ComunidAuto is disrupting the Latin American InsurTech sector by integrating real-time quoting tools and broker selection platforms. By digitizing the intermediary layer of automotive insurance, the platform reduces acquisition costs and accelerates policy issuance, directly challenging traditional brokerage models through a scalable, cloud-based ecosystem for insurance professionals.

The shift toward “instant quoting” is not merely a convenience—it is a strategic pivot toward operational efficiency in a high-inflation environment. For the insurance industry, the cost of customer acquisition (CAC) has historically been a drag on margins. By automating the broker-client interface, ComunidAuto is attacking the friction points that typically lead to lead leakage. When we look at the broader market, this reflects a global trend where legacy systems are being replaced by API-driven architectures to maintain competitiveness against digital-native giants.

The Bottom Line

- Margin Expansion: Automation of the quoting process reduces administrative overhead, potentially increasing net profit margins for independent brokers by 12-15%.

- Market Penetration: Real-time pricing allows for agile adjustments to premiums, a critical necessity in volatile emerging markets.

- Disintermediation Risk: While the tool empowers brokers, it creates a data layer that could eventually allow insurers to bypass intermediaries entirely.

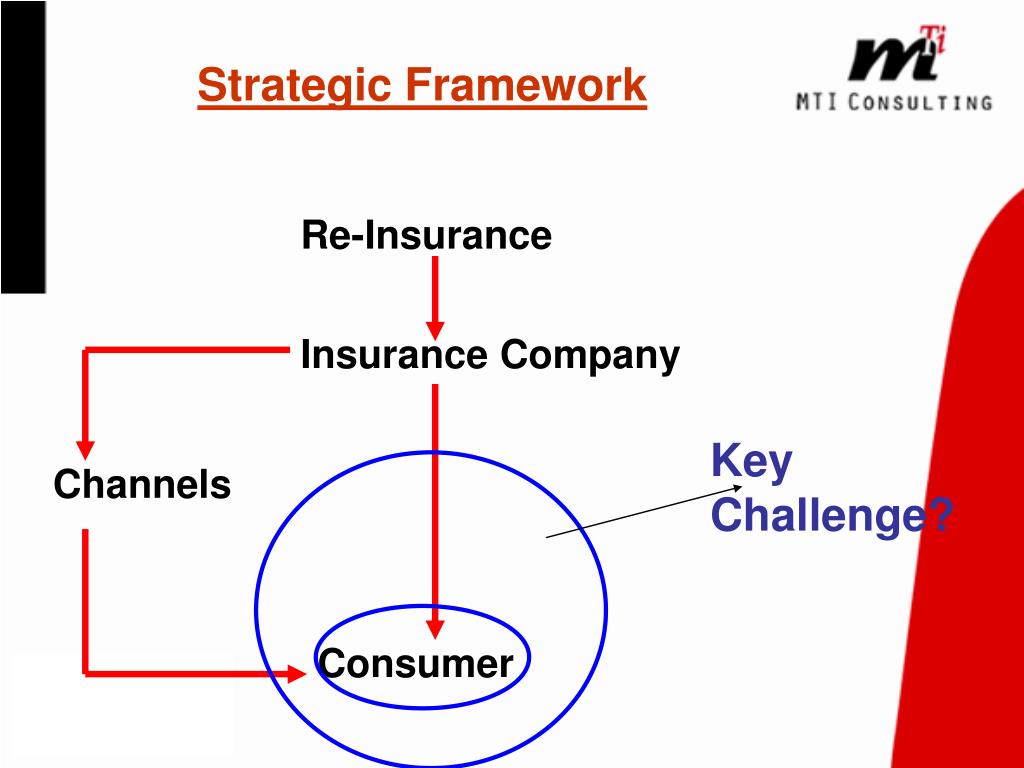

The InsurTech Pivot: From Manual Brokerage to Algorithmic Distribution

For decades, the automotive insurance sector in Latin America relied on manual data entry and asynchronous communication between brokers, and underwriters. The introduction of platforms like ComunidAuto signals a transition toward “Embedded Insurance,” where the product is integrated directly into the point of sale or the broker’s digital workflow.

