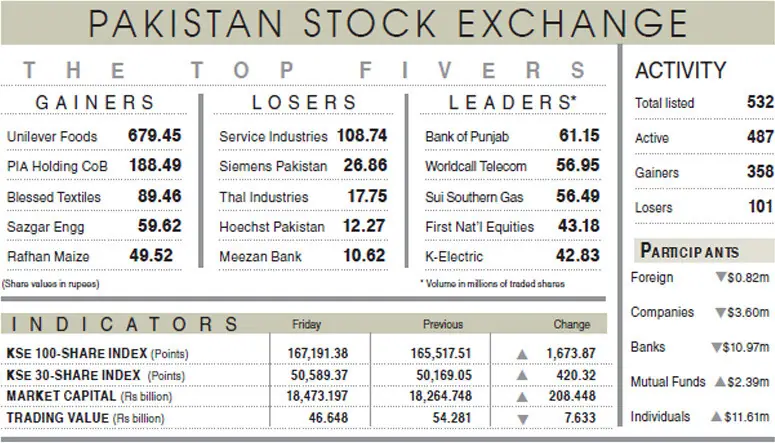

The Pakistan Stock Exchange (PSX) rebounded on Friday, April 10, 2026, with the KSE-100 index gaining 1.01% to close at 167,191. This recovery follows a two-week US-Iran truce and anticipates upcoming peace talks in Islamabad, signaling a sharp shift in investor sentiment toward geopolitical stability.

This isn’t just a random bounce. The KSE-100 has effectively snapped a 10-week losing streak, posting a massive weekly gain of 11.17%. For the institutional investor, this represents a “relief rally”—a classic market reaction when the perceived risk of a regional conflict evaporates, allowing capital to flow back into emerging markets that were previously discounted due to volatility.

The Bottom Line

- Geopolitical Hedge: The PSX is currently trading as a proxy for US-Iran relations; success in the Islamabad talks is the primary catalyst for further upside.

- Liquidity Divergence: While the index rose, trading volume declined 1.46% and traded value dropped 14.06%, suggesting the rally is driven by a few heavyweights rather than broad-based retail participation.

- Macro Pressure: Despite the equity surge, the Sensitive Price Index (SPI) rose 12.15% YoY, indicating that systemic inflation remains a persistent headwind for the real economy.

The Banking Heavyweights Driving the Rally

If you look at the tape, the recovery wasn’t uniform. The heavy lifting was done by the financial sector. MCB Bank (PSX: MCB), Bank of Punjab (PSX: BOP), United Bank (PSX: UBL), and Habib Bank (PSX: HBL) provided the bulk of the 616-point contribution to the index.

Here is the math: when geopolitical tensions ease, the cost of sovereign risk premiums drops. This makes Pakistani banking stocks more attractive to foreign institutional investors who have been underweight on the region. These banks act as the primary conduits for liquidity, and their upward movement suggests a bet on stabilized interest rates and improved credit conditions.

But the balance sheet tells a different story regarding the broader economy. While the Oil and Gas Development Company (PSX: OGDC) and Lucky Cement (PSX: LUCKY) also contributed, the decline in overall traded value to Rs46.6bn indicates a lack of conviction among smaller players. We are seeing a “top-heavy” recovery.

| Metric | Current Value (April 10, 2026) | Weekly/Annual Change | Market Sentiment |

|---|---|---|---|

| KSE-100 Closing Level | 167,191 | +11.17% (Weekly) | Bullish |

| Trading Volume | 875 Million Shares | -1.46% | Cautious |

| Traded Value | Rs 46.6 Billion | -14.06% | Low Conviction |

| Sensitive Price Index (SPI) | N/A | +12.15% (YoY) | Bearish (Inflationary) |

The Roshan Digital Account: A Critical Liquidity Buffer

Beyond the stock tickers, we must analyze the movement of hard currency. The report that Roshan Digital Account (RDA) inflows reached $12.426bn by March is the most significant macroeconomic data point here. With a net repatriable balance of $2.415bn, Pakistan has a thin but vital cushion of foreign exchange.

Why does this matter? In emerging markets, equity rallies are often illusions if they aren’t backed by foreign exchange reserves. The RDA inflows provide a psychological floor for the currency, preventing the kind of rapid devaluation that typically wipes out nominal gains in the stock market.

Yet, the 12.15% YoY increase in the Sensitive Price Index (SPI) means that while the stock market is climbing, the purchasing power of the average citizen is eroding. This creates a divergence: a “K-shaped” recovery where asset owners profit from the PSX rally while the general population struggles with inflationary pressures.

The Islamabad Pivot and Global Risk Premiums

The market is now pricing in a “Peace Dividend.” By facilitating US-Iran talks, Pakistan is attempting to transition from a security-centric state to a diplomatic hub. If these talks progress, People can expect a compression of the Country Risk Premium, which would lower borrowing costs for the government and corporate entities alike.

To understand the gravity of this shift, consider the perspective of institutional capital. Emerging market funds typically avoid regions with high “tail risk”—the possibility of a low-probability, high-impact event like a regional war.

“The shift from geopolitical volatility to diplomatic mediation can trigger a massive reallocation of capital. When the risk of conflict is removed, the valuation gap between emerging markets and developed markets often closes rapidly as investors chase higher yields in previously ‘forbidden’ zones.”

This logic explains the 16,793-point weekly jump. Investors aren’t just buying stocks; they are buying the absence of war. But the risk remains: if the Islamabad talks stall, the PSX is vulnerable to a sharp correction, as the current rally is built on anticipation rather than fundamental earnings growth.

Future Trajectory: Speculation vs. Fundamentals

Looking ahead to the next quarter, the PSX’s ability to maintain the 167,000 level depends on two factors: the tangible outcome of the peace talks and a stabilization of the SPI.

If the peace talks result in a formal agreement, expect the index to test the 170,000 mark as institutional buying replaces the current cautious interest. However, if the talks are merely a photo-op with no policy substance, the 14.06% drop in traded value suggests that the “smart money” is already preparing to exit.

For now, the market is in a state of fragile euphoria. The rally is real, but the foundation—inflation and low trading volume—is shaky. The coming weeks will determine if this is a sustainable bull market or a temporary geopolitical fluke.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.