{kind=link}

Table of Contents

- 1. Medicare Part D premiums: A Looming Question for 2026

- 2. How might the frequent formulary changes in PDPs disrupt established treatment plans for beneficiaries?

- 3. Medicare’s Stand-Alone drug Plans: A rocky Road Ahead

- 4. Understanding Medicare Part D & Stand-Alone Plans

- 5. The Rising Cost of Prescription Drugs: A Major Hurdle

- 6. The Coverage Gap (“Donut Hole”) – Still a Concern

- 7. plan Complexity & Beneficiary Confusion

- 8. Impact on Healthcare Providers

- 9. Practical Tips for Navigating PDPs

The landscape of Medicare prescription drug coverage is facing a meaningful juncture as the future of the Part D premium stabilization presentation remains uncertain for 2026. This demonstration, designed to temper premium increases for stand-alone Prescription Drug Plans (PDPs), has drawn both praise and scrutiny, wiht its continuation hanging in the balance.

The core of the issue lies in the potential impact on beneficiaries, especially those in traditional Medicare and rural areas. While a vast majority of Medicare Advantage Prescription Drug (MA-PD) enrollees currently enjoy no-premium drug coverage, a substantial portion of PDP enrollees face higher costs. The stabilization demonstration aims to bridge this gap by moderating the premium increases for PDPs.

Recently, the U.S. Government Accountability Office (GAO) issued a legal opinion stating that the demonstration aligns with the authority granted to the Secretary of Health and Human Services. This assessment, requested by Republican members of the House and Senate, lends a degree of legitimacy to the program.However, it does not obligate any future administration to maintain it.

The Trump administration has yet to signal its intentions regarding the demonstration for 2026, with an announcement expected later in July. The decision could have profound implications.If the demonstration continues, it could help ensure that Medicare beneficiaries relying on PDPs have access to relatively affordable prescription drug coverage.

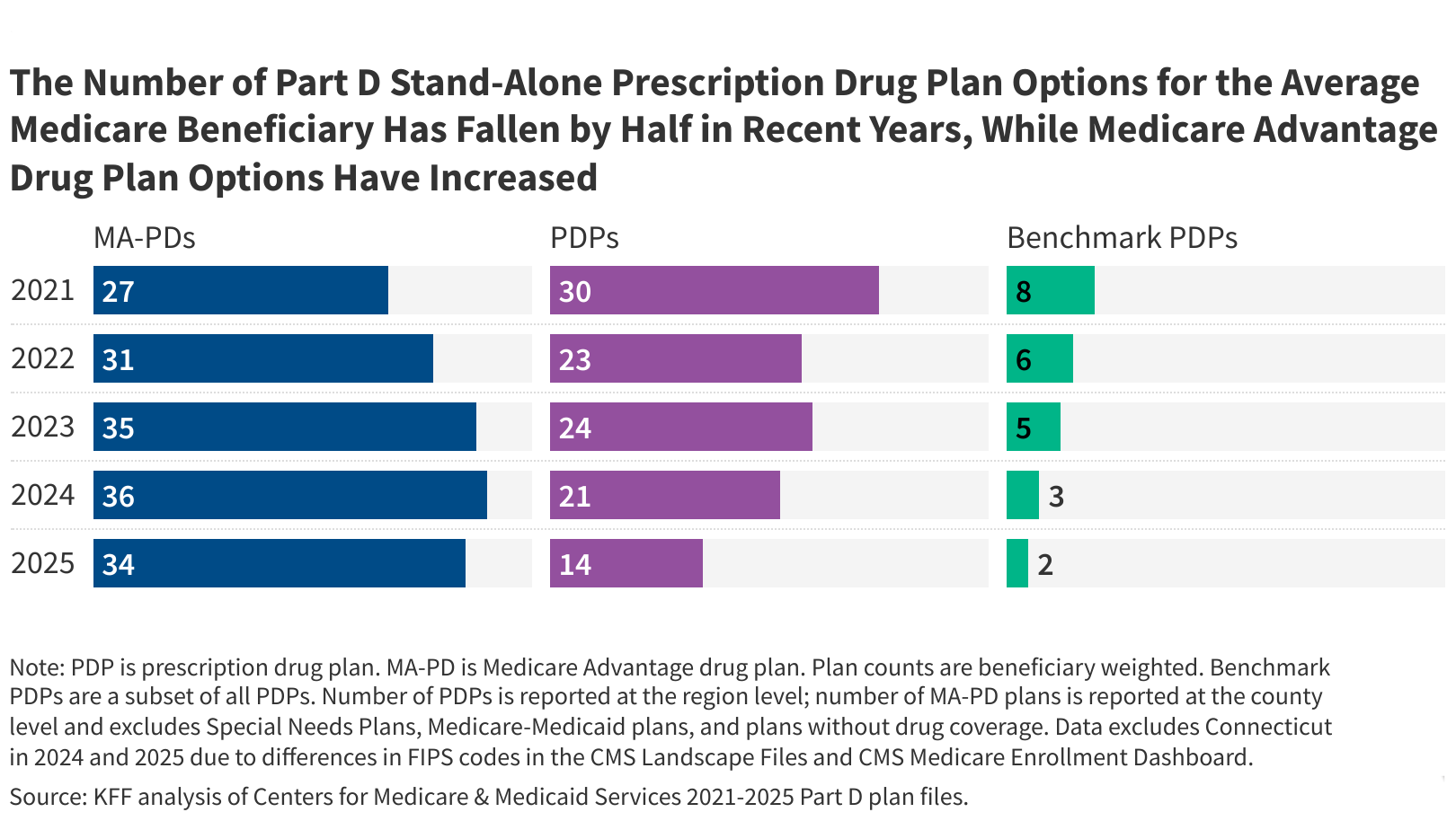

plan-specific Part D premiums for 2026 will be unveiled in the fall. Projections suggest that MA-PDs will continue to offer lower average monthly premiums than pdps, a trend observed in 2025 where MA-PDs averaged $7 per month compared to PDPs’ $39. This significant difference is partly attributed to MA-PD sponsors utilizing rebates to reduce their Part D component of the premium.

