Unseasonably warm temperatures nearing 90°. F in early April 2026 are triggering premature surges in energy demand and shifting retail consumer patterns. This anomalous weather pattern impacts utility load management, accelerates the cooling season for HVAC providers, and introduces volatility into agricultural futures and energy spot prices across North America.

While a weather forecast may seem trivial to the casual observer, for the institutional investor, it is a leading indicator of operational stress and revenue acceleration. When temperatures hit 90°F in the second week of April, the market isn’t reacting to the heat—it is reacting to the disruption of the seasonal Capex cycle. We are seeing a compressed transition from heating to cooling that threatens grid stability and disrupts inventory rotations for big-box retailers.

The Bottom Line

- Utility Load Volatility: Immediate pressure on electrical grids increases the risk of peak-load pricing and unplanned outages, impacting margins for firms like NextEra Energy (NYSE: NEE).

- HVAC Revenue Pull-Forward: A “cooling cliff” accelerates demand for residential AC units, benefiting Carrier Global (NYSE: CARR) but stressing supply chain lead times.

- Agricultural Risk: Early heatwaves during critical spring planting windows introduce volatility into corn and soybean futures, impacting global agribusiness leaders like Archer-Daniels-Midland (NYSE: ADM).

The Cooling Cliff and Utility Margin Compression

The electrical grid is designed for predictable seasonal ramps. When temperatures jump to 90°F in early April, the “ramp-up” becomes a “spike.” This forces utilities to engage peaking plants—often the most expensive and least efficient generators—to meet the sudden surge in air conditioning demand.

But the balance sheet tells a different story. While higher volume typically suggests higher revenue, the cost of procuring emergency power on the spot market can erode margins. For a company like Duke Energy (NYSE: DUK), the challenge is not the demand itself, but the cost of the electrons required to meet it during an anomalous spike.

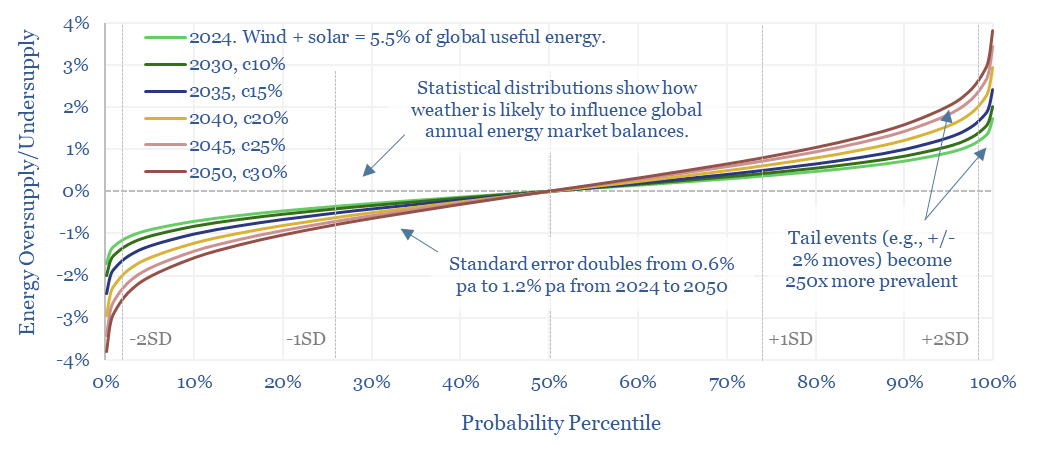

According to data from the U.S. Energy Information Administration, anomalous spring warming correlates with a 4-7% increase in short-term wholesale electricity prices in deregulated markets. Here is the math: if a utility must buy power at $150/MWh instead of $40/MWh to prevent a brownout, the operational cost per customer rises faster than the billed revenue can keep pace, assuming regulated rate structures.

“Climate volatility is no longer a ‘tail risk’ for utilities; it is a baseline operational reality. Early-season heat spikes force a premature shift in load forecasting that can leave grids vulnerable before the primary summer maintenance windows are closed.” — Marcus Thorne, Senior Energy Analyst at Global Macro Insights.

HVAC Demand and the Supply Chain Lag

For the residential services sector, 90-degree weather in April is a catalyst for immediate revenue. However, this “pull-forward” effect creates a dangerous imbalance in the supply chain. Trane Technologies (NYSE: TT) and Carrier Global (NYSE: CARR) typically manage inventory based on a May/June surge.

When the surge happens in April, the “Information Gap” emerges between consumer demand and technician availability. We are seeing a spike in service calls that exceeds the current labor capacity of most HVAC franchises. This leads to longer lead times and potential customer churn.

Why does this matter for the portfolio? Because these companies are now competing for components in a market that is suddenly 30 days ahead of schedule. If the supply of compressors and refrigerants doesn’t accelerate, the revenue gains from the heatwave will be capped by fulfillment bottlenecks.

| Sector | Correlation to Heat | Primary Financial Risk | Short-Term Market Sentiment |

|---|---|---|---|

| Utilities | Positive (Volume) | Spot Price Volatility | Neutral/Volatile |

| Agriculture | Negative (Stress) | Yield Reduction | Bearish/Speculative |

| Retail | Mixed (Seasonal) | Inventory Mismatch | Neutral |

| HVAC | Positive (Demand) | Labor/Supply Shortage | Bullish |

Agricultural Volatility and the CME Futures Market

Beyond the power grid, the real danger of a 90-degree April lies in the soil. In the Midwest, early heat can accelerate crop development too quickly or cause moisture stress during the critical germination phase for corn and soybeans.

This creates an immediate reaction in the CME Group futures markets. Traders begin pricing in “weather premiums,” which can drive up the cost of raw commodities. For a global processor like Archer-Daniels-Midland (NYSE: ADM), this volatility complicates hedging strategies and can squeeze margins if the cost of raw inputs rises faster than the price of processed goods.

But there is a catch. If the heat is followed by a sudden cold snap—a common pattern in volatile springs—the damage to the crop is compounded. This “yo-yo” effect is what institutional investors watch closely when assessing the risk profile of agricultural ETFs and commodity-linked equities.

Retail Pivot: The Inventory Mismatch

The retail sector is perhaps the most sensitive to these shifts. Companies like Walmart (NYSE: WMT) and Target (NYSE: TGT) operate on rigid seasonal calendars. Their “Spring” collections are designed for 60-75 degree weather. When the mercury hits 90°F, the demand shifts instantly to summer apparel and outdoor leisure products.

This creates an inventory mismatch. Retailers are left with an oversupply of light jackets and long-sleeve shirts (which must eventually be discounted, hitting gross margins) while facing stock-outs of fans, grills, and summer wear. This inefficiency is a hidden drag on Q2 earnings that often goes unmentioned in corporate PR speak.

As noted in recent reports by Bloomberg, the ability of a retailer to utilize AI-driven “dynamic inventory” is now a competitive advantage. Those who can shift logistics in real-time to meet a 90-degree April will outperform those clinging to a static seasonal calendar.

The Macroeconomic Trajectory

From a macroeconomic perspective, these weather anomalies contribute to “climate-driven inflation.” When energy costs spike and crop yields are threatened, the result is a marginal increase in the Consumer Price Index (CPI). While a single heatwave won’t move the needle for the Federal Reserve, a pattern of such anomalies creates a higher floor for inflation.

Looking ahead to the close of the current quarter, investors should monitor the “cooling degree days” (CDD) data. If the trend of early warming continues, we can expect a significant shift in energy expenditure and a potential volatility spike in the commodities market. The play here is not to bet on the weather, but to bet on the companies with the supply chain agility to absorb the shock.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.