Escalating tensions in the Middle East, specifically the ongoing U.S.-Israel operations in Iran and Iran’s subsequent restrictions on the Strait of Hormuz, are triggering a systemic economic shock. Oil prices have surged past $100 per barrel, equity markets are declining, and global supply chains are facing renewed disruption. This crisis threatens to derail the fragile global economic recovery, impacting energy-intensive industries and exacerbating inflationary pressures worldwide.

The Strait of Hormuz Blockade: A Calculated Risk with Global Repercussions

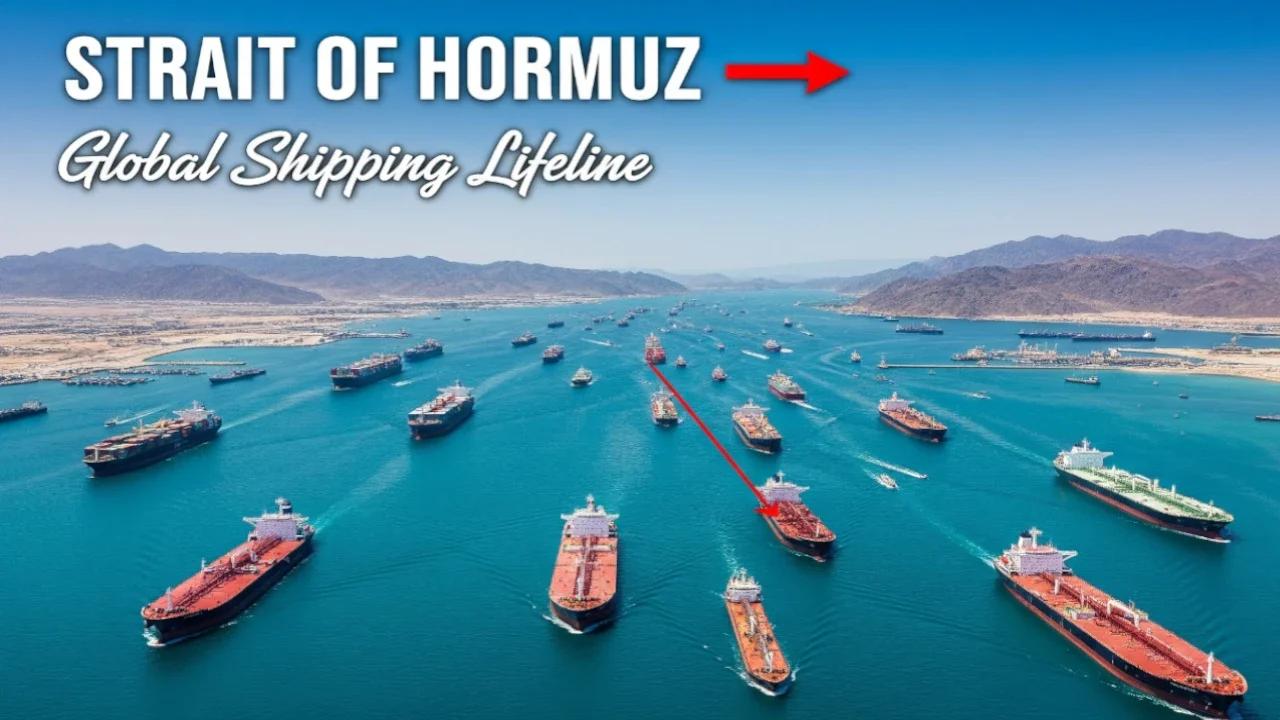

The immediate catalyst for this economic turbulence is Iran’s restriction of navigation through the Strait of Hormuz, a critical chokepoint for global energy supplies. Approximately 20% of the world’s oil passes through this waterway daily. As of March 29th, vessel traffic had plummeted to historical lows, with roughly 150 ships passing through compared to the typical 120 daily crossings, according to data analytics platform Kpler. This artificial constriction of supply has sent oil prices soaring. U.S. West Texas Intermediate crude for May delivery settled above $100 a barrel on Monday, March 31st, a level not seen since July 2022. Global benchmark Brent crude settled at $112.78 a barrel, poised for a record monthly gain exceeding 50% in March.

The Bottom Line

- Energy Price Volatility: Expect continued oil price volatility, potentially reaching $150 per barrel if the Strait of Hormuz remains significantly restricted for another month.

- Supply Chain Resilience Test: Companies reliant on Middle Eastern supply chains, particularly in petrochemicals and fertilizers, must immediately assess and diversify sourcing.

- Inflationary Pressure: The crisis will likely exacerbate existing inflationary pressures, forcing central banks to reassess monetary policy and potentially delaying interest rate cuts.

