The Strait of Hormuz is gradually reopening following a period of intense volatility, but global oil markets and shipping lanes face months of instability. This delay stems from Iranian sea-mine warnings, prohibitive insurance premiums and the logistical nightmare of clearing maritime bottlenecks in the world’s most critical energy artery.

If you’ve been watching the headlines this week, you might believe the “all clear” signal is imminent. But as someone who has spent two decades tracking the friction between Tehran and Washington, I can tell you that the physical opening of a waterway is only half the battle. The psychological and financial reopening takes far longer.

Here is why that matters. The Strait of Hormuz isn’t just a stretch of water; it is the jugular vein of the global economy. When it constricts, the world feels it in the price of a gallon of gas in Ohio and the cost of plastic polymers in Shanghai. We aren’t just talking about tankers; we are talking about the fragile trust that sustains global trade.

The Invisible Barrier: Insurance and the ‘War Risk’ Premium

Even with the ships moving again, the “ghost” of the conflict remains in the form of maritime insurance. Underwriters at Lloyd’s of London and other major hubs don’t operate on optimism; they operate on risk. When Iranian authorities warn of sea mines—as we saw in recent alerts—insurance premiums for tankers skyrocket.

But there is a catch. These “War Risk” premiums don’t vanish the moment a ceasefire is signed or a corridor is declared open. They linger until a pattern of safe passage is established over several weeks of uninterrupted transit. For the shipping companies, these costs are passed directly to the consumer, meaning the “flow-on effect” on energy prices is baked in for the next quarter.

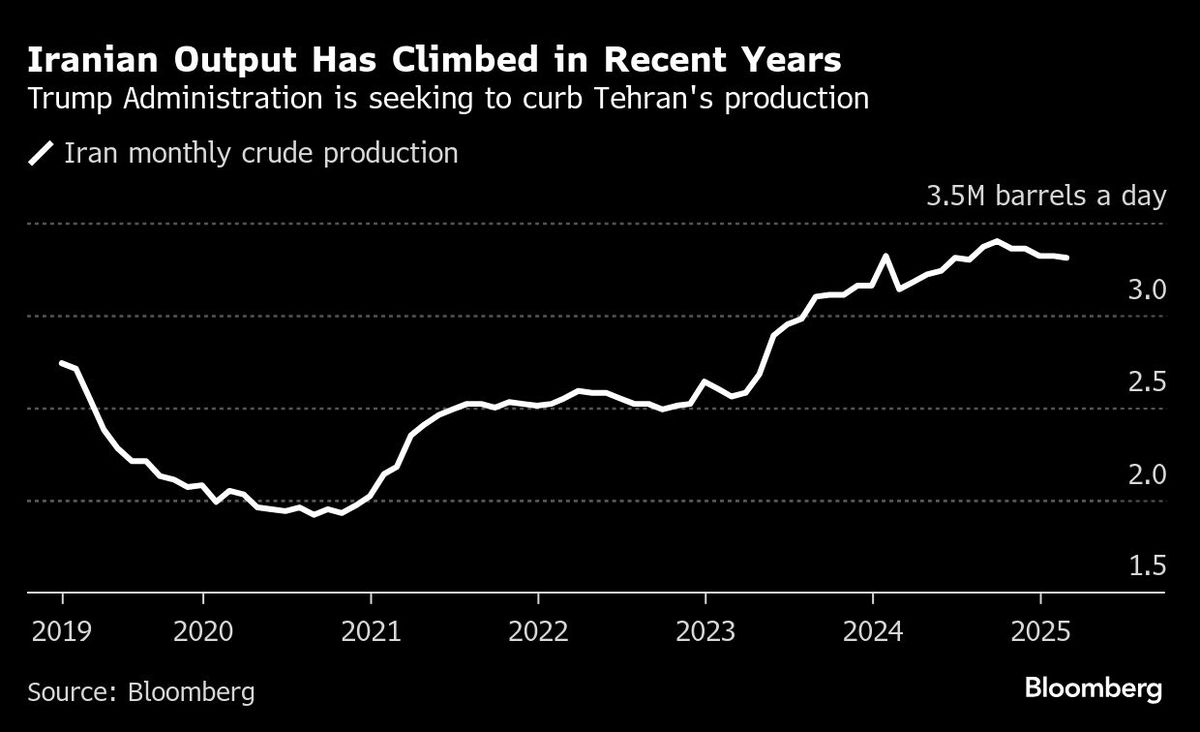

To understand the scale of the vulnerability, consider the sheer volume of energy passing through this chokepoint. Even as Saudi Arabia and the UAE have pipelines to bypass the Strait, they cannot handle the full volume of Persian Gulf exports.