Though, this premium gap could widen considerably if the administration scales back or terminates the PDP premium stabilization demonstration. Such a move could also lead to a further reduction in the availability of PDP options. This scenario, in turn, might accelerate the migration of beneficiaries from traditional Medicare to Medicare Advantage plans. Given that Medicare Advantage typically incurs higher per-beneficiary federal spending, a significant shift could translate to increased overall federal expenditures in the long run. The future of affordable Part D coverage, therefore, hinges on the upcoming decisions regarding this critical demonstration.

How might the frequent formulary changes in PDPs disrupt established treatment plans for beneficiaries?

Medicare’s Stand-Alone drug Plans: A rocky Road Ahead

Understanding Medicare Part D & Stand-Alone Plans

Medicare Part D provides prescription drug coverage for Medicare beneficiaries.While many choose to receive this coverage through a Medicare Advantage plan (MA-PD), a important number opt for stand-alone prescription drug plans (PDPs). These PDPs are offered by private insurance companies approved by medicare.However, the landscape of these plans is becoming increasingly complex, presenting challenges for both beneficiaries and healthcare providers. As of 2025, navigating these plans requires a deeper understanding of their intricacies. Australia’s Medicare system, as highlighted by the Department of Health (https://www.health.gov.au/sites/default/files/2025-02/what-is-medicare-easy-read-fact-sheet.pdf),emphasizes global healthcare access,a principle that underscores the importance of accessible and affordable prescription drug coverage within the US Medicare system.

The Rising Cost of Prescription Drugs: A Major Hurdle

The most significant challenge facing pdps is the escalating cost of prescription drugs.

Specialty Medications: The price of specialty medications – often used to treat complex conditions like cancer, rheumatoid arthritis, and multiple sclerosis – continues to soar. These drugs represent a disproportionately large share of overall drug spending.

Inflation Reduction Act Impact: While the Inflation Reduction Act (IRA) aims to lower drug costs, its full impact is still unfolding. The negotiation of prices for select drugs is a positive step, but it doesn’t address the cost of all medications.

Formulary Changes: PDPs frequently adjust their formularies (lists of covered drugs), potentially forcing beneficiaries to switch medications or face higher out-of-pocket costs. This instability creates anxiety and disruption in treatment plans.

Tiered Cost-Sharing: Most PDPs utilize a tiered cost-sharing structure, where drugs are categorized into different tiers with varying copayments or coinsurance. Navigating these tiers and understanding which drugs fall into which category can be confusing.

The Coverage Gap (“Donut Hole”) – Still a Concern

Although significantly narrowed by the Affordable Care Act, the Medicare Part D coverage gap, often called the “donut hole,” remains a concern for some beneficiaries. this gap occurs after a beneficiary and their plan have spent a certain amount on covered drugs.

Catastrophic Coverage: once spending reaches the catastrophic level, Medicare pays the vast majority of drug costs for the remainder of the year. However, reaching this level requires ample out-of-pocket spending.

Manufacturer Discounts: Pharmaceutical manufacturers are required to provide discounts on brand-name drugs during the coverage gap, but these discounts don’t always fully offset the cost.

plan Complexity & Beneficiary Confusion

The sheer number of PDPs available – often varying by region – contributes to significant beneficiary confusion.

Annual Enrollment Period: The annual enrollment period (October 15 – December 7) is a critical time for beneficiaries to review their options and choose a plan that meets their needs. However, many struggle to understand the differences between plans.

plan Finder tool: Medicare’s Plan Finder tool (https://www.medicare.gov/plan-compare/) can be helpful, but it requires beneficiaries to accurately estimate their drug costs and usage.

Limited Enrollment Windows: Outside of the annual enrollment period,beneficiaries generally only have limited opportunities to switch plans.

Star Ratings: Medicare assigns star ratings to PDPs based on their performance in various areas, such as drug coverage, customer service, and member satisfaction. These ratings can be a useful guide, but they shouldn’t be the sole basis for decision-making.

Impact on Healthcare Providers

The challenges with PDPs also impact healthcare providers.

Prior Authorizations: Obtaining prior authorizations from PDPs for certain medications can be time-consuming and burdensome for physicians and their staff.

Formulary Restrictions: Formulary restrictions can limit a physician’s ability to prescribe the most appropriate medication for a patient.

Patient Affordability: Providers frequently enough encounter patients who are unable to afford their medications due to high out-of-pocket costs, leading to non-adherence and poorer health outcomes.

Administrative Burden: Dealing with multiple PDPs and their varying requirements adds to the administrative burden for healthcare practices.

Review Your Medications: Create a comprehensive list of all your medications,including dosages and frequency.

Estimate Your Annual Drug costs: Accurately estimate your annual drug costs to help you choose a plan with appropriate coverage.

Compare Plans Carefully: Use the Medicare Plan Finder tool and compare plans based on premiums, deductibles, copayments, coinsurance, and formularies.

Check the Formulary: Ensure that your medications are covered by the plan’s formulary and understand the cost-sharing requirements.

consider Your Pharmacy Network: Choose a plan that includes your preferred pharmacy in its network.

**Seek Assistance