Beyond Oil: Ripple Effects Across Key Industries

The impact extends far beyond crude oil. The Strait of Hormuz is also a vital artery for agricultural goods and fertilizers. Gulf nations account for roughly one-third of global urea and nitrogen-based fertilizer exports. Disruptions to these shipments are already driving up fertilizer prices, threatening crop yields and potentially leading to higher food prices globally. Alpine Macro reports urea and ammonia prices have surged by approximately 50% and 20%, respectively, since the conflict began. This is a supply-side shock, leaving central banks with limited tools to combat rising costs, as Turkish economist Murat Tufan pointed out: “You cannot curb rising food costs through interest rate hikes alone when the primary drivers are external shocks to fuel and fertilizer.”

the conflict is impacting industrial gas supplies. Helium, crucial for semiconductor manufacturing and medical equipment, faces potential shortages due to disruptions among major producers, including Qatar. Aluminum prices have also climbed, with benchmark three-month aluminum on the London Metal Exchange briefly reaching $3,492 per metric ton during Monday’s trading, nearing a four-year peak. Petrochemical costs are rising, impacting industries from textiles to consumer packaging.

Logistical Nightmares and the Rerouting Calculus

The near-standstill in the Strait of Hormuz is creating significant logistical bottlenecks. S&P Global Market Intelligence estimates nearly 3,000 vessels are currently waiting nearby. Rerouting ships around Africa adds 3,500 nautical miles (6,482 km) and 10-14 days to voyages, mirroring the disruptions experienced during the 2022 Suez Canal blockage. West Coast Shipping notes that such diversions can increase transit times by 20%, severely impacting global supply chains.

Air transit hubs in Dubai, Abu Dhabi, and Doha have also been affected by Iranian strikes, disrupting cargo flows and creating headaches for industries reliant on temperature-sensitive goods, such as pharmaceuticals. One pharmaceutical executive, speaking anonymously to Reuters, warned of potential shortages of critical medicines within weeks if conditions don’t improve. The issue isn’t always a lack of medicine, but rather the availability of essential components, as David Weeks, director of supply chain risk management at Moody’s, highlighted: “In some cases, it’s the little stopper on the vial where the dosage is extracted.”

Market Reactions and Institutional Investor Sentiment

Global equity markets have reacted negatively to the escalating tensions. Major U.S. Indices have dropped by more than 7% since the fighting began, while the pan-European STOXX 600 index has slid over 8%. Asian markets have also experienced broad-based losses. The WTO estimates sustained high energy prices could reduce 2026 global GDP growth by 0.3 percentage points and lower trade growth by 0.5 percentage points. Consumer sentiment is also weakening; the University of Michigan Consumer Sentiment Index fell to a three-month low of 53.3 as war-related inflation worries mount.

| Index | Decline Since Conflict Start (March 1st, 2026) |

|---|---|

| S&P 500 | 7.3% |

| STOXX 600 | 8.1% |

| MSCI Asia Pacific | 6.5% |

| Brent Crude (Price Increase) | 52.8% |

The situation is forcing investors to reassess risk. BlackRock (NYSE: BLK), the world’s largest asset manager, has reportedly reduced its exposure to emerging markets and increased allocations to safe-haven assets like U.S. Treasury bonds.

“The geopolitical risk premium is now firmly embedded in market pricing,” says Mohamed El-Erian, President of Queens’ Gate Capital. “The potential for a wider regional conflict, coupled with the disruption to energy supplies, has fundamentally altered the investment landscape.” Bloomberg

Even **ExxonMobil (NYSE: XOM)**, typically benefiting from rising oil prices, faces uncertainty. While short-term profits are likely to increase, prolonged disruption could damage long-term demand and accelerate the transition to renewable energy sources. The company’s Q1 2026 earnings report, due in late April, will be closely watched for indications of how it’s navigating the crisis.

The Path Forward: De-escalation or Prolonged Economic Strain?

The trajectory of the global economy hinges on the resolution of the conflict. U.S. President Trump’s fluctuating rhetoric – initially threatening “total obliteration” of Iranian infrastructure, then signaling willingness to accept a closed Strait of Hormuz – underscores the unpredictable nature of the situation. The potential for miscalculation remains high.

If the Strait of Hormuz remains significantly restricted for an extended period, we can expect further escalation of oil prices, continued supply chain disruptions, and a slowdown in global economic growth. Companies must prioritize supply chain diversification, stress-test their operations against higher energy costs, and prepare for a prolonged period of uncertainty. The current crisis serves as a stark reminder of the interconnectedness of the global economy and the vulnerability of supply chains to geopolitical shocks.

The OECD has already cut its eurozone growth forecast for 2026 to 0.8% and raised its inflation outlook to 2.6%. These revisions are likely to be further adjusted downward if the situation deteriorates.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.