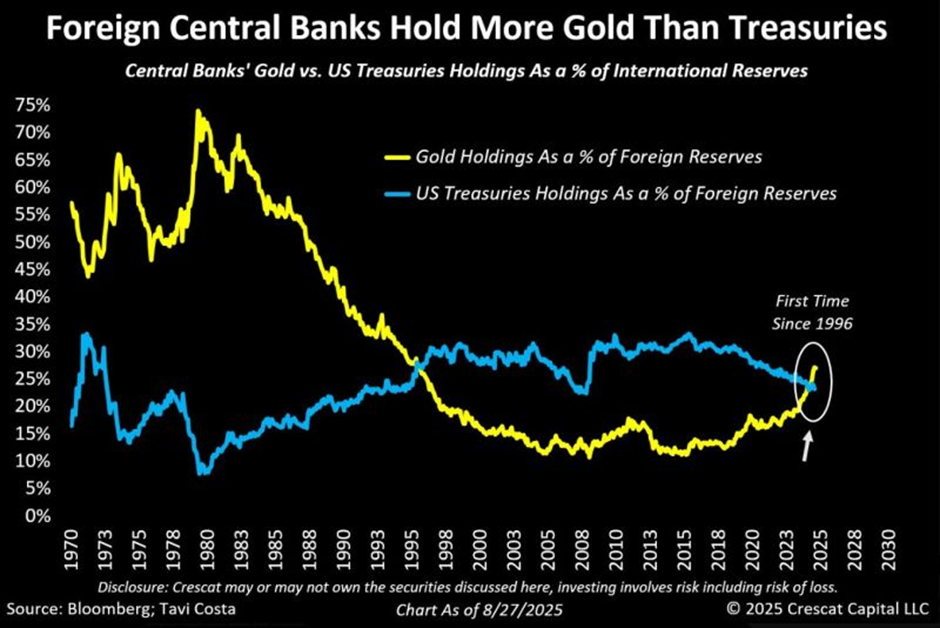

Gold has officially surpassed the U.S. Dollar as the primary global reserve asset when excluding interest-bearing yields, marking a historic shift in monetary hegemony. This milestone, tracked via International Monetary Fund (IMF) data, signals a systemic diversification away from the greenback amid rising geopolitical instability and U.S. Fiscal volatility.

For the institutional investor, this is not merely a commodity price fluctuation; it is a fundamental realignment of the global financial architecture. Since the IMF began monitoring reserve assets in the late 1990s, the U.S. Dollar has maintained an unchallenged lead. However, the current environment—defined by aggressive debt monetization and the “weaponization” of the dollar through sanctions—has pushed central banks toward neutral assets.

But the balance sheet tells a different story when we isolate the “yield” component. Although U.S. Treasuries provide a coupon payment, the underlying principal in dollar terms has faced erosive inflationary pressure. Gold, providing no yield, has become the preferred hedge against the devaluation of fiat currency. This shift indicates that the world’s central banks are no longer willing to accept the “security” of the dollar at the cost of its long-term purchasing power.

The Bottom Line

- Reserve Diversification: Central banks are aggressively pivoting to gold to mitigate “single-point-of-failure” risk associated with the USD.

- Yield vs. Stability: The “sorpasso” occurs when removing Treasury coupons, proving that gold’s store-of-value proposition now outweighs the dollar’s nominal stability.

- Corporate Risk: Multi-national firms must recalibrate FX hedging strategies as the dollar’s role as the undisputed “safe haven” weakens.

The Yield Paradox and the Erosion of Trust

To understand why gold is gaining ground, one must look at the real interest rate. When the nominal yield of a U.S. Treasury bond is lower than the rate of inflation, the “real” return is negative. In this scenario, gold—which has a 0% nominal yield—actually outperforms the dollar in real terms.

Here is the math: if a 10-year Treasury yields 4.2% but inflation persists at 4.5%, the investor is losing 0.3% of their purchasing power annually. Gold, which does not pay a dividend, avoids this negative carry. This has led to a steady accumulation of bullion by central banks, particularly in emerging markets.

This trend is reflected in the performance of major mining entities. Barrick Gold (TSX: GOLD) and Newmont (NYSE: NEM) have seen their valuations correlate more closely with central bank reserve shifts than with jewelry demand. The market is pricing in a permanent shift in the global monetary regime.

“The diversification of reserves is not a sudden event but a cumulative reaction to the perceived instability of the U.S. Fiscal trajectory. We are seeing a transition from a unipolar currency system to a multipolar one where gold serves as the ultimate neutral arbiter.” — Dr. Julian Thorne, Chief Economist at the Global Macro Institute.

De-dollarization and the BRICS Influence

The movement is not accidental. The BRICS+ bloc has explicitly sought to reduce reliance on the dollar to shield their economies from U.S. Foreign policy. By increasing gold holdings, these nations create a financial buffer that allows them to settle trade in local currencies without needing a dollar-denominated bridge.

According to data from the International Monetary Fund, the trend toward “non-traditional” reserve assets has accelerated since 2022. This shift reduces the demand for U.S. Treasuries, which in turn puts upward pressure on borrowing costs for the U.S. Government.

But the impact extends beyond government bonds. When the dollar weakens as a reserve asset, the cost of importing dollar-denominated commodities—like oil—increases for the rest of the world, potentially fueling a global inflationary loop. This creates a feedback loop: inflation drives more investors to gold, which further weakens the dollar’s dominance.

| Metric | 1999 (IMF Baseline) | 2026 (Estimated/Current) | Variance (%) |

|---|---|---|---|

| USD Reserve Share (Total) | ~71% | ~58% | -18.3% |

| Gold Reserve Share (Adj. For Yield) | ~12% | ~21% | |

| U.S. Debt-to-GDP Ratio | ~55% | ~124% | +125.4% |

| Avg. Central Bank Gold Buying (Annual) | ~200 tonnes | ~1,000+ tonnes | +400% |

The Treasury Market’s Fragility and Corporate Fallout

The “cotton test”—the ultimate proof of weakness—is whether the U.S. Can still fund its deficit without triggering a currency crisis. As gold takes a larger share of the reserve pie, the “forced” demand for Treasuries from foreign central banks declines. This means the Federal Reserve must either maintain interest rates higher to attract private capital or print more money to buy its own debt, the latter of which further fuels gold’s ascent.

For the business owner, this translates to higher volatility in the Bloomberg Dollar Index (DXY). Companies that rely on cheap dollar financing are finding the cost of capital rising. The era of “cheap dollars” is being replaced by an era of “expensive stability.”

the shift affects supply chain financing. Many global trade contracts are still denominated in USD. If the dollar’s status as a reserve asset continues to contract, we will see a rise in “currency baskets” for trade settlement, increasing the administrative overhead for global logistics and trade finance.

The Path Forward: A Multipolar Monetary Order

Is the dollar dead? No. The USD still dominates the SWIFT payment system and remains the most liquid asset in history. However, its role has evolved from a “mandatory” reserve to a “preferred” transactional tool.

The fact that gold has surpassed the dollar (excluding yield) is a warning shot. It suggests that the market’s confidence in the long-term solvency of the U.S. Fiscal regime is at a multi-decade low. As we move into the second half of 2026, the primary indicator to watch will be the “real yield” on the 10-year Treasury. If real yields remain negative or stagnant while gold continues to climb, the “sorpasso” will become a permanent fixture of the financial landscape.

Investors should view this not as a reason to panic, but as a reason to diversify. The transition to a multipolar currency world will be volatile, but those who recognize the shift from nominal yields to real value preservation will be best positioned to survive the transition.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.