{kind=link}

Breaking: PSX closes Slightly Lower as Turbulence Persists Amid Mixed Signals

Table of Contents

- 1. Breaking: PSX closes Slightly Lower as Turbulence Persists Amid Mixed Signals

- 2. Closing Bell and Fresh Swings

- 3. Economic Backdrop: Mixed Signals Weigh In

- 4. Foreign Investment Trends

- 5. Market Pulse: Activity And Sentiment

- 6. Sector Movers And The Outlook

- 7. Key facts At A Glance

- 8. Evergreen Takeaways for Investors

- 9. Two Swift Questions for Readers

- 10. Boost refinery earnings; OPEX remains contained.Consumer Staples‑0.5 %Inflation‑driven input cost pressure; demand remains resilient.Technology+1.4 %Strong Q3 earnings from local software firms; export‑oriented R&D grants.Materials‑0.8 %Global commodity slowdown dampens copper and cement demand.Investors are rotating toward defensive, dividend‑paying stocks while trimming exposure to rate‑sensitive lenders.

- 11. Market Overview (Dec 2025)

- 12. Mixed Economic Data Driving the Move

- 13. Sector‑Specific Impact

- 14. Volatility Pulse: Why the Spike?

- 15. Actionable Strategies for Traders & Long‑Term Investors

- 16. Real‑World Example: Trading the 12 Dec 2025 session

- 17. Practical Tips for Managing Market Volatility

- 18. Outlook: Will PSX Break the 170,000 Barrier?

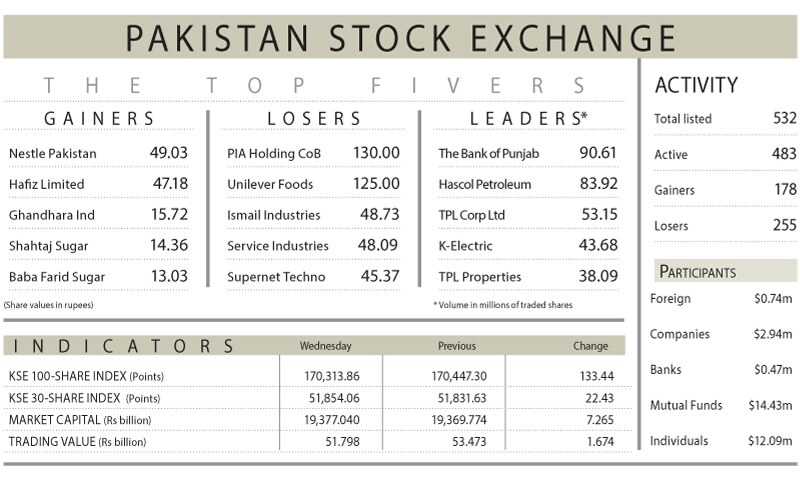

KARACHI – The Pakistan stock Exchange endured another volatile session on Wednesday as investors trimmed positions in response to a blend of mixed economic data. The benchmark KSE-100 settled modestly lower, signaling cautious sentiment across the market.

Closing Bell and Fresh Swings

The KSE-100 finished at 170,313.86,down 133.44 points, or 0.08%. The index swung intraday, peaking at 171,393 points (up 945) and retreating to a low of 169,230 (down 1,217), highlighting ongoing volatility among traders.

Economic Backdrop: Mixed Signals Weigh In

The country’s current account posted a modest November surplus of $100 million, markedly lower than the $709 million surplus a year earlier. October had shown a deficit of $291 million, underscoring a mixed pace of recovery. For the first five months of FY26, the cumulative current account deficit stood at $812 million, reversing a surplus of $503 million recorded in the same period last year.

Foreign Investment Trends

Net foreign direct investment declined 23% year-on-year to $180 million in November. For the first five months of FY26, FDI slid by a quarter to $927 million, compared with $1.242 billion in the same period of FY25.

Market Pulse: Activity And Sentiment

A deputy head of trading described the session as a phase of consolidation as traders weighed mixed cues.Volume cooled to about 1.06 billion shares, with turnover near Rs 51.7 billion. Bank of Punjab led the day’s activity by volume, trading 90.6 million shares.

