{kind=link}

Table of Contents

- 1. Breaking: mendoza Health Authority Tightens Semaglutide Coverage for Diabetes and obesity Treatments

- 2. The coverage shift for semaglutide

- 3. What are metformin and semaglutide?

- 4. Key facts at a glance

- 5. Why this matters

- 6. What readers should know

- 7. Ethical and health considerations

- 8. Helpful context and resources

- 9. Engagement questions

- 10. Citing FDA label and clinical trial outcomes (e.g., STEP 1‑5 studies).

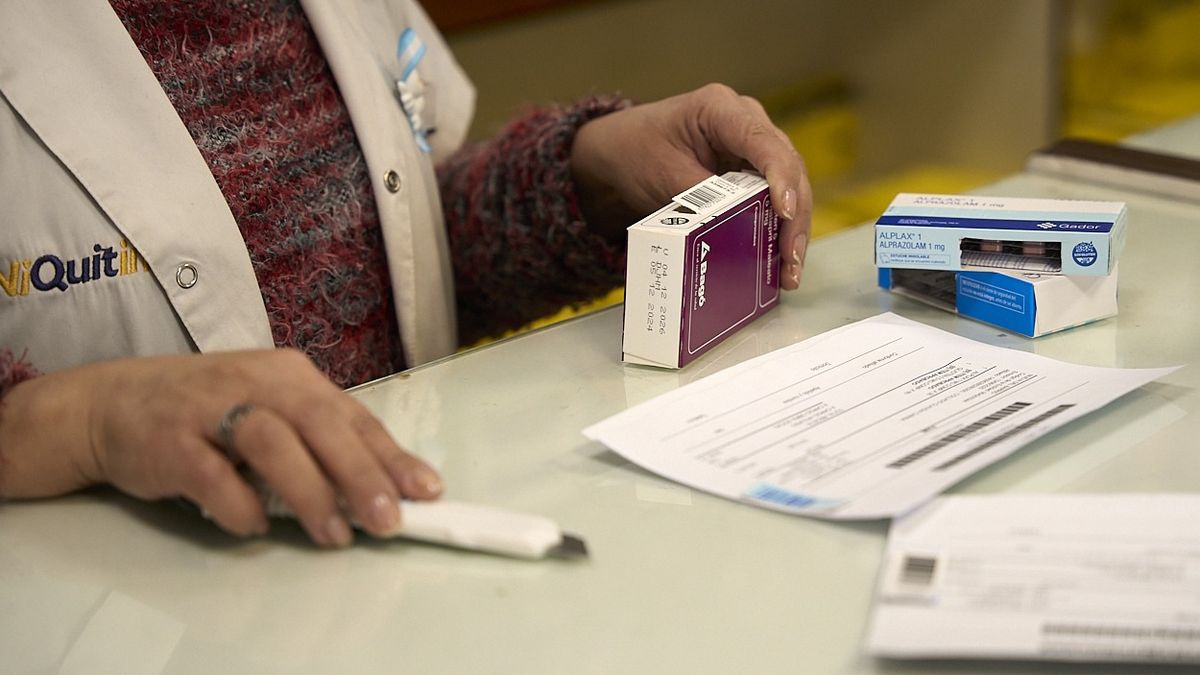

In Mendoza, regional health authorities have clarified how semaglutide is covered by social works and private insurers, signaling new limits on access unless medical indications are met. The move comes amid growing use of the drug for weight management, beyond its original diabetes indication.

the head of the Social Work for Public Employees (OSEP) said coverage depends on clear medical justification and adherence to treatment protocols. While many medications carry a fixed partial coverage, semaglutide’s insurance treatment now hinges on the underlying condition it is meant to treat and the patient’s overall management plan.

The coverage shift for semaglutide

OSEP notes that historically,social and prepaid funds often capped drug coverage at around 40%. When semaglutide is well indicated for a metabolic disorder—such as type 2 diabetes alongside obesity—the drug may be covered at a higher level, with a minimum threshold described as 70% in chronic-treatment scenarios.

For the lowest-dose formulation approved for obesity, insurers may apply the same 70% coverage if the clinical indication is appropriate.In practice, coverage depends on the pathology and the audit results of the patient’s condition.

Conversely, if authorities determine that there has been indiscriminate use of semaglutide—for example, a patient who did not follow prescribed diet or did not start with the recommended first-line therapy—the coverage can be suspended or reduced. In such cases,insurers may require starting with the appropriate treatment first (such as metformin) before reconsidering semaglutide.

A physician can request an exception evaluation to have a specific case reviewed in the medical audit. This process allows clinicians to justify direct semaglutide use when there is a compelling clinical reason to bypass a standard sequence.

