Major food corporations are facing a confluence of challenges – persistently high input costs and a consumer shift towards healthier, often less profitable, dietary choices – resulting in declining sales volumes and margin compression. This trend, accelerating since late 2023, is impacting industry giants like **Nestlé (SIX: NESN)**, **PepsiCo (NASDAQ: PEP)**, and **General Mills (NYSE: GIS)**, forcing them to reassess pricing strategies and product portfolios. The situation is particularly acute in the US and Europe, where inflation remains elevated and health consciousness is growing.

The narrative surrounding the food industry has long been one of resilience, a sector providing essential goods regardless of economic cycles. However, the current environment is proving different. It’s not simply a matter of consumers cutting back on discretionary spending; they are actively altering their consumption patterns. This isn’t a temporary blip; it’s a structural shift with potentially long-lasting consequences for the established players.

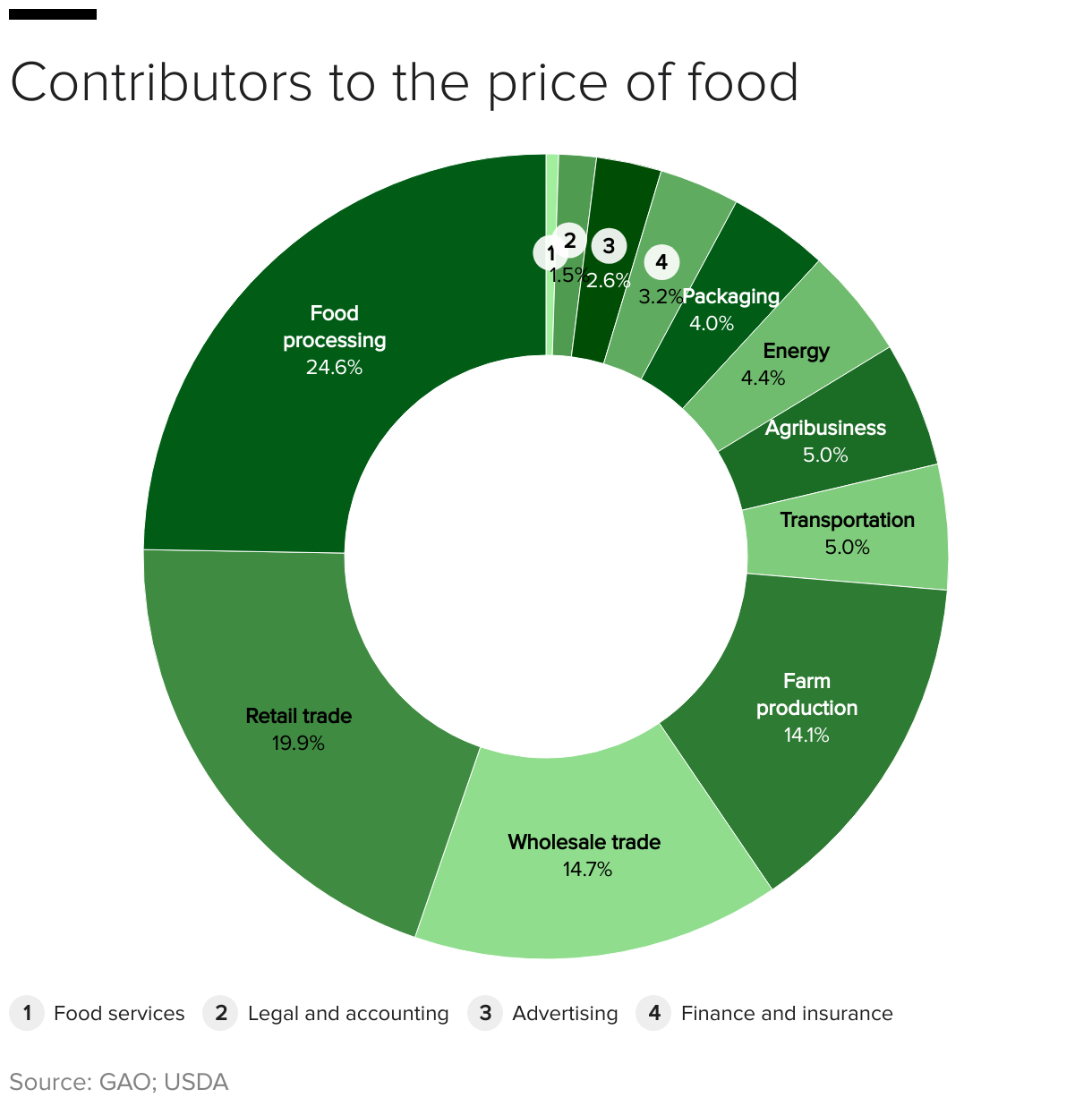

The Bottom Line

- Margin Pressure Intensifies: Big Food companies are experiencing shrinking profit margins due to rising ingredient costs and a reluctance to pass those costs onto increasingly price-sensitive consumers.

