Switching from promotional CDs to Treasurys depends on your tax bracket and liquidity needs. Treasurys offer state tax exemptions and secondary market liquidity, whereas CDs lock capital at fixed rates. Evaluate the after-tax yield spread before moving capital in this rate environment.

Tax season injects significant liquidity into the retail banking sector, often funneling refunds into high-yield certificates of deposit. However, the structural efficiency of United States Treasury securities often outweighs the promotional rates offered by commercial banks. For investors holding positions in **JPMorgan Chase (NYSE: JPM)** or **Bank of America (NYSE: BAC)** CDs, the decision matrix requires a strict analysis of after-tax returns and capital accessibility. Here is the math on why government debt might outperform bank deposits.

The Bottom Line

- Treasury interest is exempt from state and local income taxes, potentially increasing net yield by 5% to 10% for high-tax residents.

- CDs impose early withdrawal penalties, whereas Treasurys can be sold on the secondary market without principal forfeiture if held to maturity.

- Current market caution suggests prioritizing liquidity and sovereign credit quality over marginal promotional rate increases.

The Hidden Cost of Promotional Rates

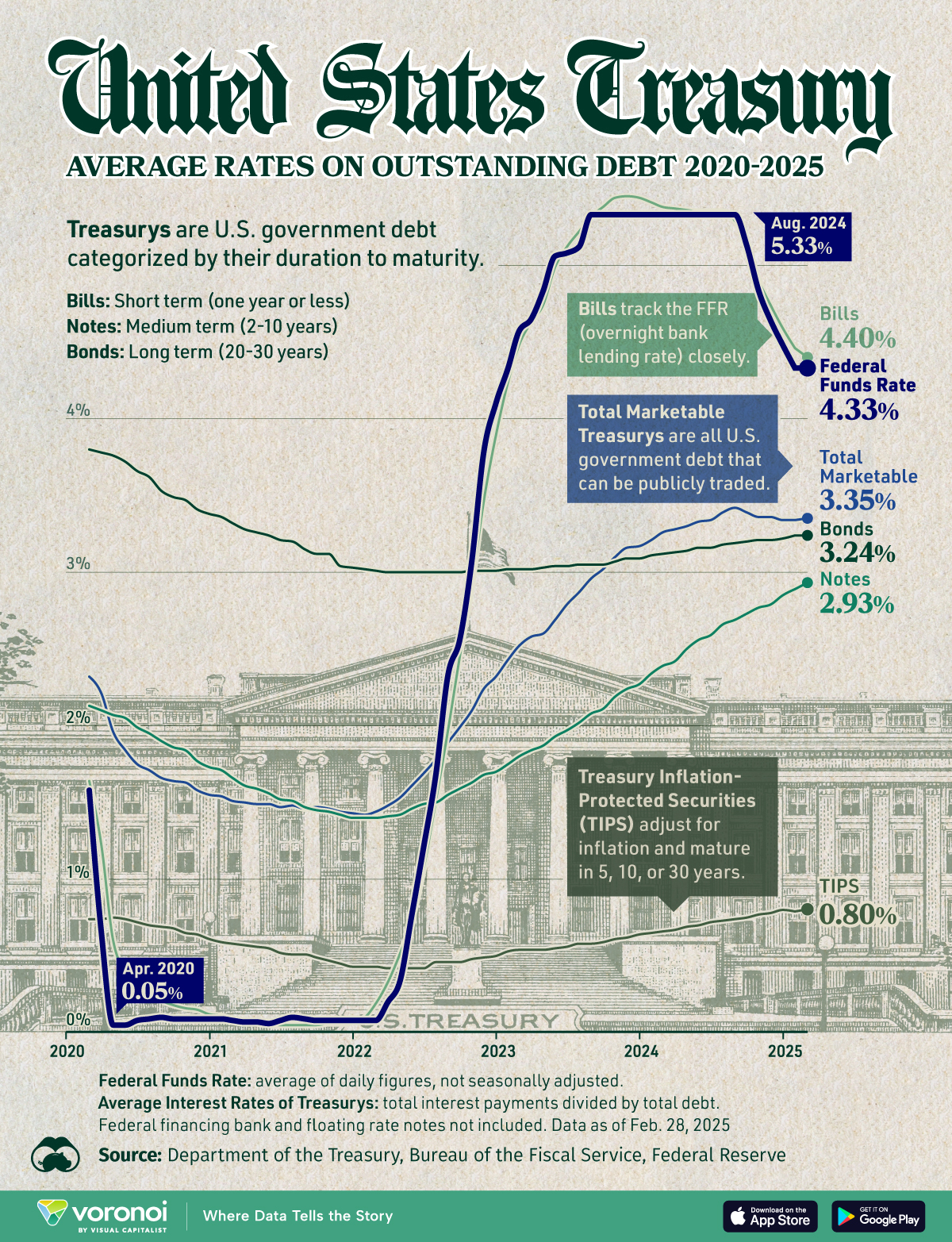

Promotional CDs often advertise headline-grabbing annual percentage yields to attract deposit inflows. Yet, these rates frequently ignore the tax drag imposed by state jurisdictions. When you purchase a certificate of deposit, the interest income is fully taxable at the federal, state, and local levels. In contrast, interest generated from Treasury bills and notes is exempt from state and local income taxes.

