Labor Day 2025: Financial Strain Drives Hospitals to Employ Aggressive Debt Collection Tactics

Table of Contents

- 1. Labor Day 2025: Financial Strain Drives Hospitals to Employ Aggressive Debt Collection Tactics

- 2. The Rise of ‘revenue Bounty Hunters’

- 3. The Impact of Medical Debt on Credit Scores

- 4. “Buy Now, Pay Later” and the Cycle of Debt

- 5. Tariffs and Household budgets

- 6. Looking Ahead: Long-Term Financial Health

- 7. Frequently Asked Questions

- 8. What is a “revenue bounty hunter?”

- 9. How do tariffs impact household spending?

- 10. What is “buy now, pay later” (BNPL)?

- 11. Why is medical debt a significant problem?

- 12. what resources are available for managing medical debt?

- 13. How can consumers protect themselves from aggressive debt collection tactics employed by “revenue bounty hunters”?

- 14. Labor Day 2025: Navigating Financial Challenges for U.S. Consumers

- 15. The Rise of “Revenue Bounty Hunters” and Debt Collection

- 16. Medical Debt’s Return to FICO Scores: A Setback for many

- 17. “cute Debt” and the Normalization of Consumer Credit

- 18. Tariff Impacts and the Cost of Goods: A Hidden Financial Strain

- 19. Protecting Your Financial Health: Practical tips

As the United States observes Labor day in 2025, a confluence of economic factors is placing immense pressure on working families. Rising costs, coupled with the re-emergence of tariffs impacting everyday goods, are squeezing household budgets, while a growing trend in healthcare debt collection is adding to the burden.

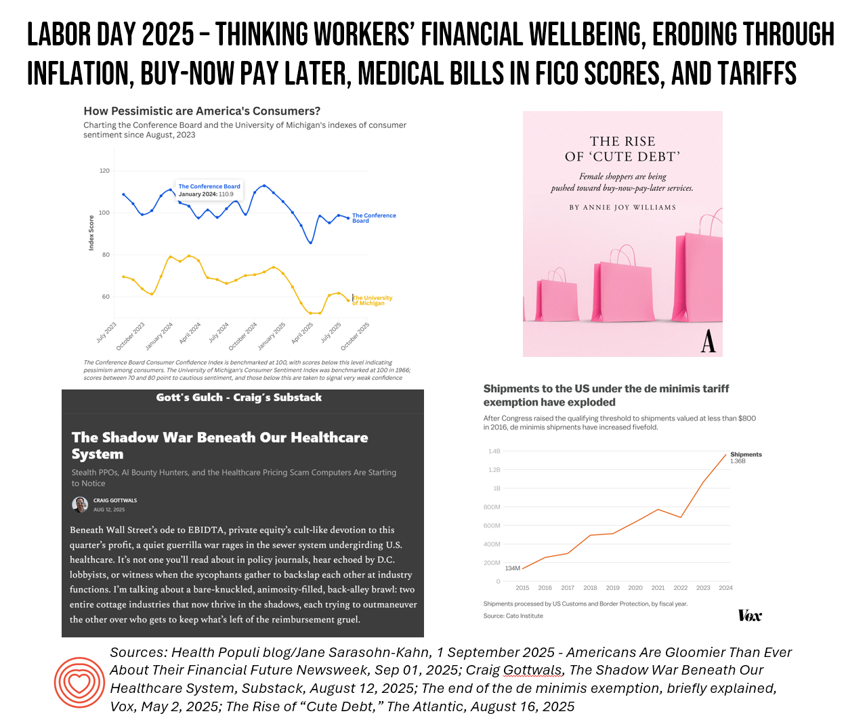

The Rise of ‘revenue Bounty Hunters’

Hospitals, grappling with underpayments and increasing financial instability, are now enlisting the services of specialized firms dubbed “revenue bounty hunters.” these companies utilize Artificial Intelligence systems to identify and pursue outstanding medical bills, a practice that raises concerns about aggressive debt collection tactics. This shift reflects a growing trend within the healthcare industry, spurred by a lack of openness in pricing and complex billing procedures.

Experts describe this emergence as an escalation of two “shadow industries” thriving within the U.S. healthcare system: opaque network pricing and AI-driven revenue recovery. Absent significant reforms,this “arms race” is likely to intensify,further obscuring the true cost of care.

The Impact of Medical Debt on Credit Scores

Medical debt has long been a significant contributor to personal bankruptcies, impacting the financial stability of countless Americans. Earlier this year, the Biden-Harris administration implemented a rule removing medical debt from credit score calculations, aiming to alleviate some of this pressure. However, a recent court ruling in July 2025 reversed this policy, once again factoring medical bills into FICO scores. This reversal poses a threat to the financial wellbeing of individuals already struggling to manage healthcare costs.

“Buy Now, Pay Later” and the Cycle of Debt

Adding to the financial strain is the growing popularity of “buy now, pay later” (BNPL) services. While initially marketed as a convenient payment option, these plans can lead to a cycle of debt, especially among women who are disproportionately affected by financial disparities. The allure of immediate purchases coupled with rising costs from tariffs creates a perfect storm for increased consumer debt.

Tariffs and Household budgets

Recent data indicates that the impact of tariffs is beginning to be felt across a wide range of household expenses. A recent survey anticipates a surge in “tariff survival” shopping this Labor Day, as consumers attempt to preemptively purchase goods before prices increase further. This trend is expected to continue throughout the holiday season, intensifying the financial pressure on families.

| Factor | Impact |

|---|---|

| Rising tariffs | Increased costs for everyday goods, impacting household budgets. |

| Medical Debt | Negative impact on credit scores, leading to financial instability. |

| BNPL Services | Potential for a cycle of debt, particularly for vulnerable populations. |

| AI Debt Collection | more aggressive attempts to recover medical bills. |

Did You Know? The Consumer Financial Protection Bureau (CFPB) estimates that medical debt affects over 100 million Americans.

