To qualify for the long-term mortgage interest deduction during parental leave in South Korea, the taxpayer must maintain their status as a “worker” with earned income. While parental leave pauses active salary, the employment relationship persists, allowing eligible joint-owners to claim deductions provided they meet the National Tax Service (NTS) income thresholds for the fiscal year.

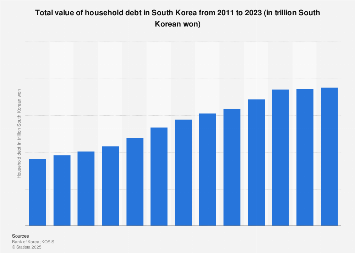

This technicality is more than a tax query; it is a microcosm of South Korea’s broader struggle to balance fiscal stability with an aggressive demographic crisis. As the government attempts to incentivize childbirth through tax breaks and subsidies, the intersection of labor laws and tax code becomes a critical lever for maintaining middle-class disposable income. In an environment where household debt-to-GDP ratios remain among the highest in the OECD, these deductions act as a vital buffer against interest rate volatility.

The Bottom Line

- Eligibility Persistence: Parental leave does not terminate “worker” status; although, the deduction is contingent upon having actual earned income during the taxable year.

- Macroeconomic Buffer: Tax deductions for mortgage interest serve as a non-monetary subsidy that mitigates the impact of the Bank of Korea (BOK) interest rate pivots on household consumption.

- Strategic Planning: Joint-ownership structures allow for a tactical shift in deduction claims between spouses to optimize the overall family tax burden during periods of income fluctuation.

The Mechanics of Mortgage Deductions During Leave

The core of the issue lies in the definition of a “worker” under the Income Tax Act. For a joint-owner to claim the long-term mortgage interest deduction, they must be a resident worker. When an employee takes parental leave, they are not resigning; they are in a state of suspended active duty. If the individual earned a salary for any portion of the year—even just three months, as noted in the source—they generally retain their status as a worker.

But the balance sheet tells a different story when calculating the actual benefit. The deduction is applied against the earned income. If the parental leave results in a significant drop in annual taxable income, the “tax shield” provided by the mortgage interest may be underutilized. Here is the math: the deduction reduces the taxable income base, not the final tax bill directly. If the income drops below the basic deduction threshold, the marginal utility of the mortgage interest deduction effectively hits zero.

This creates a strategic gap for families. In joint-ownership scenarios, the ability to allocate the deduction to the spouse with the higher marginal tax rate is the primary goal. However, the law requires the person claiming the deduction to be the actual borrower and the house owner. This rigidity often clashes with the fluid nature of modern dual-income household labor patterns.

Household Debt and the 2026 Macroeconomic Backdrop

As we move into the second quarter of 2026, the South Korean economy is navigating a precarious path. The Bank of Korea (BOK) has spent the last 18 months calibrating rates to curb inflation while preventing a hard landing for the real estate market. With household debt remaining a systemic risk, the government’s willingness to maintain these tax deductions is a calculated move to prevent a spike in defaults.

According to data from Bloomberg, the correlation between interest rate hikes and consumer spending contraction in Seoul has tightened. When mortgage payments increase, the first casualty is typically discretionary spending. By allowing workers on parental leave to continue accessing tax deductions, the state is effectively subsidizing the cost of borrowing to retain the retail economy afloat.

“The stability of the Korean housing market in 2026 depends less on novel construction and more on the liquidity of the existing homeowner. Tax incentives for families are not just social policy; they are financial stabilizers designed to prevent a deleveraging spiral,” says Dr. Ji-Hoon Kim, a Senior Fellow at the Korea Institute for Public Finance.

The ripple effect extends to the banking sector. Major institutions like KB Financial Group (KRX: 105560) and Shinhan Financial Group (KRX: 055550) must account for these tax-driven repayment capacities when assessing loan risk profiles. A shift in tax law regarding parental leave could, in theory, alter the default probability of a specific segment of the mortgage portfolio.

Comparative Eligibility Framework

To understand the nuances of who can claim these deductions during various employment transitions, consider the following breakdown of NTS standards:

| Employment Status | Worker Status | Deduction Eligibility | Key Constraint |

|---|---|---|---|

| Full-Time Active | Yes | Eligible | Must meet home value limit |

| Parental Leave | Yes | Eligible | Must have earned income in the year |

| Unemployed/Resigned | No | Ineligible | Loss of “Worker” status |

| Freelancer/Business | No | Ineligible | Mortgage deduction is for “Earned Income” |

The Strategic Shift in Family Fiscal Management

The reality is that the “Information Gap” in most tax advice is the failure to mention the opportunity cost of the deduction. For a couple with joint ownership, the decision of who claims the interest deduction should be a dynamic annual calculation based on the projected year-end taxable income of both partners.

If one spouse is on parental leave for a significant portion of the year, their marginal tax bracket drops. In this scenario, the deduction is mathematically more valuable if claimed by the spouse in the higher bracket. However, the National Tax Service (NTS) requires that the person claiming the deduction must be the one who actually paid the interest. This necessitates a clear paper trail of fund transfers from the higher-earning spouse to the loan account, or a structured joint-payment agreement.

This complexity is mirrored in global markets. Just as the Reuters reports on the US Federal Reserve’s impact on mortgage-backed securities, the BOK’s influence on the Korean market is filtered through these domestic tax laws. The intersection of labor policy (parental leave) and fiscal policy (tax deductions) is where the actual economic survival of the middle class is decided.

Looking forward, we expect the Ministry of Economy and Finance to further loosen these restrictions to combat the birth rate decline. We may see a shift where the “worker” requirement is relaxed for parents, allowing the deduction to be claimed regardless of active earned income, provided the loan is serviced. Until then, precision in timing and documentation remains the only way to maximize the tax shield.

For those tracking the broader implications, keep a close eye on the Wall Street Journal‘s coverage of Asian emerging markets, as South Korea’s ability to manage its household debt without triggering a systemic crisis will be a bellwether for the region.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.