But the balance sheet tells a different story when you adjust for jurisdiction. For an investor residing in a high-tax state like California or New York, the state tax exemption alone can bridge the gap between a promotional CD rate and a standard Treasury yield. Consider the effective yield rather than the nominal rate. If a CD offers 5.0% and a Treasury offers 4.8%, the Treasury may provide a higher return on capital after tax obligations are settled.

Market sentiment supports a shift toward sovereign debt during periods of geopolitical uncertainty. Elizabeth Hart, founder of Legacy Wealth Advisors in Singapore, noted that Asian families are becoming more cautious due to the conflict in the Middle East. This risk aversion is not limited to institutional capital. Retail investors should mirror this prudence by reducing exposure to bank credit risk in favor of sovereign guarantees.

“Asian families are becoming more cautious due to the conflict in the Middle East, seeking stability over aggressive yield chasing.” — Elizabeth Hart, Founder, Legacy Wealth Advisors

This caution extends to the banking sector’s stability. While FDIC insurance protects deposits up to limits, the administrative friction of claiming insured funds differs from the liquidity of a Treasury bond. TreasuryDirect provides a direct channel for issuance, removing the intermediary spread that banks capture.

Liquidity Constraints and Penalty Structures

The primary disadvantage of the CD structure is the lock-up period. Accessing capital before the maturity date triggers an early withdrawal penalty, often calculated as months of accrued interest. This penalty effectively reduces the principal investment. Conversely, Treasury notes possess a robust secondary market. You can sell a Treasury position at any time during market hours.

Here is the critical distinction: selling a Treasury before maturity exposes you to interest rate risk, but not penalty risk. If rates rise, the market value of your bond declines. However, if you hold to maturity, the principal is returned in full. With a CD, the penalty applies regardless of market conditions. This flexibility is vital for emergency funds or capital that may be redeployed quickly.

the secondary market for Treasurys is deeper than the market for broken CDs. Institutional investors and primary dealers facilitate liquidity in government debt, ensuring tight bid-ask spreads. Retail banks, however, often impose arbitrary fees or restrictive terms on early withdrawals. Bloomberg Rates & Bonds data consistently shows higher trading volumes in Treasury securities compared to negotiable CDs.

Comparative Analysis of Fixed Income Instruments

To visualize the structural differences, we must appear at the operational mechanics of each instrument. The following table outlines the key variances in tax treatment, liquidity, and credit risk. This comparison assumes a standard investor profile without specific institutional exemptions.

| Feature | Certificate of Deposit (CD) | U.S. Treasury Note/Bill |

|---|---|---|

| Credit Risk | FDIC Insured (up to $250k) | Full Faith and Credit of U.S. |

| State Tax | Taxable | Exempt |

| Liquidity | Penalty for Early Withdrawal | Secondary Market Sale |

| Minimum Investment | Varies by Bank (often $1k) | $100 (TreasuryDirect) |

| Interest Payment | At Maturity or Monthly | Semi-Annual or At Maturity |

The data above highlights the tax inefficiency of CDs for residents in states with income tax. The minimum investment threshold for Treasurys has lowered, making them accessible for tax-refund-sized allocations. The Wall Street Journal frequently reports on the narrowing spread between bank deposit rates and Treasury yields, signaling when the switch becomes advantageous.

Strategic Allocation for Tax Refunds

Deploying a tax refund requires a strategy aligned with your broader portfolio. If your objective is capital preservation with moderate yield, laddering Treasury bills offers a solution. This approach mitigates reinvestment risk. You purchase bonds with staggered maturity dates, ensuring regular liquidity events without exposing the entire portfolio to a single rate decision.

Regulatory bodies like the Securities and Exchange Commission monitor these instruments closely, ensuring transparency in pricing. Bank CDs, while regulated, often bury fee structures in account agreements. The transparency of Treasury auctions provides a clear view of the market-clearing rate. This visibility allows investors to verify they are receiving fair market value.

the decision rests on the net effective yield. Calculate your marginal state tax rate and apply it to the CD interest. Compare that net number to the Treasury yield. If the Treasury offers a comparable or higher net return with superior liquidity, the switch is mathematically sound. Do not let promotional marketing obscure the underlying mechanics of your fixed income allocation.

As we move through the second quarter of 2026, monitor the yield curve for inversion signals. An inverted curve typically favors short-term bills over longer notes. Adjust your duration accordingly. For most retail investors, the simplicity and tax advantages of direct Treasury ownership outweigh the marginal convenience of local bank CDs.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.