Pro Tip: Prioritize financial planning and explore options for managing medical debt, such as payment plans or debt consolidation.

As Americans navigate these challenging economic times, it is crucial to prioritize financial wellness and advocate for policies that promote affordability and transparency in healthcare.

Looking Ahead: Long-Term Financial Health

The issues highlighted today are not isolated incidents but rather symptoms of deeper systemic problems within the U.S. economy. Addressing these challenges requires a multi-faceted approach, encompassing healthcare reform, responsible trade policies, and enhanced consumer protections. Long-term financial stability will depend on creating a more equitable and enduring economic habitat.

Frequently Asked Questions

What is a “revenue bounty hunter?”

A “revenue bounty hunter” is a firm hired by hospitals to aggressively pursue unpaid medical bills,frequently enough using Artificial Intelligence to identify and collect debts.

How do tariffs impact household spending?

Tariffs increase the cost of imported goods, which can lead to higher prices for consumers on a wide range of products.

What is “buy now, pay later” (BNPL)?

BNPL is a short-term financing option that allows consumers to make purchases and pay them off in installments, but it can lead to debt accumulation.

Why is medical debt a significant problem?

Medical debt can negatively impact credit scores, limit access to financial opportunities, and contribute to personal bankruptcies.

what resources are available for managing medical debt?

Consumers can explore options such as payment plans, debt consolidation, and financial assistance programs.

What are your biggest concerns about the current economic climate? Share your thoughts in the comments below!

How can consumers protect themselves from aggressive debt collection tactics employed by “revenue bounty hunters”?

The Rise of “Revenue Bounty Hunters” and Debt Collection

As Labor Day 2025 arrives, many U.S. consumers are facing a complex financial landscape. A significant contributor to this is the increasingly aggressive tactics of debt collection agencies, often referred to as “revenue bounty hunters.” These agencies, fueled by the sale of debt portfolios, are employing more assertive methods to recover funds, impacting credit scores and financial well-being.

Debt Buying: Companies purchase debts for pennies on the dollar, often from original creditors.This allows them to profit significantly even with minimal recovery.

Aggressive Tactics: These can include frequent phone calls,letters,and even legal action,sometimes targeting individuals with limited financial resources.

Statute of Limitations: Understanding the statute of limitations on debt is crucial. While a debt collector can still attempt to collect, they may not be able to legally sue after a certain period (which varies by state).

Debt Validation: Consumers have the right to request debt validation – a written verification of the debt’s legitimacy. This is a powerful tool to challenge inaccurate or fraudulent claims.

Keywords: debt collection, revenue bounty hunters, debt buying, statute of limitations, debt validation, financial hardship, credit score, debt relief.

Medical Debt’s Return to FICO Scores: A Setback for many

A major shift impacting financial health is the reintroduction of medical debt to FICO scores in 2023, after a temporary suspension during the pandemic. While FICO 9 and 10 models treat paid medical debt differently, and smaller amounts are less impactful, unpaid medical debt can still significantly lower a credit score.

Impact on Creditworthiness: Even relatively small medical bills can negatively affect a consumer’s ability to secure loans, mortgages, and even rent an apartment.

Surprise Billing: The ongoing issue of surprise medical bills continues to contribute to unexpected debt.

No-Surprise Act: While the No Surprise act aims to protect consumers from exorbitant out-of-network charges, navigating the process can be complex.

Financial Assistance Programs: Many hospitals offer financial assistance programs or payment plans for patients struggling to afford their bills. Researching these options before a bill goes to collections is vital.

Keywords: medical debt, FICO score, credit score, surprise billing, No Surprise Act, healthcare costs, financial assistance, medical billing.

“cute Debt” and the Normalization of Consumer Credit

The term “cute debt” refers to the increasing acceptance of small-balance debts, often accumulated through “buy now, pay later” (BNPL) services. While seemingly harmless, these small debts can quickly add up and negatively impact credit utilization ratios.

BNPL Risks: BNPL services often lack the same consumer protections as customary credit cards. Late fees and potential credit reporting issues are concerns.

Credit Utilization: Keeping credit utilization (the amount of credit used compared to the total credit available) low is crucial for a good credit score.Multiple BNPL accounts can strain this ratio.

Overspending: The ease of BNPL can encourage overspending and lead to a cycle of debt.

Openness: Consumers should carefully review the terms and conditions of BNPL agreements, paying close attention to interest rates, fees, and reporting practices.

Keywords: cute debt, buy now pay later (BNPL), credit utilization, consumer credit, debt accumulation, financial responsibility, installment loans.

While often overlooked in personal finance discussions, tariffs – taxes imposed on imported goods – contribute to higher prices for consumers. The ongoing trade tensions and tariff policies have a ripple effect on the cost of everyday items.

Increased Consumer Prices: Tariffs are frequently enough passed on to consumers in the form of higher prices for goods,reducing purchasing power.

Supply Chain Disruptions: Tariffs can disrupt supply chains, leading to shortages and further price increases.

Inflationary Pressure: Tariffs contribute to overall inflationary pressure, making it more expensive to maintain a standard of living.

Impact on Specific Sectors: Certain sectors, like electronics, apparel, and automobiles, are particularly vulnerable to tariff impacts.

Keywords: tariffs, trade policy, inflation, consumer prices, cost of goods, supply chain, economic impact, purchasing power.

Protecting Your Financial Health: Practical tips

Navigating these challenges requires proactive financial management. Here are some actionable steps:

- Budgeting: Create a detailed budget to track income and expenses.

- Credit Monitoring: Regularly monitor your credit report for errors and fraudulent