japan’s Consumer Price Index (CPI) spiked to its highest rate in over four decades, reaching 4.02% in January 2025 year-over-year, according to Statistics Japan.This surge surpasses teh previous peak seen in January 2023 and marks the worst inflation rate as 1981.

Core CPI, which excludes volatile fresh food and energy prices, accelerated to 3.2%, the highest level since June 2023. When excluding both fresh food and energy, inflation reached 2.6%. This figure is a crucial metric for the Bank of Japan’s (BOJ) 2% inflation target.

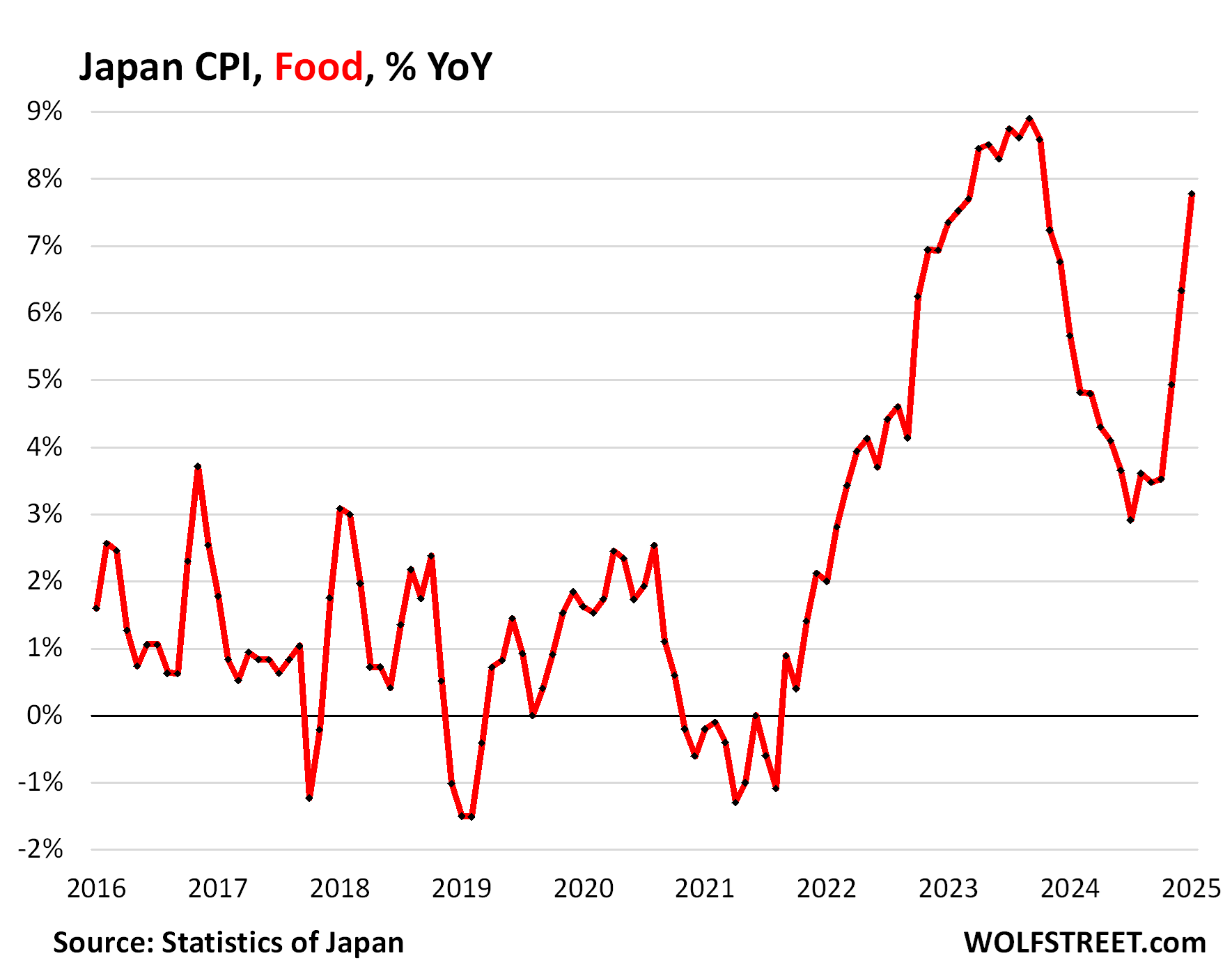

Thes figures highlight the growing strain on Japanese households, particularly as they allocate a larger portion of their spending to food then any other G7 nation. Fresh food prices surged by a staggering 7.8% year-over-year, driven by a 22.6% increase in fresh fruits and a 25.6% increase in vegetables.

Energy prices contributed considerably to the inflation surge, rising by 10.8% year-over-year.Electricity prices soared by 18.1%, while gas for home use increased by 6.2%. This spike in energy costs directly impacts household budgets, compounding the inflationary pressures on consumer spending.