- Portfolio Re-evaluation is Critical: Companies must aggressively prune underperforming brands and invest in healthier, higher-growth categories to remain competitive.

- M&A Activity Likely to Increase: Expect consolidation as larger players seek to acquire innovative, health-focused brands and smaller companies struggle with profitability.

The Price Elasticity Problem: When Loyalty Doesn’t Pay

For decades, these companies have relied on brand loyalty and economies of scale to maintain profitability. But the current inflationary environment has exposed a critical weakness: price elasticity. Consumers are demonstrably willing to switch brands – even well-established ones – to secure lower prices. According to recent data from the US Bureau of Labor Statistics, food-at-home prices increased 2.2% over the past year (as of February 2026), even as consumer spending on food away from home (restaurants) grew by 3.8% . This suggests a trade-down effect, with consumers opting for cheaper alternatives or shifting spending to experiences.

Here is the math. **Nestlé**, for example, reported a 2.5% decline in organic sales growth in North America during Q4 2025, citing “increased price sensitivity” among consumers. Their EBITDA margin contracted by 80 basis points, from 16.2% to 15.4% . **PepsiCo**, while demonstrating more resilience due to its diversified portfolio (including Frito-Lay), saw a 1.1% decrease in volume for its North American beverage segment. But the balance sheet tells a different story, with PepsiCo’s stock price remaining relatively stable, supported by its strong cash flow and dividend yield.

The Rise of Health & Wellness: A Threat to Legacy Brands

The shift towards healthier eating isn’t latest, but its acceleration is noteworthy. Consumers are increasingly scrutinizing ingredient lists, seeking out products with lower sugar, salt, and fat content. This trend is fueling the growth of smaller, more agile companies focused on natural and organic foods. **Beyond Meat (NASDAQ: BYND)**, despite its own challenges, exemplifies this shift, demonstrating consumer demand for plant-based alternatives. However, Beyond Meat’s struggles highlight the difficulty of scaling in this competitive landscape.

“We’re seeing a fundamental change in consumer priorities,” says Dr. Emily Carter, a senior economist at Capital Group.

“Consumers are no longer solely focused on price and convenience. They are willing to pay a premium for products that align with their health and ethical values. This is a significant challenge for the traditional food giants, who have built their empires on mass-produced, often highly processed, foods.”

Market Share Dynamics and Potential Consolidation

The changing landscape is creating opportunities for both disruption and consolidation. Smaller, innovative companies are gaining market share at the expense of the established players. This is particularly evident in the snack food category, where brands like **RXBAR** and **Larabar** have carved out significant niches. The pressure on margins is likely to lead to increased M&A activity, as larger companies seek to acquire these promising brands. Antitrust scrutiny, however, will be a significant hurdle. The FTC has already signaled a more aggressive stance towards mergers in the food and beverage industry.

Here’s a comparative snapshot of key financial metrics (Q4 2025):

| Company | Revenue (USD Billions) | EBITDA (USD Billions) | EBITDA Margin (%) | YOY Revenue Growth (%) |

|---|---|---|---|---|

| **Nestlé (SIX: NESN)** | 98.5 | 18.2 | 18.5 | -0.8 |

| **PepsiCo (NASDAQ: PEP)** | 86.4 | 16.5 | 19.1 | 0.5 |

| **General Mills (NYSE: GIS)** | 19.3 | 3.1 | 16.1 | -2.1 |

| **Beyond Meat (NASDAQ: BYND)** | 0.3 | -0.05 | -16.7 | -18.5 |

Supply Chain Resilience and Inflationary Pressures

The ongoing geopolitical instability and climate change-related disruptions continue to exert pressure on global supply chains. The cost of key agricultural commodities, such as wheat, corn, and soybeans, remains elevated. This is forcing food companies to explore alternative sourcing strategies and invest in supply chain resilience. **Amazon (NASDAQ: AMZN)**, with its expanding logistics network, is increasingly becoming a critical partner for food companies, offering both distribution and data analytics capabilities. How Amazon absorbs the supply chain shock is a key indicator of future industry trends.

“The food industry is facing a perfect storm of challenges,” notes Michael Thompson, CEO of FoodChain Insights.

“Inflation, changing consumer preferences, and supply chain disruptions are all converging to create a highly uncertain environment. Companies that can adapt quickly and innovate will be the ones that thrive.”

Looking ahead, the outlook for the big food companies remains cautious. While they possess significant financial resources and marketing power, they must address the fundamental shift in consumer behavior. Investing in healthier product offerings, streamlining supply chains, and exploring strategic acquisitions will be crucial for navigating this challenging landscape. The next 12-18 months will be pivotal in determining which companies can successfully adapt to the new realities of the food industry.

The market will be closely watching earnings reports from these companies in the coming quarters, paying particular attention to their ability to maintain margins and grow revenue in the face of these headwinds. The performance of smaller, more agile competitors will too be a key indicator of the broader trends shaping the industry.

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*