Mortgage Market Stagnates Amidst Economic Uncertainty

Table of Contents

- 1. Mortgage Market Stagnates Amidst Economic Uncertainty

- 2. Mortgage Rates Hover

- 3. Demand Destruction Persists

- 4. buyers’ Strike continues

- 5. Supply-Demand Dynamics

- 6. Key Market indicators

- 7. Evergreen Insights for Homebuyers

- 8. Frequently Asked Questions

- 9. How do the Bank of Canada’s interest rate hikes directly impact mortgage affordability for potential homebuyers?

- 10. Surge in Mortgage Rates as Demand Plummets and Supply Surges Amid Economic Freeze: Seeking Lower Prices, Higher Incomes, and Lower Interest Rates

- 11. The Current Mortgage Landscape: A Deep Dive

- 12. Understanding the Rate Hike & Its Impact

- 13. demand Destruction and Inventory Build-Up

- 14. Regional Variations: Where Are We Seeing the Biggest Shifts?

- 15. Strategies for Navigating the Current Market

- 16. For Buyers: Patience and Planning

- 17. For Sellers: Realistic Expectations and Strategic Pricing

- 18. The Role of Government Policy & Economic Indicators

The United States Mortgage Market Is Navigating A Period Of Instability. Recent data indicates that mortgage rates have remained relatively steady, but purchase activity remains subdued. This comes as economic indicators signal mixed signals, causing potential homebuyers to proceed with caution.