To combat inflation, the BOJ has embarked on a gradual tightening cycle, raising its policy rate three times to 0.5% from its previous negative rate of -0.1%. Moreover,the BOJ initiated quantitative tightening (QT) in 2024,accelerating the process in 2025. However, these measures are implemented cautiously due to Japan’s enormous sovereign debt burden.

“The BOJ is clearly trying to resolve Japan’s sovereign debt problem, the biggest in the developed world, by fueling inflation to devalue that debt — along with everything else denominated in yen,”

The strategy, though, comes at a cost. With the BOJ’s policy rate at 0.5% and JGB yields at 1.34%, fixed-income investors in Japan face a situation where their returns are significantly eroded by the high inflation rate. This is in stark contrast to the US, where CPI stands at 3.0%, while the midpoint of the Federal Reserve’s policy rates is 4.33%, and the 10-year Treasury yield is at 4.5%,effectively compensating investors for inflation.

Japan’s debt-to-GDP ratio, at 254% in 2024, more than doubles the US ratio of 122%. This strategy, while aiming to manage the debt burden, ultimately shifts the negative consequences to Japanese households, who bear the brunt of higher prices and significantly diminished real returns on fixed-income investments. With decades of irresponsible fiscal policies, Japan faces a challenging path forward in addressing its financial challenges.

How does Japan’s historically high debt-to-GDP ratio complicate the Bank of Japan’s (BOJ) efforts to combat inflation?

Table of Contents

- 1. How does Japan’s historically high debt-to-GDP ratio complicate the Bank of Japan’s (BOJ) efforts to combat inflation?

- 2. Japan’s Inflation Crisis: An Interview with Dr. Yumi Nakamura,Economist at the Japan Center for Economic Research

- 3. archyde News: Dr.Nakamura, thank you for joining us today to discuss Japan’s inflation surge.

- 4. Can you walk us through the key figures from the recent CPI report?

- 5. Why are prices of fresh foods and energy surging so dramatically?

- 6. How is the BOJ responding to this inflation spike?

- 7. Can you explain how this strategy might impact fixed-income investors in Japan?

- 8. what do you see as the moast challenging aspect of managing Japan’s financial challenges moving forward?

- 9. do you think ther’s a risk Japan’s efforts to combat inflation could led to a recession?

Japan’s Inflation Crisis: An Interview with Dr. Yumi Nakamura,Economist at the Japan Center for Economic Research

archyde News: Dr.Nakamura, thank you for joining us today to discuss Japan’s inflation surge.

Dr. Yumi nakamura: Thank you for having me. The current inflation rate is indeed a pressing issue for japan right now.

Can you walk us through the key figures from the recent CPI report?

Dr. Nakamura: Of course. The January 2025 CPI report from Statistics Japan shows the annual inflation rate at 4.02%, the highest in over four decades. Core CPI, excluding fresh food and energy, reached 3.2%, and the core-core rate, excluding both, stood at 2.6%. This latter figure is importent as it’s the key metric for the Bank of Japan’s (BOJ) 2% inflation target.

Why are prices of fresh foods and energy surging so dramatically?

Dr.Nakamura: Fresh food prices are up by 7.8%, driven mainly by a surge in fruits (22.6%) and vegetables (25.6%). Energy prices have risen by 10.8%,with electricity up 18.1% and gas for home use by 6.2%. These increases are impacting household budgets substantially.

How is the BOJ responding to this inflation spike?

dr. Nakamura: The BOJ has initiated a gradual tightening cycle, raising its policy rate from -0.1% to 0.5%. They’ve also begun quantitative tightening, accelerating the process this year.Though, they’re proceeding cautiously due to Japan’s massive sovereign debt burden.

Can you explain how this strategy might impact fixed-income investors in Japan?

Dr. Nakamura: While the BOJ’s policy rate is at 0.5%, Japanese Government bond (JGB) yields stand at 1.34%. With CPI at 4.02%, returns for fixed-income investors are being significantly eroded by inflation. In contrast, in the US, investors are seeing returns that more than keep up with a 3.0% CPI.

what do you see as the moast challenging aspect of managing Japan’s financial challenges moving forward?

Dr. Nakamura: The debt-to-GDP ratio at 254% is a significant hurdle.The BOJ’s strategy aims to manage this debt burden, but it shifts the negative consequences to Japanese households, who bear the brunt of higher prices and diminished real returns on investments. Decades of irresponsible fiscal policies have led us to this point,making the path forward incredibly challenging.

do you think ther’s a risk Japan’s efforts to combat inflation could led to a recession?

Dr. Nakamura: (Thoughtfully) That’s a real concern.If the BOJ tightens monetary policy too quickly or harshly, it could indeed push the economy into recession. Striking the right balance between managing debt and not stifling economic growth will be crucial in the coming months.