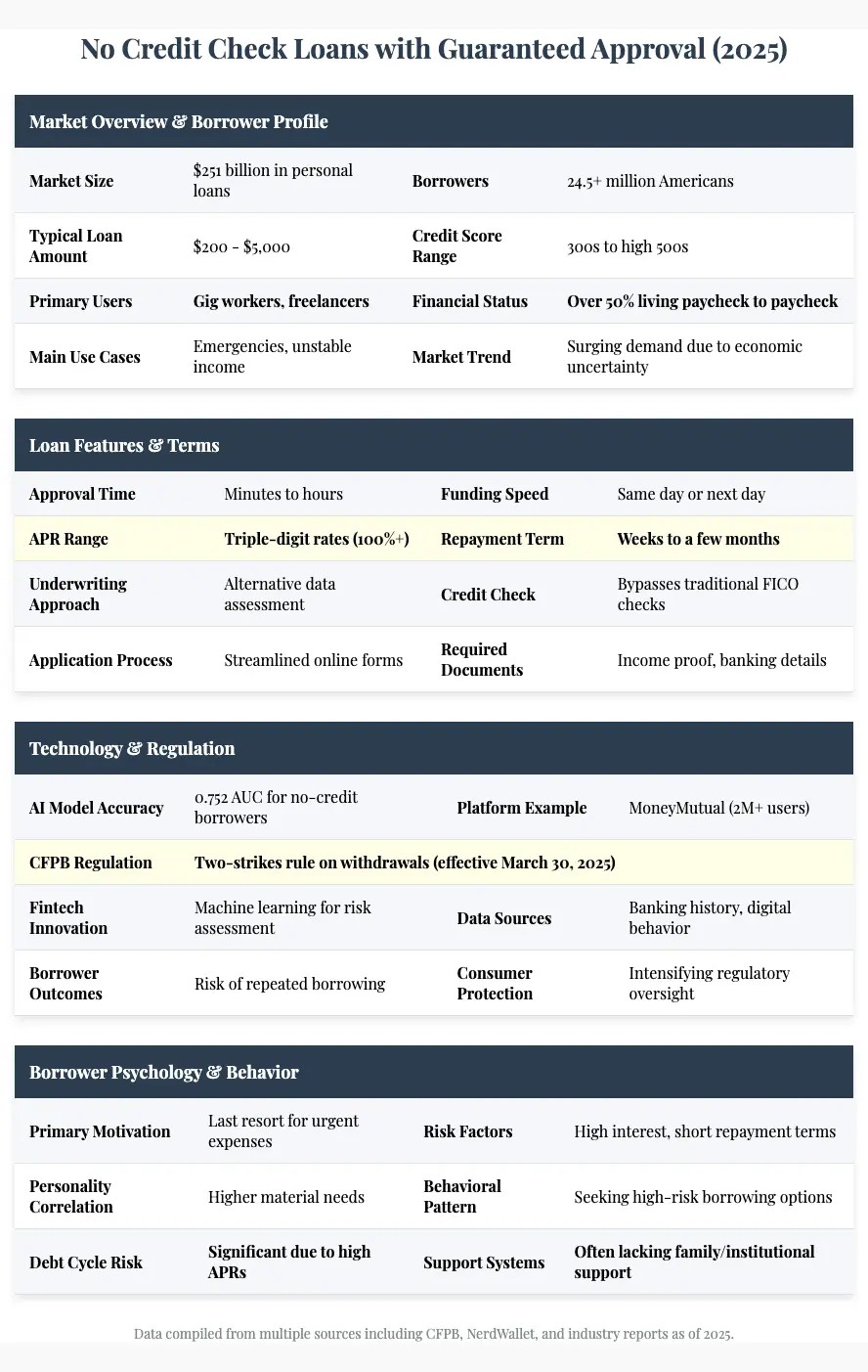

Securing a “Kredit ohne Schufa und Einkommensnachweis” (loans without credit checks or income proof) in Germany is a high-risk financial maneuver. While fintechs and niche lenders offer immediate payouts, these products typically feature predatory interest rates and stringent collateral requirements to offset the lack of traditional credit scoring.

This isn’t just a consumer finance quirk; it is a barometer for the current liquidity crisis facing the German “Mittelstand” and the freelance economy. As we move into the second quarter of 2026, the demand for non-traditional credit has surged as traditional banks tighten lending standards in response to volatile ECB interest rate trajectories. When the traditional banking sector closes its doors, the “shadow banking” sector—comprising P2P platforms and unregulated lenders—steps in to capture the risk premium.

