A Southern California couple nearly lost their home down payment to a sophisticated mortgage fraud scheme, highlighting a surge in wire fraud targeting homebuyers. The incident underscores critical vulnerabilities in the real estate closing process and the urgent need for verified communication channels between buyers, escrow agents, and lenders.

What we have is not merely a cautionary tale for a few unlucky buyers; We see a systemic risk indicator. As the U.S. Housing market grapples with elevated mortgage rates and a chronic inventory shortage, the desperation to secure property has created a “trust gap” that bad actors are exploiting with precision. When buyers are rushed, they skip the verification steps that protect their capital.

The Bottom Line

- Liquidity Risk: Wire fraud targets the most liquid moment of a real estate transaction, bypassing traditional banking safeguards via social engineering.

- Regulatory Lag: Current Consumer Financial Protection Bureau (CFPB) guidelines lack mandatory multi-factor authentication for high-value escrow transfers.

- Market Friction: Increased fraud attempts lead to longer closing windows and higher insurance premiums for title companies, adding friction to an already stagnant housing market.

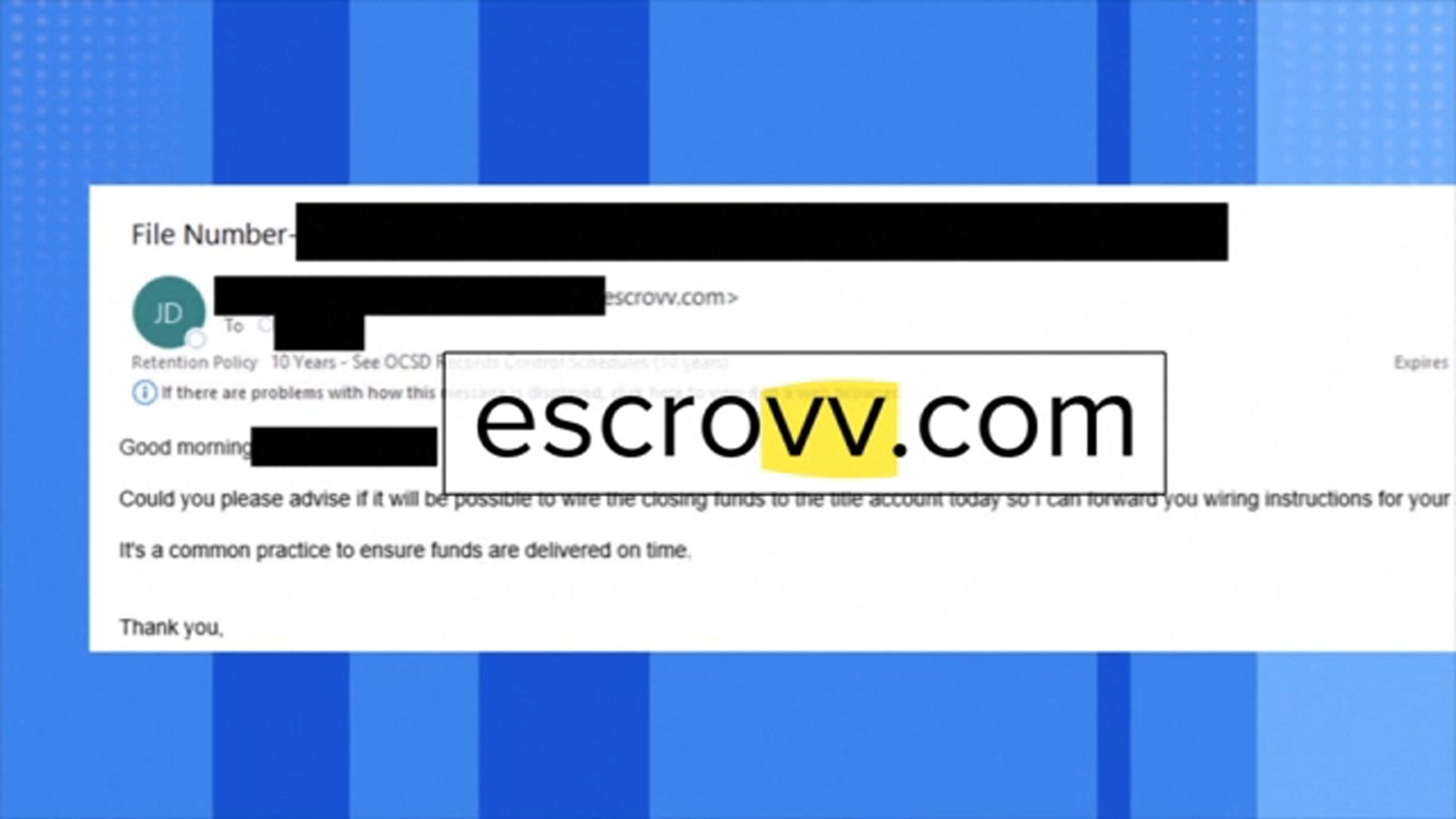

The Anatomy of the Escrow Breach

The fraud typically begins with a “man-in-the-middle” attack. Hackers compromise the email account of a real estate agent or escrow officer. They monitor conversations for the exact moment a closing date is set.

Here is the math: The fraudster sends a spoofed email—identical in branding and tone to the legitimate officer—requesting that the down payment be sent to a “latest” or “updated” account. Because the request arrives in the context of an ongoing, legitimate transaction, the psychological barrier to verification is lowered.

But the balance sheet tells a different story. For the average SoCal homebuyer, a down payment can range from $50,000 to over $200,000. Once a wire transfer is executed to a fraudulent account, the recovery rate is near 0% if the funds are immediately moved into cryptocurrency or offshore accounts.

Macroeconomic Pressure and the Fraud Incentive

Why now? The incentive for mortgage fraud has scaled alongside the volatility of the 10-year Treasury yield. As mortgage rates fluctuated throughout 2025 and into early 2026, the volume of “lock-ins” and rapid-fire bidding wars increased.

High-velocity markets create urgency. Urgency is the primary tool of the social engineer. When a buyer is terrified of losing a property to a cash offer, they are 40% more likely to overlook a slight discrepancy in an email address or a sudden change in wiring instructions.

This trend puts pressure on the operational margins of title insurance giants like First American Financial (NYSE: FAF). As the frequency of these attacks rises, the cost of “Errors and Omissions” (E&O) insurance for agents climbs, which eventually trickles down to the consumer in the form of higher closing costs.