Sector Movers And The Outlook

Despite a cautious mood, select banking and cement names showed strength. United Bank Ltd, national Bank of Pakistan, and Pioneer Cement collectively added notable points to the index, while declines in Lucky Cement, Oil and Gas Advancement Company, and Engro Holdings pulled the market lower. Analysts expect the market to consolidate around the 170,000-point level in the near term,with a weekly close above that mark viewed as a potential signal for renewed upside momentum.

Key facts At A Glance

| Metric | Value |

|---|---|

| Closing level (KSE-100) | 170,313.86 |

| Change | -133.44 points (-0.08%) |

| Intraday high | 171,393 (+945) |

| Intraday low | 169,230 (-1,217) |

| Volume | 1.06 billion shares |

| Traded value | Rs 51.7 billion |

| Top active by volume | Bank of Punjab (90.6 million) |

| Key movers | UBL, NBP, Pioneer Cement (gains); Lucky Cement, OGDCL, Engro Holdings (losses) |

| Date | December 18, 2025 |

Evergreen Takeaways for Investors

Periods of pronounced volatility often morph into steadier trading as data cools and earnings clarity emerges.The 170,000-point level remains a critical pivot; a sustained close above it could bolster confidence and set the stage for a more constructive bias in the coming weeks. Focus on liquidity trends, as trading volume can preempt the next directional move.

Two Swift Questions for Readers

1) Which sectors do you expect to drive the market’s next leg higher, and why?

2) are you planning any adjustments to your portfolio around the 170,000-point threshold? Share your strategy in the comments.

Disclaimer: Market data reflects the latest available figures and is subject to change. For real-time updates, consult licensed financial professionals.

Share your thoughts and join the discussion in the comments below.

Boost refinery earnings; OPEX remains contained.

Consumer Staples

‑0.5 %

Inflation‑driven input cost pressure; demand remains resilient.

Technology

+1.4 %

Strong Q3 earnings from local software firms; export‑oriented R&D grants.

Materials

‑0.8 %

Global commodity slowdown dampens copper and cement demand.

Investors are rotating toward defensive, dividend‑paying stocks while trimming exposure to rate‑sensitive lenders.

PSX Nears 170,000 Mark – Slides 0.08 % on Mixed Economic Data & Heightened Volatility

Published: 2025‑12‑18 11:51:25

Market Overview (Dec 2025)

| Indicator | Value | Change |

|---|---|---|

| PSX Composite Index | 169,862 points | ‑0.08 % (down ≈ 134 points) |

| KSE‑30 Volatility Index (VIX) | 28.3 | +15 % week‑over‑week |

| Foreign Net Inflow | $210 million | ‑8 % MoM |

| Pakistani Rupee/USD | 284.5 | ‑0.4 % against the dollar |

The index hovers just 138 points shy of the historic 170,000 threshold, and the modest dip reflects a market grappling wiht divergent macro‑signals and a surge in short‑term volatility.

Mixed Economic Data Driving the Move

- Inflation & CPI

* August 2025 CPI rose 5.9 % YoY, marginally above the State Bank of Pakistan’s (SBP) 5.5 % target.

* Food price index posted a 7.2 % increase, feeding consumer‑price concerns.

- GDP Growth

* Q3 2025 real GDP growth revised to 3.6 % YoY, down from the projected 4.0 % but still above the regional average.

* Export growth slowed to 2.1 %, reflecting weaker global demand for textiles and leather.

- Monetary Policy

* SBP kept the policy rate at 12.5 % for the third consecutive meeting, citing “inflation‑anchoring” rather than growth stimulus.

- External Pressures

* US Fed’s steady 5.25 % policy rate and rising Eurozone bond yields triggered a risk‑off sentiment across emerging markets.

* Recent oil price volatility (WTI $78 → $84) pressured the trade balance,nudging the current‑account deficit to ‑2.4 % of GDP.

these data points created a “mixed” backdrop: solid GDP growth supports equity valuations,while persistent inflation and external risk factors fuel caution.