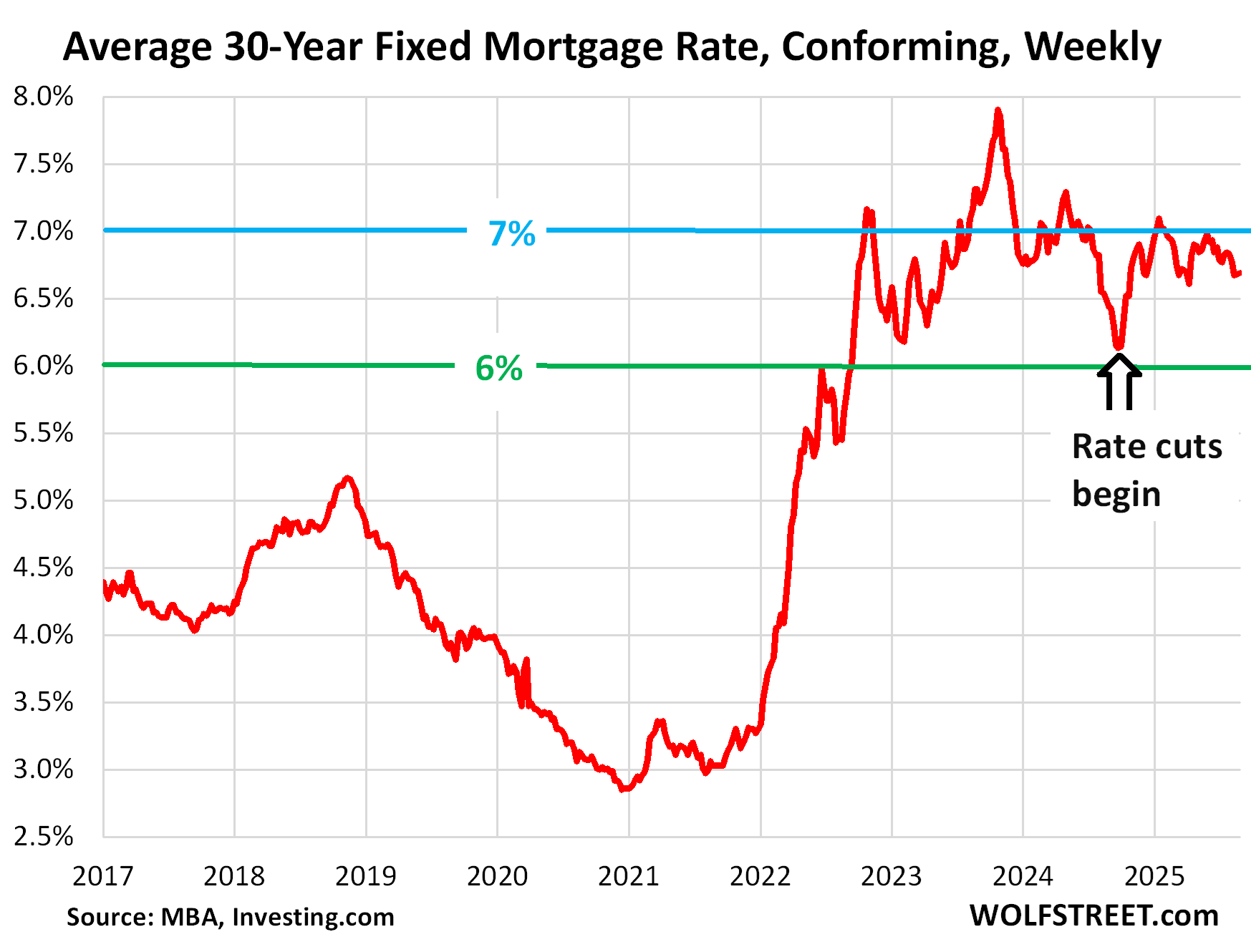

Mortgage Rates Hover

In the latest week, the average 30-year fixed mortgage rate stood at 6.69%. This rate has fluctuated between 6.6% and 7.1% as October of the previous year. This reflects a broader trend of rate stabilization after a period of rapid increases earlier in the year.

The Federal Reserve‘s policy also influences mortgage rates.The market closely watches the actions of the Federal Reserve, with any indications of future rate adjustments sparking considerable interest.

Demand Destruction Persists

Applications for home purchases remain significantly lower compared to pre-pandemic levels. They are down by 30% compared to the same period in 2019. This is due to high home prices and economic uncertainty.

Did You Know? The housing market frequently enough reflects broader economic trends, and is sensitive to changes in interest rates.

Refinancing applications are also down, by 65% compared to 2019.This decrease is mainly due to higher mortgage rates.

buyers’ Strike continues

Many potential homebuyers are waiting for prices to decrease. They are also waiting for their incomes to rise and for interest rates to fall. This wait-and-see approach has been ongoing as mid-2022 and is now completing its third year.

Supply-Demand Dynamics

While demand is soft, the supply has surged. Current data shows the highest supply of condos as the end of the housing bust in 2012.There is also the highest supply of single-family homes since the lockdown in May 2020 and before then since mid-2016.

Pro Tip: Potential buyers should carefully evaluate their financial situation,explore multiple mortgage options,and seek professional advice.

The real estate market is influenced by several factors.

Key Market indicators

| Indicator | Current Status | Trend |

|---|---|---|

| Mortgage Rates | Stable to slightly up | Fluctuating |

| Purchase Applications | Down 30% from 2019 | Low |

| Refinance Applications | down 65% from 2019 | Low |

The convergence of high prices with rising interest rates creates a challenging landscape. This has led to a decline in housing affordability and a reluctance among many potential buyers.

Evergreen Insights for Homebuyers

The housing market is influenced by a number of external factors.

A strategic approach is essential when navigating this market. Staying informed by monitoring economic indicators and consulting with real estate professionals helps future homebuyers.

Investopedia offers resources for those who want to learn more.

Frequently Asked Questions

Q: What is the primary driver of current Mortgage Rates?

A: Economic uncertainty and Fed policies are drivers for current mortgage rates.

Q: How are purchase applications performing?

A: Purchase applications are down compared to 2019.

Q: What is the status of refinancing applications?

A: Refinancing applications are down from 2019.

Q: Why is the housing demand remaining low?

A: high prices and elevated mortgage rates are contributing to suppressed demand.

Q: What actions should potential homebuyers take?

A: They should carefully evaluate their finances.

Q: What is the impact of the buyers’ strike?

A: The buyers’ strike has led to decreased demand.

What are your thoughts on the current housing market trends? Share your opinions in the comments below!

How do the Bank of Canada’s interest rate hikes directly impact mortgage affordability for potential homebuyers?

