{kind=link}

Published: October 17,2025

New York,NY – Shares of several regional banks experienced significant declines on October 16,2025,following disclosures regarding revolving credit lines provided to funds specializing in distressed debt. The sell-off, reminiscent of anxieties following the Silicon Valley Bank collapse, highlights mounting investor apprehension about hidden risks within the banking sector and the potential for rapid contagion. The decline in bank stocks underscores a growing sensitivity to off-balance sheet exposures.

Table of Contents

- 1. The Rise of Revolving Credit and its Hidden Risks

- 2. financial Impact: A Snapshot of the Market Reaction

- 3. How Revolving Credit amplifies Systemic Risk

- 4. The Problem of Opacity

- 5. What Investors Should Be Doing Now

- 6. understanding Distressed Debt Investing

- 7. Frequently Asked Questions About Regional Bank Risk & Credit Facilities

- 8. How might increased bank lending to distressed funds amplify procyclicality in financial markets?

- 9. Hidden Risks: Teh Structural Danger of Banks Lending to Distressed Funds

- 10. The Growing Trend of Bank-Distressed Fund Partnerships

- 11. Why Banks are Increasingly Involved

- 12. The Core Risks: A Systemic View

- 13. The Role of Leverage: amplifying the Problem

- 14. Regulatory Gaps and Challenges

- 15. Case Study: The 2008 Financial Crisis – Lessons Unlearned?

- 16. Benefits (and Why the Trend Persists)

- 17. Practical Tips for Risk Mitigation

Unlike traditional commercial loans, thes revolving credit facilities function as lines of credit extended to funds that acquire troubled assets at discounted rates. Banks profit from fees and interest, while funds gain financial leverage. This structure, however, introduces a unique set of challenges and amplifies existing vulnerabilities, creating a situation where even modest exposures can trigger disproportionate market reactions.

Analysts are pointing to three significant issues within this model. Firstly, the collateral backing these loans is inherently distressed, increasing the difficulty of accurate valuation. Secondly, the revolving nature of the credit permits continuous borrowing until the facility is revoked, potentially creating liquidity crunches. a conflict of interest arises: funds benefit from delaying acknowledgment of asset value declines,while banks earn revenue as long as the facilities remain active.

