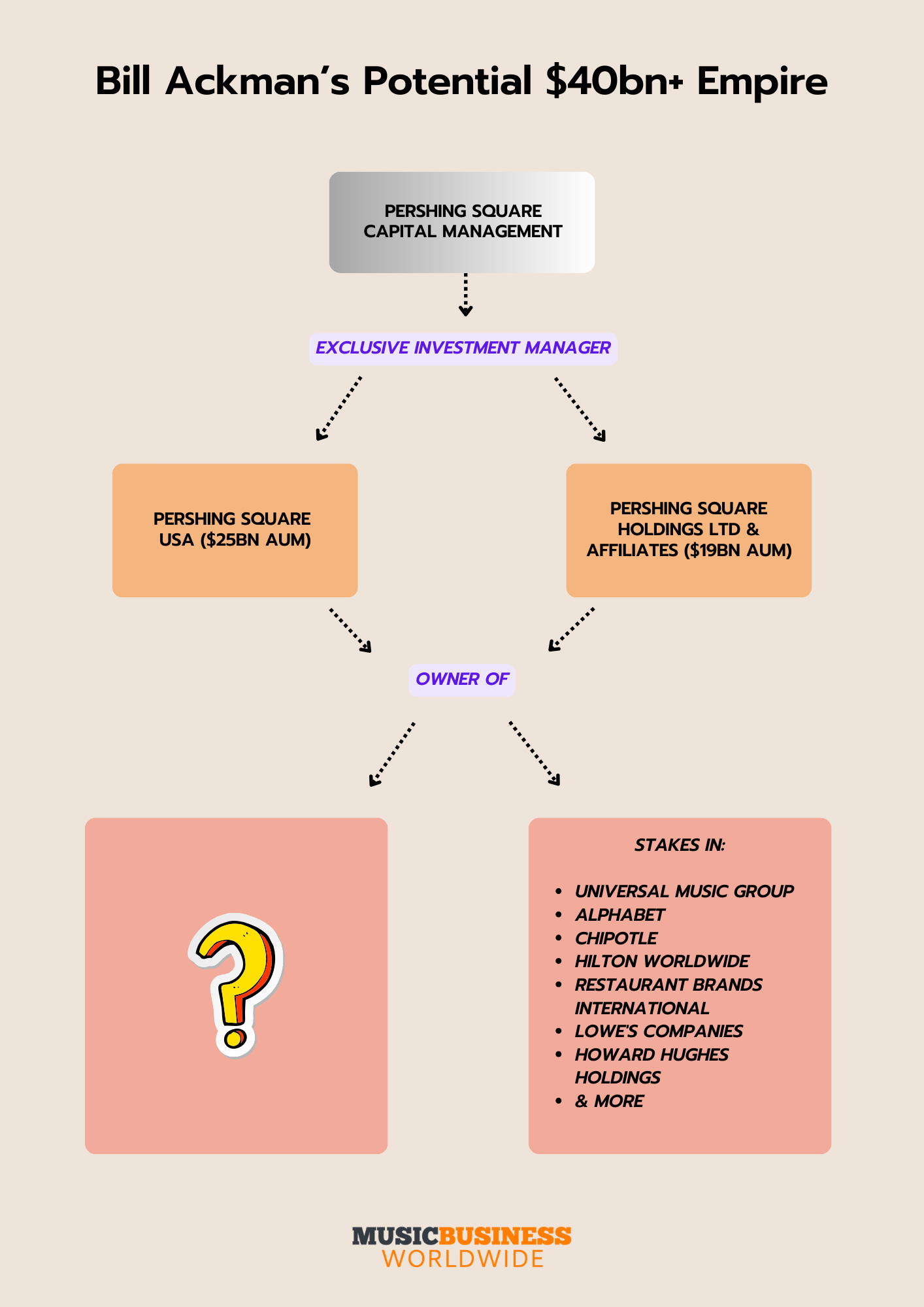

Bill Ackman’s Pershing Square has proposed a €55 billion acquisition of Universal Music Group (UMG), aiming to merge the music giant with its acquisition vehicle and transition the listing to the US. This strategic move signals a massive bet on the financialization of music catalogs and global streaming dominance.

Let’s be clear: this isn’t just another corporate shuffle in the C-suite. When a hedge fund titan like Bill Ackman decides to move on the world’s largest music company, he isn’t looking for the next viral TikTok hit or a chart-topping ballad. He is looking for an annuity. He is treating the sonic wallpaper of our lives—the songs we stream while working, driving and sleeping—as a high-yield asset class akin to prime Manhattan real estate.

The timing is everything. Dropping this news late Tuesday night, Pershing Square is playing a high-stakes game of musical chairs with the global entertainment economy. By proposing a shift from the Euronext Amsterdam to a US listing, Ackman is chasing the “valuation premium” that American markets typically grant to tech-adjacent entertainment powerhouses. But beneath the financial engineering lies a deeper question: what happens to the art when the ownership shifts from a legacy conglomerate to a ruthless activist investor?