| Metric | Approximate Daily Volume | Global Share | Primary Dependency |

|---|---|---|---|

| Crude Oil Transit | 20-21 Million Barrels | ~20% of Global Consumption | Asia-Pacific Markets |

| LNG Exports (Qatar) | High Volume | Critical for EU/Asia | Energy Transition Stability |

| Alternative Route Capacity | Limited | < 10% of Total Volume | East-West Pipeline (KSA) |

The Geopolitical Chessboard: Leverage and ‘Tolls’

The recent friction regarding “tolls” for ships crossing the Strait—which the Greek Prime Minister recently labeled unacceptable—reveals a deeper struggle for leverage. Iran isn’t just managing a waterway; it is utilizing the Strait as a tool of asymmetric diplomacy. By creating a perception of instability, Tehran gains a seat at the table during negotiations over sanctions and nuclear frameworks.

This represents a classic example of “grey zone” warfare. It is not a full-scale invasion, nor is it total peace. It is a calibrated state of tension designed to exhaust the patience of Western allies and force concessions. When we see warnings about sea mines, it is often a signal to the U.S. Department of State that the cost of maintaining the status quo is rising.

“The Strait of Hormuz is the ultimate geopolitical lever. The ability to threaten the flow of oil allows a regional power to project influence far beyond its military capabilities, effectively holding the global energy market hostage to local political grievances.”

This sentiment is echoed across the halls of the North Atlantic Treaty Organization (NATO), where planners are increasingly concerned about the “interconnectivity of crises.” A skirmish in the Gulf doesn’t stay in the Gulf; it ripples into the Red Sea and affects the stability of the Suez Canal, creating a compounding effect on global supply chains.

Why the Recovery Lag is Structural, Not Just Political

Beyond the politics, there is the brutal reality of maritime logistics. When a major shipping lane is restricted, ships don’t just “wait.” They are rerouted around the Cape of Good Hope or anchored in distant lagoons. This creates a “clustering effect.”

Imagine a highway that has been closed for a week. When it opens, you don’t suddenly have a smooth flow of traffic; you have a massive bottleneck of thousands of cars trying to merge at once. In the shipping world, this means port congestion in Singapore and Jebel Ali, leading to delays in container shipments that have nothing to do with oil.

the “mine threat” mentioned by Iranian authorities creates a lingering operational hazard. Clearing a waterway of mines is a slow, methodical process. Until the International Maritime Organization (IMO) and coalition forces can verify the safety of the deep-water channels, the largest VLCCs (Very Large Crude Carriers) will remain hesitant to enter the most efficient lanes.

The Macro-Economic Ripple: From Crude to Consumer

For the foreign investor, the lesson here is that volatility is the modern baseline. The “flow-on effects” will manifest as a slow bleed of increased costs rather than a sudden spike. We are seeing a shift where energy security is no longer about “having oil,” but about “the reliability of the route.”

This is pushing nations toward an accelerated “de-risking” strategy. We are seeing increased investment in transatlantic pipelines and a faster pivot toward renewables in Europe, not necessarily for the climate, but for national security. The Strait of Hormuz is effectively teaching the world that dependence on a single chokepoint is a strategic liability.

As we move through April, don’t expect a sudden drop in energy prices. Expect a grinding, slow return to normalcy as the insurance markets recalibrate and the shipping bottlenecks clear. The water may be open, but the risk remains submerged.

The bottom line: We are witnessing the transition from a world of “just-in-time” logistics to “just-in-case” security. The question is no longer if the Strait is open, but who controls the key to the gate.

Do you think the West’s reliance on these maritime chokepoints is an outdated strategy, or is the cost of diversifying routes simply too high for the current global economy? Let me know your thoughts in the comments.