolitical narrative in the Middle East. However, the long-term trajectory of equity valuations depends more on the cost of inputs than on diplomatic handshakes.” — Dr. Julian Voss, Chief Economist at the Global Macro Institute.

Strategic Implications for Institutional Portfolios

Institutional investors are currently rotating out of extreme defensive postures. The “best week since 2022” for Asian stocks suggests that the fear of a regional conflict has reached a saturation point and any news—even tentative optimism—is being treated as a catalyst for a rally.

However, the smart money is watching the Bloomberg Commodity Index closely. The volatility in petrol and diesel prices, as noted by recent reports, suggests that the “last mile” of the ceasefire is the most dangerous. A failure in the US-Iran talks would not just reverse the current gains; it would likely trigger a flight to quality, benefiting the US Dollar (USD) and Gold.

we must consider the impact on the semiconductor supply chain. With TSMC (NYSE: TSM) and Nvidia (NASDAQ: NVDA) operating in a high-tension geopolitical environment, any diplomatic thaw between major powers reduces the “geopolitical discount” currently applied to their P/E ratios. If the talks signal a broader move toward stability, we could see a significant expansion in valuation multiples for the tech sector.

To understand the full scope of this volatility, one should examine the Reuters Market Data and the latest SEC filings regarding energy hedges for Fortune 500 companies. Many firms have over-hedged their fuel costs, meaning they are currently losing money on derivatives while the spot price of oil rises.

The Path Forward: Speculation vs. Fundamentals

As we gaze toward the close of the current trading cycle, the primary question is whether this rally is based on fundamentals or mere speculation. The fundamentals are mixed: energy costs are rising, and Chinese inflation is returning. The speculation, however, is bullish: a peaceful Middle East opens trade and lowers risk.

For the business owner, the takeaway is clear: do not mistake a diplomatic rally for a structural decline in costs. The rise in Chinese factory gate costs is a permanent shift in the supply chain landscape. Companies should focus on diversifying their sourcing to avoid being caught in a PPI spike.

In the coming weeks, the market will move from “optimism” to “verification.” Once the actual terms of the US-Iran talks are released, the market will stop trading on hope and start trading on the math of oil barrels and shipping lanes. Expect heightened volatility as the gap between the “optimism” of the stock market and the “doubt” of the oil market finally closes.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.