Brazil’s IGP-M inflation index rose 0.52% in March, impacting rental contracts, but those expiring in April are shielded from increases. This divergence stems from contractual clauses and a broader 1.83% year-over-year decline in the index. While rising agricultural prices contribute to the current uptick, the impact on renters is limited by pre-existing agreements, creating a temporary buffer against broader inflationary pressures.

The Disconnect Between Headline Inflation and Rental Costs

The recent increase in the IGP-M, as reported by the FGV, presents a nuanced picture for Brazilian renters. While the 0.52% rise in March signals inflationary pressure – particularly in agricultural commodities like beef, eggs, and milk – a significant portion of the rental market remains insulated. This is due to the prevalence of contracts that explicitly prevent negative adjustments when the IGP-M falls. Essentially, while landlords *could* theoretically lower rents based on the 1.83% 12-month decline, most contracts prevent this, maintaining rental income at current levels. This creates a lag effect, where renters don’t immediately benefit from the index’s downturn.

The Bottom Line

- Rental Market Stability: Despite IGP-M increases, a large segment of the rental market faces no immediate price hikes due to contractual protections.

- Agricultural Inflation Driver: Rising agricultural prices are the primary catalyst for the recent IGP-M increase, signaling potential broader inflationary risks.

- Divergence from IPCA: The IGP-M’s composition differs significantly from the IPCA (Brazil’s official consumer price index), offering a distinct perspective on inflationary trends.

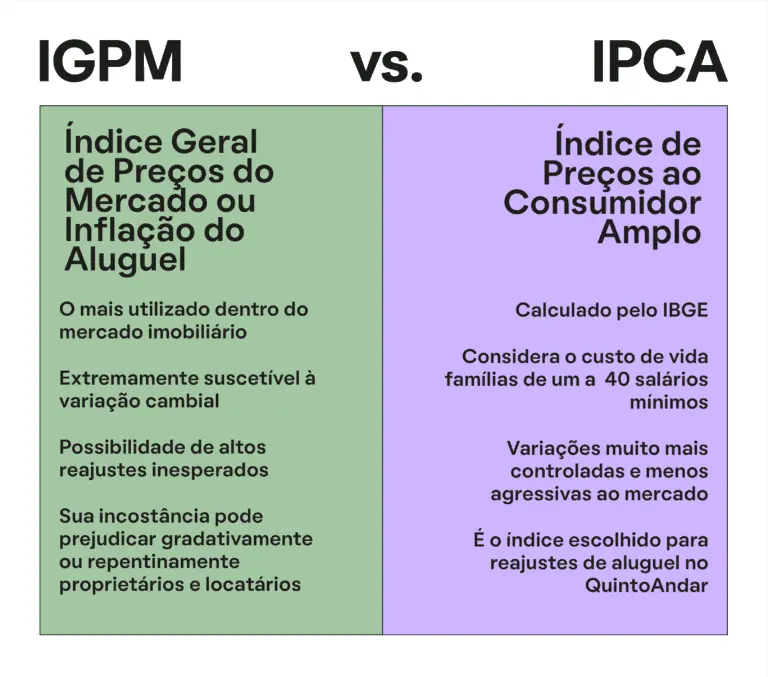

Understanding the IGP-M and its Limitations

It’s crucial to understand that the IGP-M isn’t a direct measure of consumer inflation. The IGP-M (Índice Nacional de Preços — Mercado) focuses on prices of goods and services used in production – agriculture, industry, and construction – rather than the basket of goods consumed by households. This is why it differs from the IPCA (Índice Nacional de Preços ao Consumidor Amplo), which tracks the price changes experienced by families earning up to 40 minimum wages (approximately R$64,840 as of March 2026). The Central Bank of Brazil’s FOCUS report consistently highlights the divergence between these two indices, and their respective impacts on monetary policy.

The current situation highlights a potential disconnect. While the IGP-M is rising, driven by agricultural factors, the IPCA – which more directly impacts consumer spending – may not reflect the same intensity. This divergence complicates the task for the *Banco Central do Brasil* as it navigates monetary policy decisions.

The Impact on Real Estate Investment Trusts (REITs)

The stability in rental income, despite the IGP-M increase, has implications for Brazilian Real Estate Investment Trusts (REITs), known as *Fundos de Investimento Imobiliário* (FIIs). While rising IGP-M typically allows for higher rental adjustments, the contractual limitations prevent immediate gains for many FIIs. This is particularly relevant for FIIs focused on commercial properties with long-term leases indexed to the IGP-M.

**Bradesco Real Estate Funds (BRESF11)**, a major player in the Brazilian REIT market, for example, will likely see a muted impact on its Q2 2026 earnings from the IGP-M increase. However, as older contracts expire and are renegotiated, the potential for increased rental income will become more apparent. According to a recent report by Suno Research, FIIs with a higher proportion of short-term leases indexed to the IGP-M are better positioned to benefit from the current inflationary environment.

| REIT (Ticker) | Q1 2026 Revenue (BRL Millions) | Q1 2026 EBITDA (BRL Millions) | % of Leases Indexed to IGP-M |

|---|---|---|---|

| Bradesco Real Estate Funds (BRESF11) | 125.5 | 88.2 | 45% |

| Vinci Logistics (VILC11) | 98.7 | 72.1 | 60% |

| XP Corporate (XPML11) | 75.3 | 55.8 | 30% |

Geopolitical Risks and the Agricultural Impact

The FGV report specifically cited the worsening geopolitical situation in the Middle East as a contributing factor to the IGP-M increase. This is manifesting in higher prices for petroleum derivatives, which in turn impacts transportation costs and agricultural inputs. The rising cost of fertilizer, for instance, directly affects agricultural production and ultimately contributes to higher food prices.

“We are seeing a clear transmission of geopolitical risk into commodity prices, and Brazil, as a major agricultural exporter, is particularly vulnerable. The IGP-M is an early indicator of these pressures.”

– Dr. Ana Paula Kliemann, Senior Economist, NovaBroke

This situation underscores the interconnectedness of global events and their impact on the Brazilian economy. The ongoing conflict in the Middle East, coupled with potential disruptions to global supply chains, could lead to sustained inflationary pressures in the agricultural sector, even if rental costs remain relatively stable in the short term.

Looking Ahead: The Trajectory of the IGP-M and its Implications

The future trajectory of the IGP-M remains uncertain. While the current increase is largely driven by agricultural factors and geopolitical risks, the overall economic outlook for Brazil will play a crucial role. The *Banco Central do Brasil*’s monetary policy decisions, particularly regarding interest rates, will significantly influence inflationary pressures. Reuters’ commodity price forecasts suggest that agricultural prices are likely to remain elevated in the coming months, potentially putting further upward pressure on the IGP-M.

However, the contractual limitations on rental adjustments will continue to provide a buffer for many renters, preventing a direct and immediate pass-through of inflationary pressures. This creates a complex dynamic where the IGP-M signals broader economic risks, but the impact on a significant portion of the population is delayed, and mitigated. Investors should closely monitor the expiration of existing rental contracts and the terms of new leases to assess the potential for future rental income growth within the FII sector.