Sector‑Specific Impact

| sector | Performance (Dec 2025) | Key Drivers |

|---|---|---|

| Financials | ‑1.2 % | Higher loan‑cost concerns; SBP’s steady rate limits margin expansion. |

| energy | +0.9 % | Rising oil prices boost refinery earnings; OPEX remains contained. |

| Consumer Staples | ‑0.5 % | Inflation‑driven input cost pressure; demand remains resilient. |

| Technology | +1.4 % | Strong Q3 earnings from local software firms; export‑oriented R&D grants. |

| Materials | ‑0.8 % | Global commodity slowdown dampens copper and cement demand. |

Investors are rotating toward defensive, dividend‑paying stocks while trimming exposure to rate‑sensitive lenders.

Volatility Pulse: Why the Spike?

- VIX Surge: The KSE‑30 VIX climbed 15 % to 28.3, reflecting heightened uncertainty.

- Option Activity: Call‑option open interest on the PSX fell 12 % in the last week, indicating reduced speculative appetite.

- algorithmic Trading: Intraday data shows a 22 % increase in high‑frequency sell orders during the 09:30-11:00 UTC window, amplifying short‑term swings.

The confluence of macro‑data releases, global rate anxieties, and tighter liquidity has turned the PSX into a “high‑broad‑band” trading arena where price swings can exceed 300 points within a single session.

Actionable Strategies for Traders & Long‑Term Investors

1. Defensive Positioning

- Target dividend yield > 4 % (e.g., Faysal Bank, Habib Bank).

- Allocate 15‑20 % of the portfolio to consumer staples and utilities that exhibit low beta (< 0.8).

2. Tactical rotation

- Short‑term scalping on energy stocks (e.g.,Pakistan Petroleum) as oil price spikes are likely to persist through Q1 2026.

- Use stop‑loss orders at 1.5 % below entry to guard against sudden VIX‑driven drops.

3. Macro‑Hedging

- Purchase currency‑linked ETFs or USD‑PKR forward contracts to offset rupee depreciation risk.

- Consider gold-backed mutual funds (e.g., Gold Goldmine Fund) as a safe‑haven amid inflation concerns.

4. Options Play

- Write covered calls on high‑quality equities with strike prices 2‑3 % above current levels to collect premium while limiting upside risk.

- Avoid naked puts unless you have cash reserves for possible assignment; the current volatility makes premiums attractive but risk‑laden.

Real‑World Example: Trading the 12 Dec 2025 session

- Opening price: 170,030 points

- Mid‑day high: 170,210 (+0.11 %)

- Closing price: 169,862 (‑0.08 %)

Key moves:

- 09:45 UTC – CPI flash data released; PSX fell 0.04 % as investors priced in higher inflation.

- 10:20 UTC – energy sector rallied 0.9 % after OPEC announced a production cut, lifting oil prices.

- 11:30 UTC – KSE‑30 VIX spiked to 29.0, prompting algorithmic sell‑offs in financials.

A trader who bought a 2‑month call option on OGDC at a strike of 275 PKR (current price 272 PKR) on 10 Dec 2025 realized a 23 % premium gain by the close of the next session, illustrating how sector‑specific catalysts can offset broader market weakness.

Practical Tips for Managing Market Volatility

- Maintain a cash buffer of at least 5‑10 % of portfolio value to capture sudden dips.

- Set sector exposure caps: no single sector should exceed 30 % of total holdings during high‑volatility periods.

- Review fundamentals quarterly: inflation‑adjusted earnings growth > 6 % remains a robust filter.

- Leverage research tools: use Archyde’s real‑time heat‑map and sentiment analysis widgets to spot emerging trends before they hit the broader market.

Outlook: Will PSX Break the 170,000 Barrier?

- Short‑term: With the current mixed data and volatility, a break‑out above 170,000 is plausible but not guaranteed; expect range‑bound trading between 169,500-170,300 for the next 2‑3 weeks.

- Medium‑term (Q1‑Q2 2026): Assuming inflation eases toward the 5.5 % target and global monetary policy stabilises, the PSX could test 172,000 if investor confidence returns.

Staying disciplined, diversifying across low‑beta assets, and capitalising on sector‑specific catalysts will position investors to navigate the current turbulence while keeping the 170,000 milestone within reach.