The Bottom Line

- The Valuation: A €55 billion offer underscores UMG’s unmatched leverage over streaming platforms and its massive library of “must-have” IP.

- The US Pivot: Moving the listing to the US is a tactical play to unlock higher stock multiples and attract a different breed of institutional investor.

- The Artist Risk: The move could accelerate the “financialization” of music, prioritizing quarterly dividends over long-term artist development.

The Great Migration to Wall Street

For years, UMG has operated under the umbrella of Vivendi, though it has since carved out its own identity. However, Europe’s markets often lack the aggressive appetite for “growth-at-all-costs” that defines the NYSE. By bringing UMG home to the US, Ackman isn’t just changing the ticker symbol; he’s changing the expectations.

Here is the kicker: the US market views music catalogs not as art, but as data streams. In the eyes of Wall Street, a Taylor Swift song isn’t a piece of poetry; it’s a predictable cash flow with a low correlation to the broader stock market. This makes UMG the ultimate hedge against inflation. If the economy dips, people still listen to music.

But the math tells a different story for the artists. While the corporate valuation skyrockets, the “per-stream” payout remains a point of contention. We are seeing a widening gap between the value of the catalog and the compensation of the creator. As Ackman pushes for efficiency, the pressure to squeeze more from global streaming royalties will only intensify.

Beyond the Monthly Subscription

The real play here isn’t actually Spotify or Apple Music. Those are the utilities—the plumbing of the industry. The real gold mine is what analysts call “the super-fan economy.”

The industry is currently pivoting away from the flat $10-a-month subscription model, which has hit a ceiling in developed markets. The new frontier is direct-to-consumer monetization: tiered memberships, digital collectibles, and exclusive “inner circle” access. UMG sits on the most valuable IP in existence, and a US-listed, Pershing Square-backed UMG would be perfectly positioned to weaponize this data.

“The transition of music from a product to a financial asset is nearly complete. We are no longer in the business of selling records; we are in the business of managing intellectual property yields.”

This shift transforms the record label from a talent scout into a portfolio manager. When you look at the relationship between UMG and its rivals like Sony Music and Warner Music Group, the scale of this deal creates a staggering imbalance of power. UMG doesn’t just negotiate with streaming platforms; it dictates terms to them.

The Power Dynamics of the Big Three

To understand the scale of this €55 billion gamble, you have to look at the landscape. UMG isn’t just a leader; it’s a hegemon. While Sony has a strong grip on publishing and Warner maintains a lean, aggressive posture, UMG owns the cultural zeitgeist.

| Company | Primary Strength | Market Position | Strategic Focus (2026) |

|---|---|---|---|

| Universal Music Group | Massive Catalog/Global Reach | Market Leader | Super-fan Monetization |

| Sony Music | Publishing/Synergy with Gaming | Strong Challenger | Cross-Media Integration |

| Warner Music Group | Agile Digital Strategy | Niche Powerhouse | Independent Distribution |

But here is where it gets messy. The music industry is currently grappling with the AI revolution. The tension between generative AI and copyright law is the defining battle of the decade. By acquiring UMG, Ackman isn’t just buying songs; he’s buying the legal standing to sue every AI company that trains its models on UMG’s artists without a license.

The move effectively turns UMG into a “copyright fortress.” In a world where AI can mimic any voice, the only thing with actual value is the verified, legal ownership of the original recording. What we have is the “moat” that Pershing Square is actually buying.

The Creative Collision Course

Now, let’s talk about the human element. Music is an emotional product, but hedge funds are cold. There is an inherent friction between the “artist-first” rhetoric of labels and the “shareholder-first” mandate of an activist investor.

We’ve already seen the trend of artists like Bruce Springsteen and Bob Dylan selling their catalogs for hundreds of millions. It’s a retirement plan for the legends, but for the rising stars, it creates a system where the label owns the future of their creativity before they’ve even hit their prime. If Ackman implements a “lean” operational model, we may witness a shift toward shorter-term, more aggressive contracts that favor immediate ROI over long-term artist development.

As reported by Variety and Deadline, the industry is already seeing a rise in “independent” movements where artists bypass labels entirely. A Pershing Square takeover could either accelerate this exodus or, conversely, create a UMG so powerful that it becomes the only viable path to global stardom.

“The risk is that music becomes too ‘optimized.’ When you manage a catalog like a stock portfolio, you stop taking risks on the weird, the avant-garde, and the slow-burn artists who don’t fit a spreadsheet.”

The bottom line? Bill Ackman is betting that the world will never stop humming along to the hits. He’s betting that the copyright of a song is the safest bet in the world. He might be right about the money, but the cultural cost is yet to be tallied.

So, I aim for to hear from you: Does it bother you that your favorite artists are becoming “assets” in a hedge fund’s portfolio, or is this just the natural evolution of the digital age? Let’s get into it in the comments.