What are metformin and semaglutide?

Metformin is an oral prescription medication used with diet and exercise to treat type 2 diabetes by lowering blood glucose. It can reduce glucose levels, improve hemoglobin A1C, and assist with weight loss when combined with lifestyle changes.

Semaglutide is a GLP-1 receptor agonist that targets multiple pathways: it lowers blood sugar by boosting insulin release and, in the brain, curbs appetite, helping patients feel full. It began as an injectable therapy and later gained a pill form for weight management,along with its diabetes indication.

Key facts at a glance

| Aspect | Details |

|---|---|

| Primary coverage rule | Well-indicated semaglutide may receive higher coverage (up to 70%) for chronic conditions. |

| Conditions considered | Diabetes with metabolic disorder; obesity with clinical justification. |

| Low-dose obesity indication | May qualify for 70% coverage if clinically justified. |

| Limitations | Indiscriminate use or failure to follow recommended steps may reduce or suspend coverage. |

| Exceptions process | Physicians can request an exception evaluation for individual cases. |

Why this matters

Experts say the new guidelines aim to balance patient access with responsible prescribing. Semaglutide remains a powerful tool for managing metabolic disease and obesity, but proper medical indication and adherence to standardized treatment sequences are now more explicitly tied to insurance coverage decisions.

What readers should know

Patients facing coverage decisions should discuss candidly with their clinicians and insurers, and keep detailed medical records showing indications, treatment steps, and response to therapy.

Ethical and health considerations

Experts emphasize that access to prescribed medications is one piece of a broader chronic-disease management plan. Patients should pair pharmacotherapy with diet, physical activity, and regular medical follow-up.This article provides general information and should not replace medical advice from a clinician.

Helpful context and resources

For further reading on semaglutide’s uses and regulatory status, see authoritative health sources such as the U.S.Food and Drug Governance and major medical organizations discussing GLP-1 therapies and metabolic health.

Engagement questions

1) Have you or someone you know navigated insurance decisions around semaglutide or similar therapies? What was the outcome?

2) Should clinicians pursue exception evaluations more proactively to ensure patients with complex metabolic conditions access the full benefits of semaglutide?

Disclaimer: This article provides general information about insurance coverage practices and medical therapies. It is indeed not medical advice. Consult your healthcare provider and insurer for guidance specific to your situation.

Share your experiences or questions in the comments below to join the discussion. For more on semaglutide and metabolic health, you can explore reliable external sources linked here.

FDA: Drug approvals and information • Mayo Clinic: metformin overview

Citing FDA label and clinical trial outcomes (e.g., STEP 1‑5 studies).

Semaglutide Coverage Criteria – Who Gets Insured?

- Medical necessity – Most carriers require a documented diagnosis of obesity (BMI ≥ 30 kg/m²) or BMI ≥ 27 kg/m² with at least one obesity‑related comorbidity (type 2 diabetes, hypertension, dyslipidemia, obstructive sleep apnea, etc.).

- FDA indication – The drug must be prescribed for the weight‑loss indication (e.g., Wegovy®) rather than the diabetes indication (Ozempic®). Some plans treat the two formulations differently.

- Previous therapy – Insurers often demand proof that lifestyle modification, diet counseling, and at least one FDA‑approved anti‑obesity medication (e.g., liraglutide) have been tried and failed.

Key Payers & Their Specific Requirements

| Payer | Typical Coverage Policy | Common Limitations |

|---|---|---|

| Medicare Part D | Covers semaglutide when prescribed for obesity in a “comprehensive obesity management program” approved by the plan’s Pharmacy & Therapeutics (P&T) Committee. | Annual benefit cap (~$4,500); requires prior authorization and documentation of BMI ≥ 30 kg/m². |

| Medicaid (state‑specific) | Coverage varies; 18 + states have adopted the “Obesity Treatment” benefit. | Some states enforce a 12‑month “step‑therapy” rule before semaglutide is approved; prior authorization mandatory. |

| Large Commercial Plans (e.g., UnitedHealthcare, Blue Cross Blue Shield) | Generally cover semaglutide under “weight‑loss drug” tier if a prior authorization package includes BMI, comorbidity list, and a physician‑signed treatment plan. | Tier 3 or 4 co‑pay ($75‑$150 per month); quantity limits of 12 weeks initially, then 24‑week extensions after review. |

| Health Savings Account (HSA) & Flexible Spending Account (FSA) Eligible Plans | Can be reimbursed directly by the employee if the drug is deemed a qualified medical expense. | No insurer limits, but the employee bears full cost until the HSA/FSA funds are tired. |

Prior Authorization Checklist (Step‑by‑Step)

- Patient eligibility form – Include BMI,comorbidities,and previous medication trial details.