Surge in Mortgage Rates as Demand Plummets and Supply Surges Amid Economic Freeze: Seeking Lower Prices, Higher Incomes, and Lower Interest Rates

The Current Mortgage Landscape: A Deep Dive

The Canadian housing market is currently experiencing a significant shift. A confluence of factors – rising mortgage rates, dwindling housing demand, and a growing housing supply – has created an “economic freeze” impacting both buyers and sellers. This isn’t simply a correction; it’s a recalibration driven by macroeconomic forces and individual financial pressures. Understanding these dynamics is crucial for anyone involved in the real estate market, whether your a first-time homebuyer, a seasoned investor, or simply monitoring the economy.

Understanding the Rate Hike & Its Impact

The Bank of Canada’s aggressive interest rate hikes, implemented to combat inflation, are the primary driver behind the surge in mortgage interest rates. This has dramatically increased the cost of borrowing, effectively pricing many potential buyers out of the market.

fixed Mortgage Rates: Have climbed substantially,making long-term financial planning more challenging.

Variable Mortgage Rates: While initially attractive, have also risen in tandem with the Bank of Canada’s policy rate, impacting homeowners with variable-rate mortgages.

Stress Test implications: The mortgage stress test, requiring borrowers to qualify at a rate higher than their contracted rate, further restricts access to homeownership.

This increase in rates directly correlates with a decrease in mortgage affordability, a key indicator of housing market health.

demand Destruction and Inventory Build-Up

As mortgage rates have soared,housing demand has plummeted. Potential buyers are delaying purchases, hoping for rates to stabilize or prices to fall. This decreased demand is manifesting in several ways:

Longer Days on Market: Properties are taking significantly longer to sell compared to the frenzied pace of the past few years.

Price Reductions: Sellers are increasingly forced to lower their asking prices to attract buyers. Data from the Canadian Real Estate Association (CREA) shows a growing trend of price adjustments.

Reduced Bidding Wars: The competitive bidding wars that characterized the peak of the market have largely subsided.

Simultaneously,housing supply is increasing. New construction projects are coming online, and some homeowners are choosing to list their properties, anticipating further price declines. This combination of decreased demand and increased supply is creating a buyer’s market in many regions. Cities like Calgary, while still relatively robust, are seeing inventory levels rise. (As evidenced by recent forum discussions on RedFlagDeals regarding mortgages in Calgary for newcomers with limited credit history – see source https://forums.redflagdeals.com/mortgage-2681536/).

Regional Variations: Where Are We Seeing the Biggest Shifts?

The impact of these trends isn’t uniform across Canada. Some regions are experiencing more pronounced declines than others.

Ontario & British Columbia: These provinces,previously the hottest markets,are seeing the most significant price corrections.

Alberta: While more resilient due to its strong economy,Alberta is also experiencing a slowdown,notably in major cities like Calgary.

Atlantic Canada: Markets in Atlantic Canada, which saw rapid growth during the pandemic, are now cooling down.

Prairie Provinces: Saskatchewan and Manitoba are showing more stability, but are still susceptible to the broader economic headwinds.

Given the challenging surroundings, what can buyers and sellers do?

For Buyers: Patience and Planning

Shop Around for Mortgage Rates: Don’t settle for the first rate you’re offered. Work with a mortgage broker to compare rates from multiple lenders.

Improve Your Credit Score: A higher credit score can qualify you for better rates.

Increase Your Down Payment: A larger down payment reduces your loan amount and can lower your monthly payments.

Consider a Pre-Approval: A mortgage pre-approval gives you a clear understanding of how much you can borrow and locks in a rate for a specific period.

Be Prepared to Negotiate: In a buyer’s market, you have more leverage to negotiate the price and terms of the sale.

For Sellers: Realistic Expectations and Strategic Pricing

Price Competitively: overpricing your property will only result in it sitting on the market for an extended period.

Consider Renovations: Minor renovations can increase your property’s appeal and possibly justify a higher price.

work with an Experienced Realtor: A knowledgeable real estate agent can provide valuable insights into the local market and help you navigate the selling process.

Be Flexible: Be prepared to negotiate with buyers and consider offers that might potentially be below your initial asking price.

The Role of Government Policy & Economic Indicators

Government policies and key economic indicators will continue to shape the housing market.

**Bank