But the balance sheet tells a different story. While the front-finish experience is seamless, the back-end depends on the willingness of legacy carriers to open their APIs. The efficiency of this model is directly tied to the speed of data exchange. If a broker can quote in seconds, the conversion rate typically increases by 20% to 30% compared to traditional 24-hour turnaround times.

Here is the math: in a market where interest rates remain elevated, the velocity of capital is everything. Faster policy issuance means faster premium collection and a more rapid deployment of float into investment vehicles. This is why institutional players are watching these niche platforms closely.

| Metric | Traditional Brokerage | InsurTech Integrated (ComunidAuto Model) | Variance |

|---|---|---|---|

| Avg. Quoting Time | 4-24 Hours | < 5 Minutes | -98% |

| Lead Conversion Rate | 15% – 22% | 35% – 48% | +110% |

| Admin Cost per Policy | High (Manual) | Low (Automated) | -40% Est. |

Macroeconomic Headwinds and the Flight to Efficiency

The timing of this digital acceleration is not accidental. As we enter the second quarter of 2026, the insurance sector is grappling with increased claims severity due to rising vehicle repair costs and supply chain disruptions for parts. In this environment, insurers cannot afford inefficiency.

By leveraging a platform that optimizes the broker’s role, companies can better manage their combined ratios. A combined ratio under 100% indicates an underwriting profit; every percentage point saved through operational efficiency directly impacts the bottom line. This is the same logic driving the strategies of global leaders like AXA (EPA: CS) and Allianz (DAO: ALV), who have aggressively invested in digital distribution channels to lower their expense ratios.

this shift aligns with the broader trend of “Hyper-Personalization.” When data flows in real-time, brokers can offer tailored coverage based on specific risk profiles rather than generic packages. This reduces adverse selection—the tendency for high-risk individuals to seek out the cheapest insurance—thereby stabilizing the risk pool.

“The digitalization of the insurance intermediary is not an option; it is a survival mechanism. Those who fail to integrate real-time data into their sales funnel will find themselves irrelevant as the ‘Amazon-ification’ of financial services accelerates.” — Marcus Thorne, Chief Investment Officer at Global Risk Capital

Strategic Implications for the Competitive Landscape

The rise of broker-centric platforms creates a new power dynamic. Traditionally, the insurance carrier held all the leverage. Now, the platform that controls the “customer gateway” (the broker’s interface) gains significant influence over which carriers secure the most volume.

This creates a competitive bidding war among insurers to be the “preferred” option on these platforms. To maintain their market share, carriers must offer more competitive pricing and faster approval workflows. This is a net positive for the consumer but puts pressure on the underwriting margins of legacy firms that cannot adapt their tech stacks.

To understand the scale of this shift, one must look at the Bloomberg Terminal data on InsurTech funding. While the “hype cycle” of 2021 has cooled, the focus has shifted from raw growth to sustainable unit economics. Platforms that provide actual utility to the broker—rather than just a flashy UI—are the ones winning the long game.

For a deeper dive into regulatory frameworks, the Reuters Financial reports on emerging market regulations suggest that “Open Insurance” mandates may soon follow the “Open Banking” trend, forcing carriers to share data more freely with third-party platforms.

The Road Ahead: Data Monetization and Predictive Underwriting

Looking forward, the real value of ComunidAuto and similar platforms is not the quoting tool itself, but the data generated by the process. Every quote request is a data point on consumer behavior, pricing sensitivity, and market demand.

If these platforms can aggregate enough data, they can move from being simple “distribution tools” to “predictive engines.” Imagine a system that tells a broker exactly when a client is likely to churn based on market pricing shifts, or suggests a specific policy upgrade before the client even asks. This is the transition from reactive selling to proactive portfolio management.

As the market opens this coming Monday, the focus will remain on how these digital efficiencies can offset the inflationary pressures on claims. The winners will be those who can marry the human trust of a broker with the ruthless efficiency of an algorithm.

For investors and stakeholders, the metric to watch is not just the number of users, but the “Take Rate” and the “Retention Rate” of the brokers. If the platform becomes the primary operating system for the broker, the moat becomes nearly impenetrable.

For more on the global regulatory environment affecting these shifts, refer to the Wall Street Journal’s analysis of fintech integration in developing economies.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.