| Risk Factor | Impact on Buyer | Impact on Market Liquidity | Mitigation Cost |

|---|---|---|---|

| Wire Fraud | Total Loss of Principal | High (Transaction Failure) | Moderate (Verification Steps) |

| Interest Rate Volatility | Increased Monthly Cost | Medium (Reduced Demand) | Low (Refinancing) |

| Inventory Shortage | Bidding War Pressure | High (Price Inflation) | N/A |

Systemic Vulnerabilities in Digital Closings

The shift toward “digital closings” was intended to streamline the process, but it has expanded the attack surface. The reliance on email for the transmission of sensitive banking data is a legacy flaw in a modern financial environment.

Institutional investors are noticing the shift. The move toward blockchain-based title registries—where the “tokenization” of a deed ensures a secure, immutable transfer of ownership—is no longer a theoretical exercise; it is a necessity for risk mitigation.

“The reliance on email for the transmission of wire instructions is the single greatest operational vulnerability in the residential real estate sector. Until we move to a cryptographically verified identity system, the human element will remain the weakest link.”

The Federal Bureau of Investigation (FBI) and the Securities and Exchange Commission (SEC) have frequently warned about the rise of “Business Email Compromise” (BEC). In the context of real estate, BEC is not just a corporate headache; it is a catastrophic event for the individual consumer.

How This Impacts the Broader Economy

When a buyer loses a down payment, the ripple effect is immediate. The transaction fails, the seller must return the property to the market, and the local economy loses the immediate stimulus of a home sale and the subsequent “new home” spending spree (furniture, renovations, landscaping).

this creates a chilling effect on consumer confidence. If the process of buying a home—the largest investment most people ever make—is perceived as insecure, buyers may pivot toward the rental market. This shift benefits large-scale institutional landlords like **BlackRock (NYSE: BLK)**, who possess the infrastructure to manage risk at scale, further consolidating residential ownership into corporate hands.

To avoid this, buyers must implement a “zero-trust” protocol. This means never trusting an email for financial instructions. A phone call to a known, verified number is the only acceptable form of verification.

The Trajectory of Real Estate Security

Looking ahead to the remainder of 2026, we expect to see a mandatory shift toward secure portals. The era of sending wire instructions via PDF attachment must conclude. We are moving toward a landscape where the National Association of Realtors (NAR) will likely mandate encrypted communication platforms to maintain professional liability standards.

For the business owner and the investor, the lesson is clear: efficiency cannot approach at the expense of security. The “convenience” of a digital closing is worthless if the capital never reaches the destination.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.