Escalating tensions in the Middle East, specifically surrounding potential conflict with Iran, are placing significant downward pressure on oilfield services companies. Analysts predict reduced capital expenditure from national oil companies (NOCs) and international oil companies (IOCs) operating in the region, alongside increased geopolitical risk premiums. This translates to project delays, contract renegotiations, and a potential decline in revenue for key players. The impact is already being reflected in market sentiment, with sector-specific ETFs experiencing increased volatility.

The Shifting Sands of Middle Eastern Energy Investment

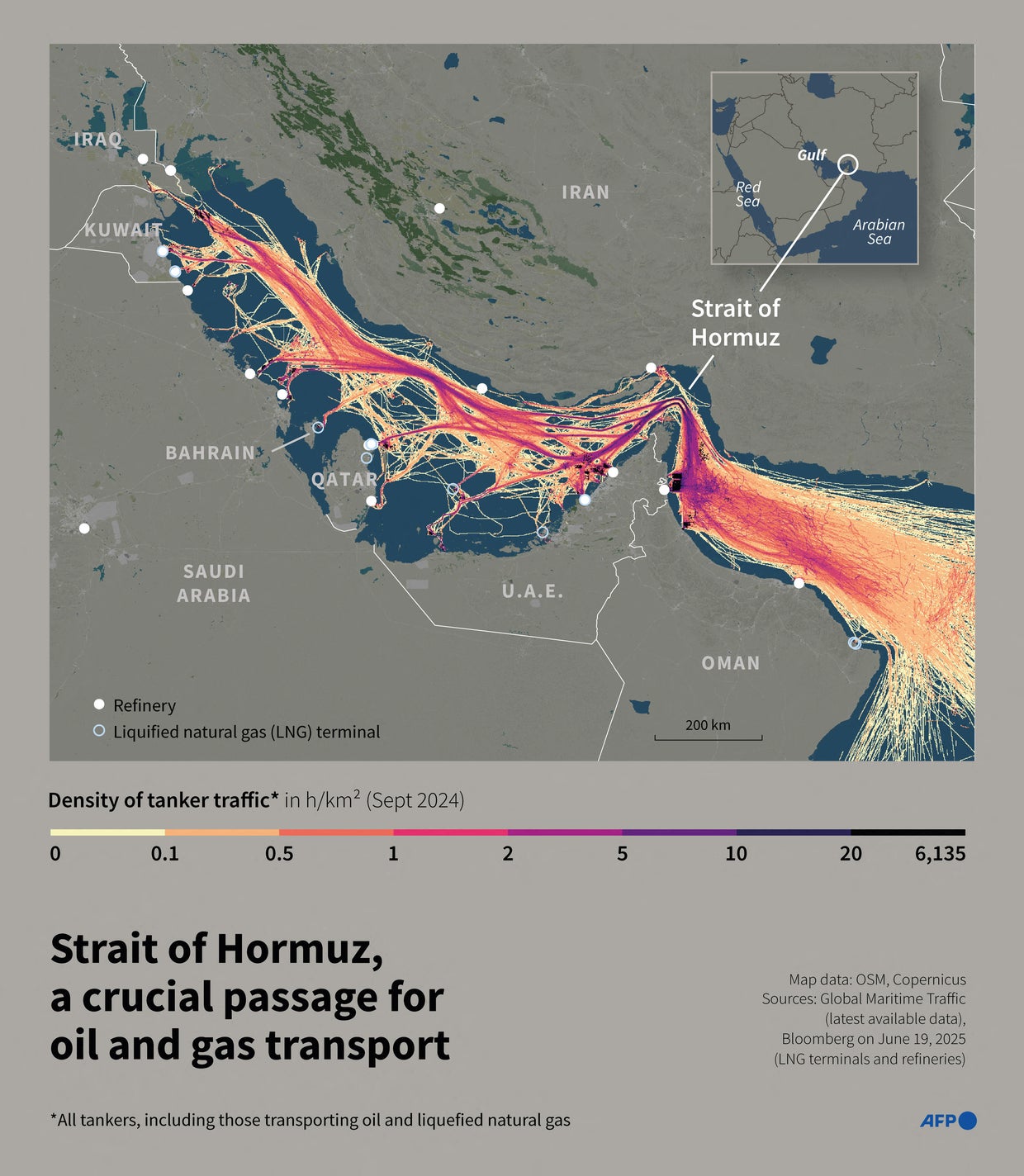

The immediate concern stems from the potential disruption to oil production and transportation routes in the Persian Gulf. While a full-scale war remains uncertain, the heightened risk is prompting companies to reassess their investments. Reuters reported in January that Iranian oil exports were already at record highs despite sanctions, indicating a complex geopolitical landscape even *before* the current escalation. This existing volatility is now amplified. The focus is shifting from expansion to risk mitigation, impacting companies heavily reliant on projects in Saudi Arabia, Iraq, and the UAE.

