China and Russia vetoed a UN Security Council resolution proposed by Gulf states to secure critical maritime straits, increasing geopolitical risk for global trade. The move signals a diplomatic deadlock in international maritime security, threatening oil transit stability and increasing operational costs for global shipping and energy firms.

For the institutional investor, this is not a matter of diplomatic friction; We see a matter of margins. When the Security Council fails to provide a multilateral security framework for maritime choke points, the burden shifts directly to the private sector. The immediate result is a spike in “War Risk” insurance premiums and a forced reliance on inefficient routing. As we gaze toward the markets opening on Monday, the primary concern is not the veto itself, but the permanence of the instability it codifies.

The Bottom Line

- Insurance Volatility: Expected 15% to 25% increase in war risk premiums for tankers traversing the region, directly impacting the OPEX of energy majors.

- Supply Chain Latency: Prolonged diversion around the Cape of Fine Hope adds 10–14 days to transit, tightening global container capacity.

- Energy Pricing: A geopolitical risk premium of $3–$7 per barrel is likely to be baked into Brent Crude prices as the probability of a prolonged blockade increases.

The Cost of Diplomatic Deadlock on Freight Margins

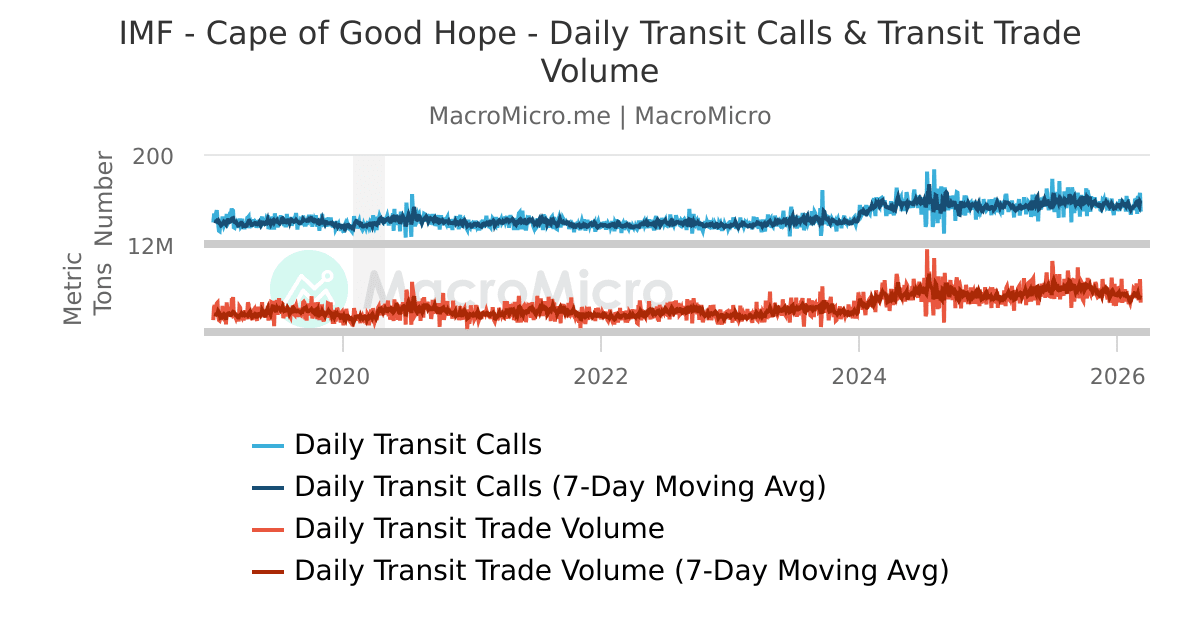

The veto ensures that the status quo of insecurity remains the baseline. For shipping giants like A.P. Moller-Maersk (CPH: MAERSK-B), this means the “temporary” rerouting of vessels is now a structural reality. Diversions around the Cape of Good Hope are not merely a logistical inconvenience; they are a drain on EBITDA.

