Stamp duty remains the primary financial concern for UK homebuyers, with 30% citing it as a worry, exceeding concerns about rising mortgage rates (11%) and falling house prices (19%). This friction, a year after threshold changes took effect, is impacting transaction volume despite strong buyer confidence, according to a new report from LRG. The average stamp duty bill now stands at £8,552 for standard movers and £3,552 for first-time buyers.

The resurgence of stamp duty as a major obstacle isn’t simply a matter of increased costs. It’s a signal of shifting market psychology. While mortgage rates garnered significant attention in late 2023 and early 2024, the fixed cost of stamp duty is proving to be a more persistent deterrent, particularly as the initial post-pandemic housing boom cools. This is particularly relevant as the Bank of England held rates steady at 5.25% in March 2026, signaling a potential plateau in the rate hike cycle, but not necessarily a reduction in overall housing costs.

The Bottom Line

- Stamp duty is now a greater impediment to home buying than mortgage rate fluctuations, impacting transaction volumes.

- The current stamp duty thresholds, established after the 2022 temporary changes, are disproportionately affecting first-time buyers.

- Government intervention, such as a review of stamp duty thresholds or targeted relief, could stimulate housing market activity.

The Historical Context: A Year Since the Reset

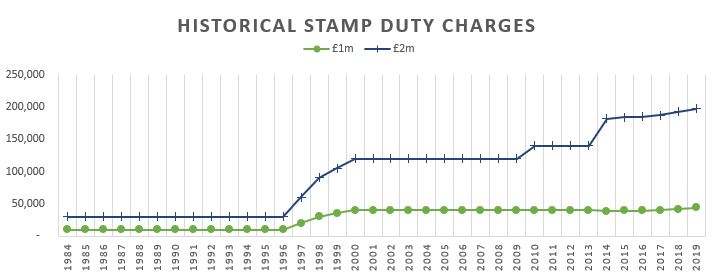

April 1st, 2025, marked the end of the temporary stamp duty thresholds introduced in 2022 during the pandemic. These thresholds, designed to stimulate the housing market, were a significant boon for buyers. The nil-rate band for standard buyers dropped from £250,000 to £125,000 and for first-time buyers, relief fell from £425,000 to £300,000. HM Revenue & Customs data confirmed a surge in transactions in March 2025 as buyers rushed to complete purchases before the changes took effect. HMRC statistics present a 28.4% increase in transactions in March 2025 compared to February 2025.

The Financial Impact: A Deeper Dive into the Numbers

Here is the math. At the current average asking price of £371,042 (as of Rightmove’s March 2026 House Price Index), a standard home mover now faces a stamp duty bill of £8,552. This represents an increase of £2,500 compared to the £6,052 paid under the previous thresholds. For first-time buyers, the impact is even more pronounced. At the same average price, they now pay £3,552 in stamp duty, whereas they would have paid nothing under the pre-April 2025 rules. This effectively adds a significant barrier to entry for those looking to get on the property ladder.

| Buyer Type | Average Property Price (£) | Stamp Duty (Pre-April 2025) (£) | Stamp Duty (Post-April 2025) (£) | Increase (£) | Percentage Increase (%) |

|---|---|---|---|---|---|

| Standard Mover | 371,042 | 6,052 | 8,552 | 2,500 | 41.3% |

| First-Time Buyer | 371,042 | 0 | 3,552 | 3,552 | N/A |

Beyond the Headline: Market-Wide Implications

The impact of stamp duty extends beyond individual homebuyers. It ripples through the entire housing ecosystem. Reduced transaction volumes directly affect revenue for estate agents, conveyancers, and mortgage brokers. It can dampen consumer confidence and slow down economic growth. The property sector contributes approximately 20% to the UK’s GDP, making it a crucial component of the overall economy. The Office for National Statistics provides detailed data on the contribution of the housing sector to the UK economy.

The situation is further complicated by the broader macroeconomic environment. While inflation has cooled from its peak in 2023, it remains above the Bank of England’s 2% target. This, coupled with lingering concerns about global economic uncertainty, is contributing to a cautious outlook among potential homebuyers. The recent performance of **Persimmon (LSE: PSN)** and **Taylor Wimpey (LSE: TW)**, two of the UK’s largest housebuilders, reflects this sentiment. Both companies have reported a slowdown in sales in their latest earnings reports, citing affordability concerns and the impact of higher interest rates and stamp duty.

Expert Perspectives: A Call for Reform

The calls for stamp duty reform are growing louder. Kevin Shaw, national sales managing director at LRG, argues that the tax is “outdated” and “restricts mobility.” But the sentiment isn’t limited to industry insiders.

“Stamp duty is a blunt instrument that disproportionately impacts first-time buyers and those looking to downsize. A more progressive system, perhaps linked to income or property wealth, would be fairer and more efficient.” – Dr. Johnathan Reynolds, Senior Economist, Capital Economics.

Dr. Reynolds’ point highlights a key debate: the fairness and efficiency of the current system. The current structure, based solely on property price, doesn’t account for individual circumstances or ability to pay. This can create significant hardship for those on lower incomes or with limited savings.

The Future Trajectory: What to Expect

Looking ahead, the future of stamp duty remains uncertain. The upcoming Autumn Statement presents an opportunity for the government to address the issue. Potential options include a temporary reduction in stamp duty rates, an increase in the nil-rate band, or a more fundamental reform of the tax system. Although, with the government facing competing fiscal pressures, any significant changes are unlikely in the short term. But the balance sheet tells a different story, with declining transaction numbers potentially forcing a re-evaluation of the tax’s impact on the broader economy. The pressure from industry groups like LRG, coupled with growing public concern, will likely keep the issue on the political agenda. The key will be finding a solution that balances the need for revenue with the desire to stimulate housing market activity and promote homeownership.

The current situation underscores the delicate interplay between fiscal policy, monetary policy, and consumer sentiment in the UK housing market. Navigating this complexity will require a nuanced and pragmatic approach from policymakers.

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*