The Bottom Line

- Risk Premium: Loans without income proof carry APRs significantly higher than standard consumer loans, often exceeding 12-15%.

- Credit Gap: The rise of “no-Schufa” loans indicates a growing segment of the population locked out of the primary financial system.

- Regulatory Heat: BaFin is increasing scrutiny on fintech lenders to prevent systemic debt traps in the consumer sector.

The Mechanics of Risk: Why “No Schufa” is a Misnomer

First, let’s be clear: no professional lender ignores risk. If a lender claims to ignore the SCHUFA Holding AG (the primary German credit agency), they aren’t ignoring risk; they are simply pricing it differently. They replace the credit score with alternative data or high-interest buffers.

Here is the math. In a standard loan, the interest rate is a reflection of the probability of default. When you remove the income proof and the credit score, the probability of default spikes. To maintain a positive expected value, the lender must increase the interest rate to a level that covers the anticipated losses across their entire portfolio.

But the balance sheet tells a different story. Many of these “immediate payout” loans are actually short-term bridge loans disguised as consumer credit. They are designed for velocity, not stability. For the borrower, this creates a “debt spiral” where the cost of servicing the loan exceeds the original liquidity require.

Macroeconomic Pressure and the Fintech Pivot

The shift toward these products is closely tied to the broader European economic landscape. With inflation remaining sticky and the European Central Bank (ECB) maintaining a restrictive stance, the cost of capital has risen. This has disproportionately affected freelancers and small business owners who lack the rigid payroll structures required by legacy banks like Deutsche Bank (ETR: DBK).

we are seeing a pivot in the fintech sector. Companies are moving away from “growth at all costs” and toward “risk-adjusted yield.” By offering loans to the under-banked, these platforms are essentially harvesting a high-yield niche that traditional banks find too administratively expensive to manage.

Consider the impact on the broader economy. When a significant portion of the workforce relies on high-interest, non-traditional credit to maintain consumption, it creates a fragile floor for GDP growth. Any further contraction in the labor market could lead to a spike in defaults that ripples through the fintech ecosystem.

| Loan Type | Avg. Interest Rate (APR) | Approval Speed | Risk Level |

|---|---|---|---|

| Traditional Bank Loan | 3.5% – 7.0% | 3-7 Days | Low |

| Fintech Credit (with Schufa) | 5.0% – 11.0% | Instant/24h | Moderate |

| No-Schufa/No-Income Loan | 12.0% – 20.0%+ | Immediate | Extreme |

The Regulatory Wall: BaFin and the Future of Lending

The German Federal Financial Supervisory Authority, BaFin, is not watching this trend with indifference. There is a growing movement to standardize “alternative credit scoring” to prevent predatory lending. If BaFin mandates stricter transparency on “effective interest rates,” many of the current “immediate payout” models will become unprofitable overnight.

The tension here is between financial inclusion and financial stability. While these loans provide a lifeline, they often act as a bridge to nowhere. Institutional investors are beginning to price in this regulatory risk, leading to a cooling of VC funding for “disruptive” lending apps that lack robust underwriting frameworks.

“The proliferation of unsecured, high-interest consumer credit in the Eurozone is a lagging indicator of systemic stress. When the primary credit market fails, the secondary market doesn’t solve the problem—it merely monetizes the desperation.”

This sentiment is echoed across the Bloomberg terminals, where analysts are tracking the correlation between rising “no-Schufa” search volumes and declining consumer confidence indices.

Strategic Outlook for the Borrower and the Market

For the individual, the “immediate payout” is a tactical win but a strategic failure. The cost of capital in these instruments is designed to erode wealth, not build it. A more sustainable approach involves the use of Reuters-tracked credit restructuring tools or seeking government-backed micro-loans for the self-employed.

Looking ahead to the rest of 2026, expect a consolidation in the fintech lending space. The “wild west” era of ignoring income proof is ending as the cost of defaults rises. We will likely see a shift toward “hybrid scoring,” where lenders use open banking data (real-time transaction analysis) instead of static Schufa scores to determine creditworthiness.

The trajectory is clear: the market is moving toward hyper-personalized risk pricing. Those who can provide transparent, real-time data will see rates drop; those who rely on “no-proof” loans will find themselves paying a premium that is mathematically unsustainable.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.