Oil prices are rebounding as the blockage of the Strait of Hormuz persists, threatening roughly 20% of global petroleum liquid consumption. Following the steepest price decline since 2020, markets are now pricing in prolonged supply disruptions, sparking volatility in energy equities and raising concerns over global inflationary pressures.

This is not merely a geopolitical skirmish; it is a systemic shock to the global energy supply chain. When the world’s most critical oil chokepoint is compromised, the “risk premium” returns to the foreground of every trading desk from New York to Singapore. For institutional investors, the current volatility represents a violent tug-of-war between recessionary fears and acute supply-side scarcity.

The Bottom Line

- Energy Volatility: Increased crude prices directly inflate operational overhead for logistics-heavy sectors, compressing margins for non-energy industrials.

- Monetary Policy Friction: Sustained energy inflation limits the Federal Reserve’s ability to implement rate cuts, potentially extending the “higher for longer” interest rate environment.

- Strategic Pivot: Upstream producers with non-Middle Eastern assets, such as those in the Permian Basin, gain an immediate competitive valuation advantage.

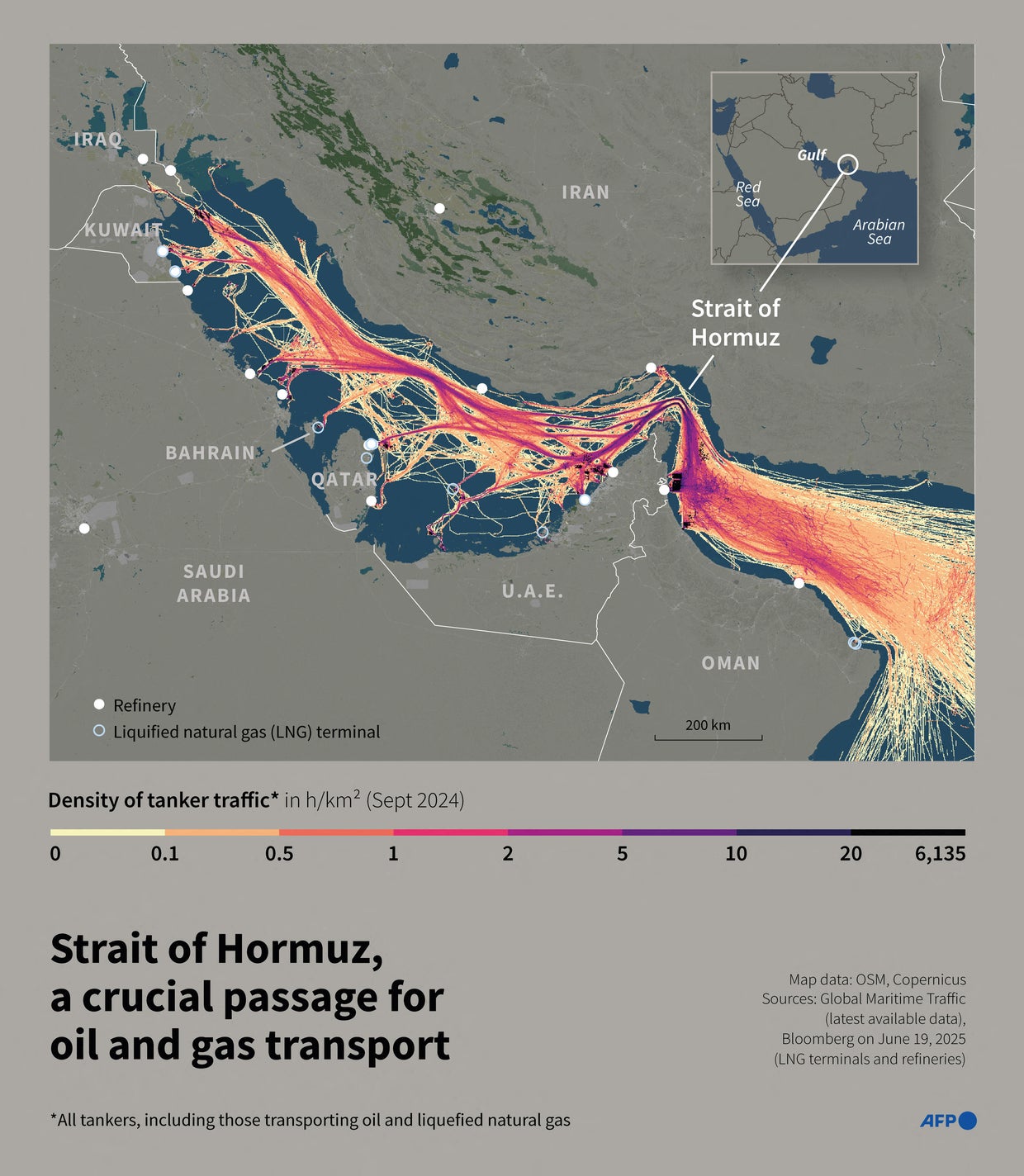

The Geopolitical Risk Premium and Crude Valuations

The initial price drop was a reaction to oversupply fears, but the persistence of the Hormuz blockage has shifted the narrative. We are no longer talking about demand destruction; we are talking about physical unavailability. This shift fundamentally alters the valuation models for energy giants like Exxon Mobil (NYSE: XOM) and Chevron (NYSE: CVX).