financial Impact: A Snapshot of the Market Reaction

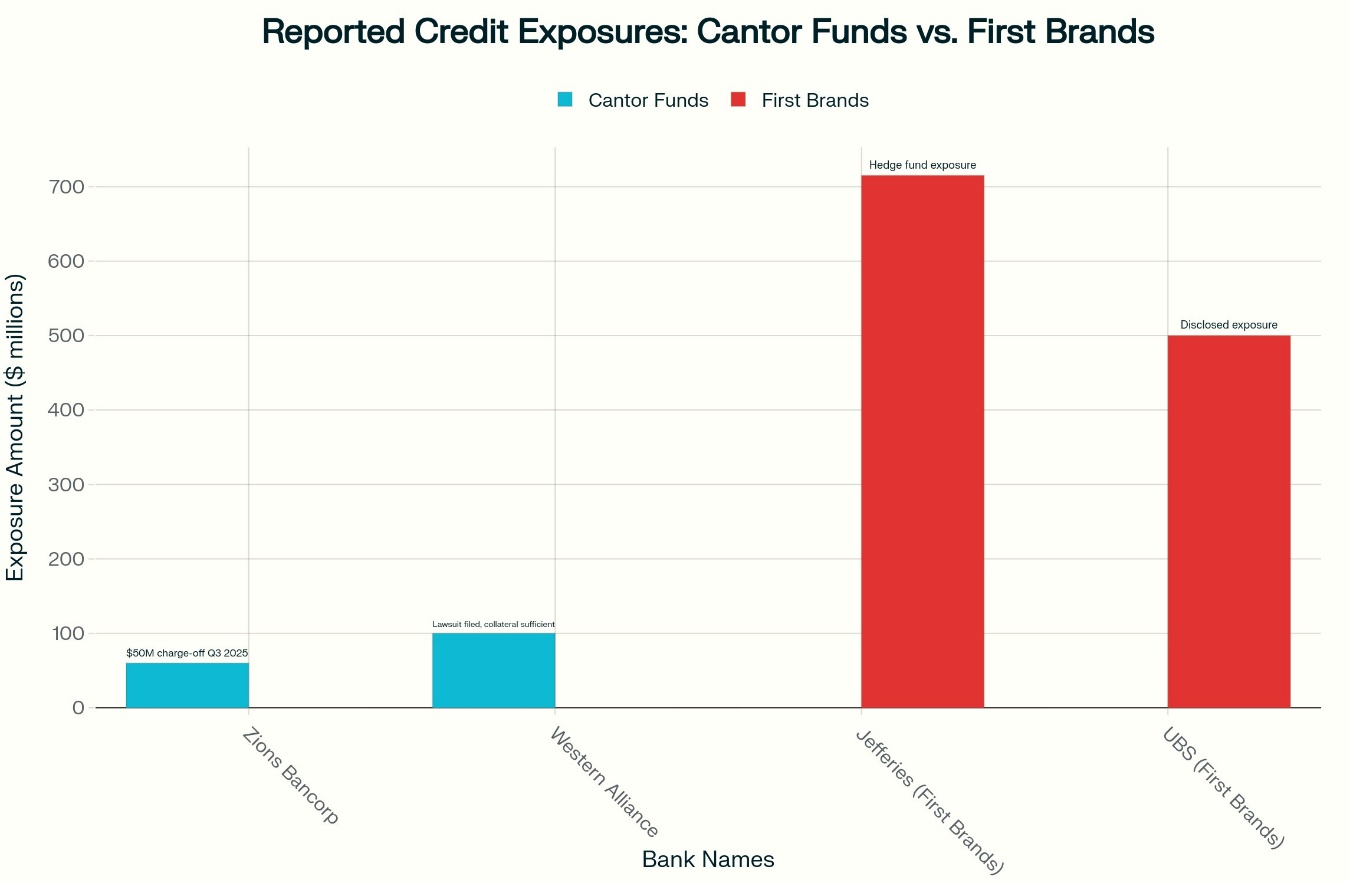

Recent filings, including 8-K reports and investor presentations, indicate total exposure across several banks ranges from $200 million to over $500 million. For institutions wiht assets between $10 billion and $30 billion, a $100 million exposure represents between 30 and 100 basis points of tangible common equity – a potentially substantial figure. The immediate market response demonstrated investor anxiety.

| Bank/Index | Stock Price decline (October 16, 2025) |

|---|---|

| [Bank A] | 13.14% |

| [Bank B] | 10.81% |

| KBW Regional Banking Index | 6.31% |

How Revolving Credit amplifies Systemic Risk

The continuous availability of funds means banks maintain real-time exposure to declining collateral values without the built-in maturity limits of conventional loans. When the value of fund assets decreases – whether through market forces or misrepresentation – the bank has already disbursed the funds. This dynamic creates significant incentive misalignment.

Funds may be motivated to understate asset value drops to avoid margin calls,while banks continue to generate revenue from fees and spreads.This pressure can lead to underpricing of risk, as observed in recent instances where banks maintained or even expanded facility sizes despite deteriorating fund performance. Accurately valuing distressed debt is also a challenge, relying on subjective assessments of recovery value and timelines, rather than objective market pricing.

The Problem of Opacity

Four key factors contribute to the difficulty of assessing these risks. These include limited public reporting on fund performance, the ability to draw funds with short notice, the complexity of transfer pricing when banks provide both lending and advisory services, and the lack of standardized methods for valuing distressed debt. this makes it nearly impossible for analysts to accurately gauge potential losses.

Chart comparing exposure levels between cantor Funds and First Brands, illustrating the relative scale of risk across different credit events.

What Investors Should Be Doing Now

Experts advise investors to re-evaluate risk premiums applied to regional bank credits, demanding larger discounts until greater transparency is achieved or underwriting standards tighten. Its also prudent to reduce position sizes or widen stop-loss orders for banks known to have exposure to asset-backed revolvers. Careful monitoring of regulatory filings and footnotes for terms like “asset-backed revolver” or “fund facility” may provide early warning signs. Hedging strategies,such as purchasing out-of-the-money puts,could offer downside protection,while considering bank ETFs that underweight regionals,or favor larger institutions with stronger disclosure practices can also be valuable.

Furthermore, investors should be aware of potential merger and acquisition activity, as prolonged uncertainty and depressed valuations may increase the likelihood of takeovers. increased regulatory scrutiny will likely lead to higher compliance costs and reduced margins for banks operating in this space.

Did You Know? the current environment mirrors concerns raised after the 2008 financial crisis regarding complex financial instruments and opaque risk exposures.

Pro Tip: regularly review disclosure quality regarding off-balance sheet exposures and quantify concentrations to funds or asset-backed facilities to stay informed.

Are regional banks adequately preparing for increased regulatory scrutiny in the wake of these events? Do you believe greater transparency will be enough to restore investor confidence?

understanding Distressed Debt Investing

Distressed debt investing involves purchasing the debt of companies facing financial difficulty, typically at substantial discounts. the goal is to profit from the eventual recovery of the debt, through restructuring, liquidation, or a prosperous turnaround of the borrower. However, it is an inherently risky strategy, requiring specialized expertise in valuation, legal frameworks, and turnaround operations. The rise of these funds has created both opportunities and challenges for the broader financial system.

According to a recent report by Preqin, assets under management in distressed debt funds reached $85 billion in 2024, demonstrating continued investor interest. Preqin Distressed Debt Report

Frequently Asked Questions About Regional Bank Risk & Credit Facilities

- What is a revolving credit facility? It’s a type of loan that allows borrowers to draw,repay,and redraw funds up to a certain limit.

- What is distressed debt? It refers to the debt of companies facing financial hardship, often trading at a discount to its face value.

- Why are these credit facilities risky for banks? The collateral is already distressed, and the revolving nature of the credit can amplify losses quickly.

