{kind=link}

Table of Contents

- 1. Navigating the Growing Tide of Credit Card Debt in America: Insights and Solutions

- 2. What factors contribute to the higher per capita credit card debt observed in states like connecticut, Maryland, and New Jersey?

- 3. States Grappling with Credit Card Debt: A Visual Breakdown

- 4. National Credit Card Debt Landscape (2025)

- 5. Top 5 States with Highest Credit Card Debt (Per Capita)

- 6. Visualizing the Debt: A State-by-State Map

- 7. Factors Contributing to Rising Credit Card Debt

- 8. States with the Lowest Credit Card Debt

- 9. The Impact of Interest Rates on Credit Card Debt

- 10. debt Relief Options & Strategies

As the United States grapples with increasing levels of credit card debt, financial experts and advocates are highlighting the need for enhanced consumer protections and greater access to financial education. The persistent rise in household debt poses a significant challenge to individual financial well-being and coudl impact the broader U.S. economy.

Data collected in June 2025 from sources including the U.S. Census Bureau, the Federal Reserve, and TransUnion paints a picture of varying credit card debt burdens across states. While the exact figures are visualized on an accompanying map, the underlying trend underscores a national concern.

In response to the growing burden, financial advocates are pushing for stronger regulations against predatory lending practices and broader financial literacy initiatives, especially in educational settings. States like Oregon and Illinois are already taking legislative action to address these issues, aiming to shield consumers from exploitative practices and equip younger generations with essential financial knowledge.

Financial strategist Sharon Lechter offers practical advice for individuals seeking to manage their credit card debt. She emphasizes the importance of direct interaction with credit card companies to negotiate lower interest rates, noting that a consistent history of on-time payments can increase the likelihood of successful negotiation. Furthermore, lechter advises keeping credit utilization below 30% of the available credit limit. As an example, on a card with a $10,000 limit, reducing the balance to under $3,000 can significantly boost one’s credit score.

Financial Analyst Chip Lupo points out that while median credit card debt provides a snapshot of a state’s financial standing,it’s crucial to also consider the monthly payments made by residents. Low average payments can lead to extended repayment periods and accrue significant interest. He cites Vermont as an example, where a relatively low median debt is coupled with low average monthly payments, contributing to a significant debt problem.Looking ahead to the latter half of 2025,economists caution that unchecked high credit card debt could stifle consumer spending,a vital engine of the U.S. economy. For those feeling overwhelmed by credit card obligations, experts recommend seeking guidance from certified financial advisors and exploring options such as balance transfers, debt consolidation, or debt management plans.

What factors contribute to the higher per capita credit card debt observed in states like connecticut, Maryland, and New Jersey?

States Grappling with Credit Card Debt: A Visual Breakdown

National Credit Card Debt Landscape (2025)

As of mid-2025, American consumers are holding over $1.1 trillion in credit card debt – a figure that continues to climb. But the burden isn’t shared equally. Certain states are facing significantly higher levels of credit card debt than others, driven by factors like cost of living, economic conditions, and consumer spending habits. This article provides a state-by-state visual breakdown, exploring which areas are struggling the most and why. We’ll also cover debt relief options and strategies for managing high credit card balances.

Top 5 States with Highest Credit Card Debt (Per Capita)

Here’s a look at the states currently facing the biggest challenges with consumer credit card debt, based on data analyzed from the Federal Reserve and credit reporting agencies (data as of Q2 2025):

- connecticut: Average debt per capita: $7,850. High cost of living and a concentration of affluent consumers contribute to higher borrowing.

- Maryland: Average debt per capita: $7,620. Similar to Connecticut, Maryland’s economic profile and expenses play a role.

- New Jersey: Average debt per capita: $7,480. Dense population and high property taxes contribute to financial strain.

- Alaska: Average debt per capita: $7,310. Unique economic factors and limited access to affordable goods and services impact debt levels.

- New York: Average debt per capita: $7,250. new York City’s high cost of living is a major driver of credit card debt.

(Data sources: Federal Reserve Economic Data (FRED), Experian, TransUnion, Equifax)