Here is the math: When a primary artery for 21 million barrels per day (bpd) is restricted, the market doesn’t just price in the missing barrels. It prices in the uncertainty of when they will return. This creates a floor for Brent crude that resists traditional bearish indicators.

But the balance sheet tells a different story for the midstream sector. While upstream producers benefit from higher spot prices, pipeline and transport firms face logistical nightmares. The cost of rerouting shipments around the Arabian Peninsula adds significant tonnage and time to delivery, increasing the “cost-to-serve” for global refineries.

“The structural fragility of the Strait of Hormuz remains the single greatest point of failure in the global energy architecture. Markets can hedge against price drops, but they cannot hedge against a total lack of physical molecules.” — Senior Energy Strategist, Goldman Sachs

Inflationary Pressure and the Federal Reserve’s Tightrope

The timing of this supply shock is particularly problematic for macroeconomic stability. As we move through April 2026, the global economy has been attempting to stabilize inflation near the 2% target. A sustained spike in energy costs acts as a regressive tax on consumers and a cost-push inflationary trigger for businesses.

If energy prices remain elevated, the Consumer Price Index (CPI) will likely spot a secondary spike. This puts the Federal Reserve in a precarious position. They cannot easily stimulate growth if energy-driven inflation is accelerating. We may see a delay in anticipated rate cuts, which will keep borrowing costs high for little to mid-sized enterprises.

Look at the ripple effect on the automotive sector. Companies like Ford (NYSE: F) and General Motors (NYSE: GM) are already navigating a transition to EVs. A sudden surge in gasoline prices can accelerate EV adoption in the short term, but the increased cost of raw materials—often transported via oil-dependent shipping—could raise the MSRP of the vehicles themselves.

Logistics Bottlenecks and the Shipping Contagion

The blockage does not just affect oil; it affects the entire maritime insurance market. War risk premiums for tankers traversing the region have increased by an estimated 15% to 25% in the last week. This is where the “hidden” cost of the crisis resides.

Shipping conglomerates like A.P. Moller-Maersk (CPH: MAERSK) are forced to recalibrate routes. When tankers are diverted or delayed, it creates a “congestion cascade” at alternative ports. This inefficiency lowers the effective global shipping capacity, driving up freight rates across the board, regardless of whether the cargo is oil or consumer electronics.

To understand the scale of the current volatility compared to the historic 2020 crash, consider the following data:

| Metric | 2020 Market Crash | April 2026 Event |

|---|---|---|

| Primary Driver | Demand Collapse (Pandemic) | Supply Blockage (Geopolitical) |

| Brent Volatility | -70% (Peak to Trough) | +/- 12% (Weekly Swing) |

| Global Supply State | Extreme Oversupply | Structural Deficit |

| Central Bank Stance | Aggressive Easing/Stimulus | Hawkish/Inflation-Wary |

| Shipping Impact | Underutilization | Route Diversion & Congestion |

The Strategic Pivot to Non-OPEC Assets

The persistence of this crisis is accelerating a capital flight toward “safe-haven” energy jurisdictions. We are seeing an increased appetite for assets in the U.S. Shale play and Guyanese offshore fields. The goal is simple: decouple from the volatility of the Persian Gulf.

This shift is not just about oil; it is about energy security. Governments are now treating energy procurement as a national security imperative rather than a procurement exercise. This means long-term contracts are replacing spot-market reliance, which will likely lead to a more fragmented and less efficient global oil market in the long run.

“We are witnessing the finish of the ‘just-in-time’ era for energy. The new mandate is ‘just-in-case,’ and that requires a massive reallocation of capital toward diversified, onshore production.” — Chief Economist, International Energy Agency (IEA)

For the business owner, the takeaway is clear: energy costs are no longer a predictable line item. Hedging strategies that were sufficient in 2024 are now obsolete. Companies must build “energy elasticity” into their pricing models to survive a period of prolonged geopolitical instability.

Moving forward, watch the U.S. Energy Information Administration (EIA) reports for shifts in strategic reserve releases. If the U.S. Decides to flood the market to dampen prices, it may provide temporary relief, but it will not solve the underlying structural risk of the Hormuz chokepoint. For a deeper dive into market pricing, monitor the Bloomberg Terminal data on Brent futures and the Reuters Commodities feed for real-time shipping updates.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.