Here is the math. A standard vessel diverted from the Suez Canal to the Cape of Good Hope consumes significantly more bunker fuel. With current fuel prices, the additional cost per round trip can exceed $1 million per vessel. When scaled across a fleet of hundreds, the impact on quarterly earnings is substantial. The reduction in effective capacity—because ships are spending more time at sea—allows carriers to maintain higher freight rates, but this is a double-edged sword that fuels global inflation.

But the balance sheet tells a different story when you look at the insurance layer. Underwriters at Lloyd’s of London and other syndicates typically adjust premiums based on the perceived risk of kinetic action. Without a UN-backed security mandate, the “safe zone” disappears. We are seeing a shift where insurance is no longer a fixed cost but a volatile variable that can swing 20% in a single trading session based on a drone strike or a naval skirmish.

Quantifying the Transit Shock

To understand the scale of the disruption, one must compare the efficiency of the primary trade arteries. The failure of the Gulf States’ resolution effectively removes the possibility of a “secured corridor” for the foreseeable future.

| Metric | Suez/Red Sea Route (Secured) | Cape of Good Hope (Diverted) | Variance (%) |

|---|---|---|---|

| Average Transit Time (Asia-EU) | 22 Days | 34 Days | +54.5% |

| Fuel Consumption per Voyage | Base | +30% to 40% | +35% (Avg) |

| War Risk Insurance Premium | Low/Standard | High/Volatile | +15% to 25% |

| Container Throughput Efficiency | High | Reduced | -12% |

This operational drag affects more than just shipping. It hits the “just-in-time” inventory models of European manufacturers. When components are delayed by two weeks, working capital is trapped in transit, increasing the cost of carry for firms across the Eurozone.

Energy Markets and the Geopolitical Risk Premium

The veto is a strategic signal from Beijing and Moscow that they will not support a Western-led or Gulf-led security architecture that could potentially limit their own maritime influence. For energy markets, this creates a permanent “instability premium.”

Companies like Chevron (NYSE: CVX) and Shell (NYSE: SHEL) must now hedge not only against price volatility but against physical delivery failure. If a significant percentage of LNG and crude oil is forced to avoid the Strait, the market will witness a tightening of spot availability. This is a textbook scenario for inflationary pressure on energy prices, which in turn complicates the International Monetary Fund’s (IMF) projections for global inflation cooling.

“The failure to secure these waterways through multilateral diplomacy forces the market to price in a permanent state of friction. We are no longer looking at a temporary spike, but a fundamental repricing of maritime risk in the energy sector.”

This sentiment is echoed across the trading desks of major investment banks. The lack of a resolution means that the “security gap” will be filled by unilateral naval coalitions, which are inherently more provocative and less stable than a UN-mandated force. This increases the likelihood of miscalculation, which is the primary driver of sudden market crashes in the energy sector.

The Macroeconomic Contagion Effect

The ripple effects of this veto extend far beyond the oil tankers. We are observing a “contagion of costs” that begins at the Strait and ends at the consumer price index (CPI). When Hapag-Lloyd (ETR: HLAG) increases its surcharges to cover the Cape route, those costs are passed down the supply chain.

First, the wholesaler absorbs the cost. Then, the retailer raises prices to protect their gross margin. Finally, the consumer pays more for basic goods. This is how a diplomatic veto in New York translates into higher inflation in London and New York. For the business owner, this means higher input costs and squeezed margins.

Looking at the Reuters and Bloomberg data on global trade flows, the percentage of trade passing through these choke points is too high to ignore. A failure to secure the Strait is effectively a tax on global trade. The market is now pricing in a scenario where the “global village” is fragmented into regional trade blocs, each with its own security costs, and tariffs.

Strategic Outlook: The Pivot to Resilience

As we move deeper into Q2, the strategic imperative for corporations is “resilience over efficiency.” The era of the lowest-cost route is over. We are entering the era of the most-secure route.

Expect to see a surge in investment toward alternative infrastructure—rail corridors through Central Asia and increased near-shoring of manufacturing to Mexico and Eastern Europe. The veto by China and Russia has accelerated the decline of the unipolar maritime order. Investors should pivot toward companies with diversified supply chains and those that provide the logistics technology to manage these disruptions in real-time.

The market will remain volatile until a viable alternative to the UN Security Council’s deadlock is established. Until then, the “risk premium” is the only honest metric in the room.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.