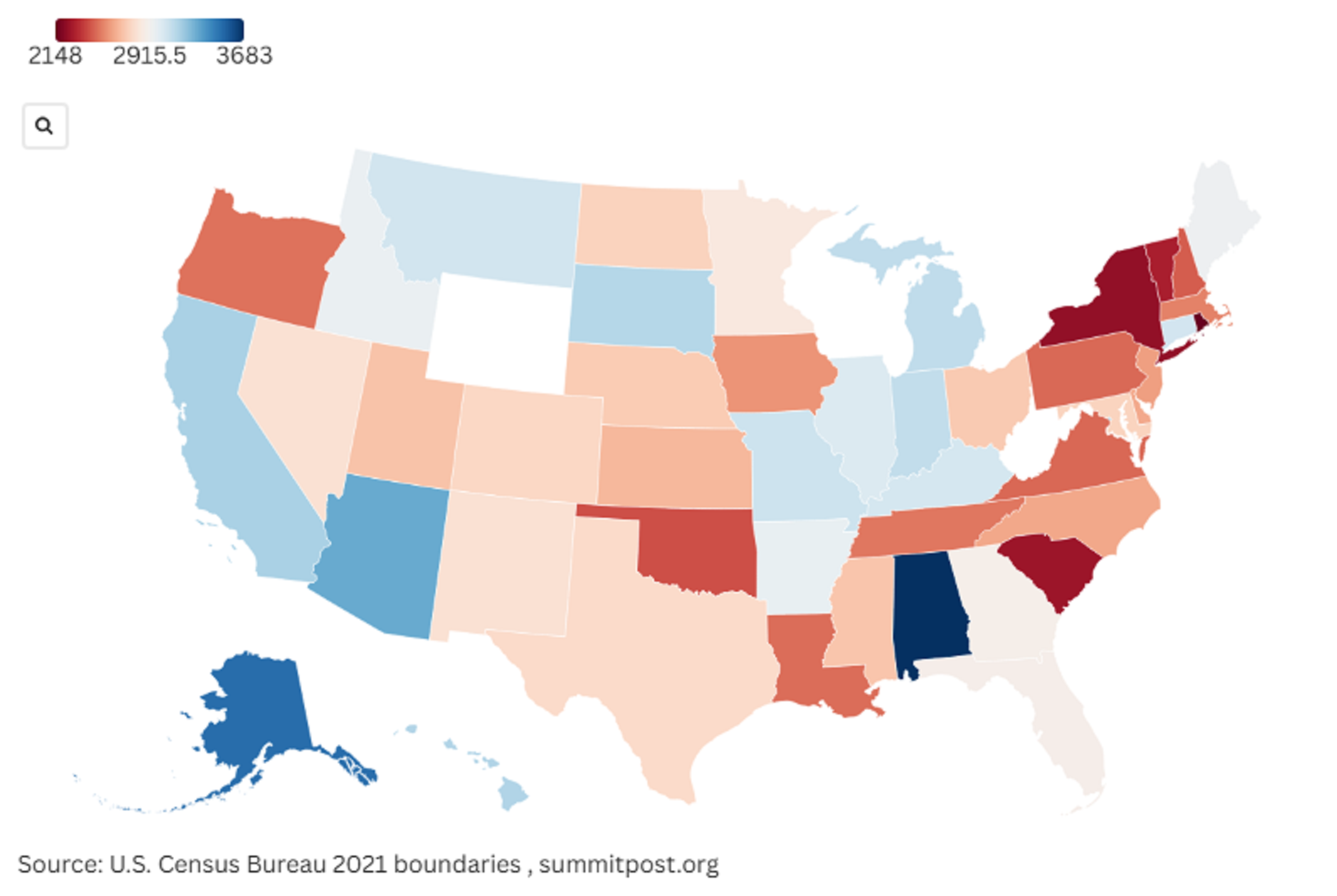

Visualizing the Debt: A State-by-State Map

(Imagine a US map here, color-coded by per capita credit card debt. Darker shades represent higher debt levels. this would be a key visual element for archyde.com)

This map illustrates the geographic distribution of credit card debt. Notice the concentration of higher debt in the Northeast and Mid-Atlantic regions. Southern states generally exhibit lower average debt, though this doesn’t necessarily indicate better financial health – it can also reflect lower average incomes.

Factors Contributing to Rising Credit Card Debt

Several interconnected factors are fueling the increase in credit card balances across the nation:

Inflation: Persistent inflation has increased the cost of essential goods and services, forcing many consumers to rely on credit to cover expenses.

Economic Uncertainty: Concerns about a potential recession and job security lead to increased reliance on credit as a safety net.

lifestyle Creep: As incomes rise (for some),spending frequently enough increases proportionally,leading to higher debt levels.

buy Now, Pay Later (BNPL) Impact: While not technically credit card debt, BNPL services can contribute to overall consumer indebtedness and potentially lead to missed payments on othre obligations.

Reduced Savings Rates: Many Americans have depleted their savings in recent years, leaving them more vulnerable to financial shocks and reliant on credit.

States with the Lowest Credit Card Debt

Conversely, some states are managing credit card debt more effectively. Here are the bottom 5 (per capita):

- Mississippi: Average debt per capita: $4,500

- West Virginia: Average debt per capita: $4,650

- Alabama: average debt per capita: $4,780

- Arkansas: Average debt per capita: $4,820

- South Carolina: Average debt per capita: $4,950

These states generally have lower costs of living and, in some cases, lower average incomes. However, its crucial to note that lower debt doesn’t always equate to financial stability.

The Impact of Interest Rates on Credit Card Debt

Rising interest rates significantly exacerbate the credit card debt problem. The average credit card interest rate in July 2025 is 21.49% (according to Bankrate.com). This means that even small balances can quickly balloon due to accrued interest. States with higher debt levels are especially vulnerable to the impact of these rates. Debt consolidation and balance transfers become increasingly important strategies in this environment.

debt Relief Options & Strategies

For individuals struggling with credit card debt, several options are available:

Balance Transfer Credit Cards: Transferring high-interest debt to a card with a 0% introductory APR can save notable money on interest charges.

Debt Consolidation Loans: Combining multiple debts into a single loan with a lower interest rate can simplify repayment.

Debt Management Plans (DMPs): offered by credit counseling agencies, DMPs involve negotiating with creditors