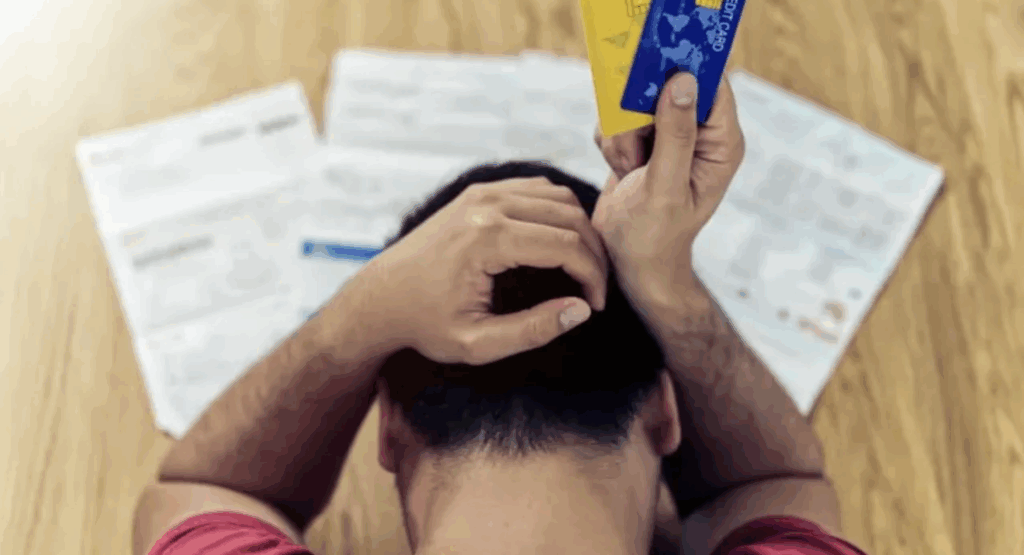

Family Debt Crisis: Why Even High-Income Households Are Struggling – And What’s Coming Next

A staggering 30% increase in family debt in the first half of the year isn’t just a statistic; it’s a flashing warning sign. Across income brackets, from middle-class families to those traditionally considered financially secure, the inability to manage loan payments is skyrocketing. Delinquencies have nearly tripled, signaling a systemic strain that goes beyond isolated financial hardship. This isn’t a temporary blip – it’s a fundamental shift in how households are navigating economic pressures, and understanding the forces at play is crucial for protecting your financial future.

The Perfect Storm: What’s Driving the Debt Surge?

Several converging factors are fueling this unprecedented rise in family debt. Persistent inflation, particularly in essential goods like groceries and energy, is forcing households to rely more heavily on credit to maintain their standard of living. The end of pandemic-era support programs, such as expanded unemployment benefits and stimulus checks, has removed a crucial safety net for many. Furthermore, rising interest rates, implemented to combat inflation, are making existing debt more expensive to service, creating a vicious cycle.

But it’s not just about external pressures. A shift in spending habits, fueled by social media and the “buy now, pay later” (BNPL) phenomenon, is contributing to the problem. BNPL services, while convenient, often encourage impulsive purchases and can lead to overextension of credit. This is particularly concerning as these services aren’t always reported to credit bureaus, masking the true extent of a household’s financial obligations.

Delinquency Rates: A Canary in the Coal Mine

The dramatic increase in loan delinquencies is perhaps the most alarming indicator of the growing crisis. Traditionally, delinquencies would rise primarily among lower-income households. However, recent data shows a significant uptick in missed payments among higher earners, even those using credit cards. This suggests that even financially stable families are struggling to cope with the combined pressures of inflation and rising interest rates. This trend is particularly worrying because it indicates a broader economic vulnerability than previously anticipated.

Beyond the Numbers: The Psychological Impact of Debt

The consequences of mounting debt extend far beyond financial strain. Studies have consistently shown a strong correlation between financial stress and mental health issues, including anxiety, depression, and even suicidal ideation. The constant worry about making ends meet can erode relationships, impact work performance, and create a pervasive sense of hopelessness. Ignoring the psychological toll of personal debt is a critical oversight.

Future Trends: What to Expect in the Coming Months

Experts predict that the current trend of rising debt and delinquencies is likely to continue, at least in the short term. While inflation may eventually moderate, interest rates are expected to remain elevated for some time, continuing to squeeze household budgets. The potential for a recession further complicates the outlook, as job losses would exacerbate the debt crisis. We can also anticipate increased scrutiny of BNPL services and potential regulatory changes to address their risks.

A key trend to watch is the potential for a “debt hangover” – a prolonged period of reduced consumer spending as households prioritize debt repayment over discretionary purchases. This could have significant implications for economic growth. Furthermore, the increasing prevalence of credit card debt, particularly among higher-income earners, suggests a shift in financial behavior that may be difficult to reverse.

The Rise of “Financial Fatigue”

A less-discussed but increasingly relevant factor is what some experts are calling “financial fatigue.” After years of economic uncertainty – the pandemic, inflation, and now the threat of recession – many individuals are simply exhausted by the constant need to manage and adjust their finances. This fatigue can lead to apathy and poor financial decision-making, further exacerbating the debt problem. Understanding this psychological element is crucial for developing effective solutions.

Protecting Your Financial Wellbeing: Actionable Steps

While the situation is concerning, there are steps individuals can take to mitigate the risks. Prioritize creating a realistic budget and tracking expenses. Focus on paying down high-interest debt, such as credit cards, as quickly as possible. Explore options for debt consolidation or balance transfers. And, importantly, seek professional financial advice if you’re struggling to manage your debt. Resources like the National Foundation for Credit Counseling offer valuable support and guidance.

The current debt crisis is a complex issue with far-reaching consequences. It’s a wake-up call for individuals, policymakers, and financial institutions alike. Proactive planning, responsible borrowing, and a focus on financial wellbeing are essential for navigating these challenging times and building a more secure future.

What are your biggest concerns about rising family debt? Share your thoughts and strategies in the comments below!