The Bottom Line

- Reduced Capex: Expect a 10-15% reduction in capital expenditure by major NOCs and IOCs in the region over the next 12-18 months.

- Contract Risk: Existing contracts, particularly those with force majeure clauses, are likely to be scrutinized and potentially renegotiated, impacting revenue recognition.

- Sector Rotation: Investors are shifting capital away from oilfield services towards perceived safer havens, creating potential buying opportunities for long-term investors.

Halliburton, Schlumberger, and Baker Hughes: A Sector Under Scrutiny

The impact isn’t uniform. **Halliburton (NYSE: HAL)**, **Schlumberger (NYSE: SLB)**, and **Baker Hughes (NYSE: BKR)** – the industry’s giants – are all exposed, but to varying degrees. Schlumberger, with its broader international footprint and focus on technology, may be slightly better positioned to weather the storm. However, all three companies are likely to experience headwinds. The Wall Street Journal highlights that a sustained increase in oil prices, while potentially benefiting producers, could also dampen global demand, ultimately impacting service company activity.

Here is the math. As of March 26, 2026, Halliburton’s market capitalization stood at $28.5 billion, Schlumberger at $62.1 billion, and Baker Hughes at $35.2 billion. A 10% decline in revenue across the board would translate to roughly $2.85 billion, $6.21 billion, and $3.52 billion in lost revenue, respectively. These figures don’t account for potential cost-cutting measures or shifts in operational focus.

| Company | Ticker | Market Cap (USD Billions – March 26, 2026) | 2025 Revenue (USD Billions) | Q1 2026 Revenue (USD Billions) | YOY Q1 Revenue Growth |

|---|---|---|---|---|---|

| Halliburton | NYSE: HAL | 28.5 | 29.8 | 7.1 | -3.2% |

| Schlumberger | NYSE: SLB | 62.1 | 65.4 | 15.8 | -1.1% |

| Baker Hughes | NYSE: BKR | 35.2 | 37.1 | 8.9 | -4.5% |

But the balance sheet tells a different story. Companies with strong balance sheets and diversified revenue streams will be better equipped to navigate the uncertainty. The long-term demand for energy, even with the growth of renewables, ensures that oilfield services will remain relevant for decades to come. The question is *how* the industry adapts.

Beyond the Gulf: Supply Chain Disruptions and Inflationary Pressures

The impact extends beyond the immediate region. Disruptions to oil supply could exacerbate existing inflationary pressures, particularly in transportation and manufacturing. This, in turn, could lead to higher interest rates and a slowdown in global economic growth. The energy sector is intricately linked to the broader economy, and a shock in one area can ripple through multiple industries. Bloomberg analysts are already warning of a potential spike in oil prices, potentially exceeding $100 per barrel, if the conflict escalates significantly.

Expert Perspectives on the Looming Crisis

“We are seeing a clear flight to safety in the energy sector. Investors are rotating out of companies with significant exposure to the Middle East and into those with more stable geopolitical profiles. This trend is likely to continue until there is a clear de-escalation of tensions.” – Dr. Emily Carter, Chief Investment Officer, Horizon Asset Management (March 27, 2026)

the situation is forcing companies to re-evaluate their supply chains. Reliance on materials and components sourced from the Middle East is being questioned, leading to a search for alternative suppliers. This could drive up costs in the short term but ultimately enhance supply chain resilience.

The Long Game: Adapting to a New Energy Landscape

The current crisis underscores the need for oilfield services companies to diversify their offerings and invest in new technologies. Focusing on carbon capture, utilization, and storage (CCUS), geothermal energy, and hydrogen production could provide new revenue streams and reduce reliance on traditional oil and gas. **Saudi Aramco (Tadawul: 2222)**, for example, is heavily investing in CCUS technologies, creating opportunities for service companies with expertise in this area. The shift towards a lower-carbon future is inevitable, and companies that embrace this transition will be best positioned for long-term success.

The situation is fluid and requires constant monitoring. The potential for escalation remains high, and the impact on the oilfield services sector could be significant. However, with careful planning, strategic diversification, and a focus on innovation, companies can navigate these challenges and emerge stronger in the long run. The key is to anticipate the evolving geopolitical landscape and adapt accordingly.