- How can investors assess this risk? Monitor bank disclosures and look for exposure to “asset-backed revolvers” or “fund facilities.”

- What is the role of regulatory oversight? Regulators are likely to increase scrutiny and potentially implement tighter reporting requirements.

- What impact can this event have on the broader economy? Reduced lending and increased risk aversion could slow economic growth.

- Are there any option investment strategies to consider? Diversifying into large-cap banks with stronger disclosure practices is an option.

Share this article with your network and join the conversation in the comments below!

How might increased bank lending to distressed funds amplify procyclicality in financial markets?

The Growing Trend of Bank-Distressed Fund Partnerships

The relationship between traditional banks and distressed debt funds has deepened significantly in recent years. While seemingly a mutually beneficial arrangement – banks offloading risky assets and funds potentially reaping high returns – this trend introduces systemic risks that are frequently enough underestimated. This article explores the hidden dangers of banks lending to distressed funds, focusing on the potential for contagion, regulatory loopholes, and the amplification of market downturns. We’ll cover distressed debt investing, leveraged finance, and the implications for financial stability.

Why Banks are Increasingly Involved

Several factors drive banks towards collaborating with distressed funds:

* Capital Relief: Selling non-performing loans (NPLs) or other distressed assets frees up regulatory capital, allowing banks to lend more in other areas. This is particularly crucial under stricter Basel III regulations.

* De-risking Balance Sheets: Offloading problematic assets improves a bank’s overall financial health and reduces exposure to potential losses.

* Fee Income: Banks earn fees from arranging and participating in these transactions, boosting profitability.

* Limited Internal Expertise: Dealing with complex distressed situations often requires specialized skills that banks may lack internally. Private credit funds fill this gap.

The Core Risks: A Systemic View

The core danger lies in the interconnectedness created by these lending arrangements. Here’s a breakdown of the key risks:

* Contagion Risk: If a distressed fund suffers significant losses, it may be forced to liquidate assets rapidly, driving down prices across the board. banks heavily exposed to that fund – through direct loans or indirect exposure via collateral – could face substantial losses, potentially triggering a cascade effect. This is a classic example of systemic risk.

* Procyclicality: these arrangements exacerbate market cycles. Banks are more likely to lend to distressed funds during economic downturns, when assets are cheapest. This increased demand can artificially inflate asset prices, creating a bubble that eventually bursts.

* Opacity and Complexity: The structures involved are often incredibly complex, making it difficult for regulators and investors to fully understand the risks. Shadow banking activities are often involved, further obscuring the true extent of exposure.

* Moral Hazard: Banks may be less diligent in their initial lending practices if they know they can always offload the risk to a distressed fund. This creates a moral hazard problem,encouraging reckless behavior.

The Role of Leverage: amplifying the Problem

Distressed funds frequently employ significant leverage – borrowing money to amplify their returns. Banks are often the primary lenders providing this leverage. This creates a hazardous feedback loop:

- Increased Returns (on paper): Leverage boosts potential profits during good times.

- Higher Risk: Leverage magnifies losses during downturns.

- Bank Exposure: Banks are directly exposed to these leveraged positions.

- Potential for Fire Sales: If the fund encounters difficulties, forced asset sales can destabilize the market.

The use of margin calls and collateralized loan obligations (CLOs) further complicates the situation,potentially accelerating the downward spiral.

Regulatory Gaps and Challenges

Current regulations often struggle to keep pace with the evolving relationship between banks and distressed funds. Key challenges include:

* Limited Visibility: Regulators may lack a complete picture of banks’ exposure to distressed funds, particularly through indirect channels.

* Classification Issues: Determining the appropriate risk weighting for loans to distressed funds can be challenging.

* Cross-Border Complexity: many distressed funds operate across multiple jurisdictions, making regulation even more difficult.

* Lack of Stress Testing: Existing stress tests may not adequately account for the systemic risks posed by these arrangements.

Case Study: The 2008 Financial Crisis – Lessons Unlearned?

The 2008 financial crisis provides a stark warning. While the specific instruments differed, the underlying principle of interconnectedness and excessive leverage remains relevant. The collapse of Lehman Brothers, heavily involved in complex financial instruments, triggered a global credit crunch.The current situation, with banks increasingly reliant on distressed funds, shares concerning similarities.The rise of special purpose vehicles (SPVs) in the current market echoes the structures that contributed to the 2008 crisis.

Benefits (and Why the Trend Persists)

Despite the risks, the bank-distressed fund relationship offers some benefits:

* Efficient Capital Allocation: Distressed funds can put capital to work in situations where banks are unwilling or unable to act.

* Restructuring Expertise: Funds often possess the skills and resources to successfully restructure struggling companies.

* Economic Recovery: By taking ownership of distressed assets, funds can help facilitate economic recovery.

However, these benefits must be weighed against the potential systemic risks.

Practical Tips for Risk Mitigation

For banks and regulators:

* Enhanced Due Diligence: Thoroughly assess the risks associated with lending to distressed funds, including the fund’s investment strategy, leverage levels, and