- Physician’s prescribing rationale – A concise letter (≤ 300 words) citing FDA label and clinical trial outcomes (e.g., STEP 1‑5 studies).

- weight‑loss program enrollment proof – Documentation of participation in a CDC‑approved lifestyle program (≥ 12 weeks).

- Lab values – Baseline HbA1c, fasting lipids, and serum creatinine (to rule out contraindications).

- Safety checklist – Confirm no history of medullary thyroid carcinoma, multiple endocrine neoplasia type 2, or severe gastrointestinal disease.

Submit the package electronically via the payer’s portal; most insurers respond within 5‑7 business days.

Why Utilization Limits Exist

- Cost containment – Semaglutide’s average wholesale price (AWP) in 2025 was $1,200 per month. Insurers set annual caps to manage pharmacy spend.

- Clinical evidence – Long‑term data beyond 24 months remain limited; payers apply “duration limits” until more robust safety data emerge.

- Risk mitigation – Tiered step‑therapy prevents premature initiation when cheaper, evidence‑based options (e.g.,diet counseling,metformin) may suffice.

Typical Out‑of‑Pocket Scenarios

| Scenario | Expected Cost to Patient |

|---|---|

| Standard commercial plan (Tier 4) | $90–$150 co‑pay per month after deductible. |

| Medicare Part D (after $445 deductible) | 25 % coinsurance → roughly $300/month (subject to annual cap). |

| Medicaid (no co‑pay) | Fully covered after prior authorization; occasionally a $10‑$20 dispensing fee. |

| Self‑pay / cash price | $950–$1,100 per month (discounts may apply via manufacturer patient assistance). |

Practical Tips for Maximizing Coverage

- Align prescription with the proper brand name – “Wegovy” for weight loss, “Ozempic” for diabetes; confusion can trigger denial.

- Document BMI trend – Provide two recent measurements (≥ 3 months apart) to prove persistent obesity.

- Leverage manufacturer assistance programs – The “Weight‑loss Savings Card” offers up to $300 off the first 3 months for eligible patients.

- Appeal strategically – If denied, submit an “peer‑to‑peer” review request with the prescribing endocrinologist’s clinical notes, referencing STEP trial outcomes (e.g., 15 % average weight loss at week 68).

Real‑World Example (2024 Case Study)

- Patient: 42‑year‑old female, BMI = 33 kg/m², hypertension, stage 2 pre‑diabetes.

- intervention: Enrolled in a CDC‑certified 16‑week lifestyle program; trialed liraglutide for 6 months without ≥ 5 % weight loss.

- Outcome: After meeting the prior‑auth checklist, her blue Cross plan approved semaglutide. Over 12 months she achieved a 14 % weight reduction,HbA1c fell from 6.2 % to 5.4 %, and antihypertensive dose was halved.

- Lesson: Comprehensive documentation of failed alternatives and program enrollment dramatically reduced denial risk.

Frequently asked Questions (FAQ)

- Q: Does insurance cover semaglutide for off‑label uses (e.g., PCOS)?

A: Generally no. Coverage is limited to FDA‑approved obesity or type 2 diabetes indications unless a medical necessity exception is granted.

- Q: Can I get a 90‑day supply to lower co‑pays?

A: Most plans restrict initial fills to 30‑day supplies; after 3 months of continuous therapy, a 90‑day refill may be approved subject to prior authorization.

- Q: What happens after the annual benefit cap is reached?

A: Patients either pay the full “cash price” or switch to an choice therapy; some insurers offer a “cap‑exceed” supplemental plan for an additional premium.

- Q: Are pharmacists able to “switch” (i.e., therapeutic interchange) semaglutide to a lower‑cost biosimilar?

A: As of 2025, no FDA‑approved biosimilar for semaglutide exists, so therapeutic interchange is not applicable.

Key Takeaways for Providers

- Prepare a robust prior‑authorization packet that aligns with each payer’s specific criteria.

- Emphasize documented failure of lifestyle measures and prior anti‑obesity agents.

- Monitor patient progress and be ready to submit renewal documentation at the 12‑ and 24‑week marks to avoid interruptions.

Key Takeaways for Patients

- Keep a copy of all BMI records, lab results, and lifestyle program certificates.

- Ask your prescriber to include a concise “medical necessity” statement in the prior‑auth request.

- Explore manufacturer savings cards and state Medicaid programs before opting for self‑pay.