2023-05-04 15:51:00

The European Central Bank (ECB) decided this Thursday to raise key interest rates by 25 basis points, a slowdown compared to previous increases. However, it remains an aggravation and a signal for the markets. What is the cost to households and businesses? Have the Euribor already incorporated this increase? What are the ECB’s criteria for making decisions? Wasn’t Inflation slowing down? These and other questions answered concisely.

1683218790

#interest #rates #inflation

1. Increase exposure to longer duration assets

2022 has been a difficult year for all credit markets, given the inflationary pressures and resulting interest rate hikes. Assets with longer duration were sold off in particular. However, rates markets have rallied over the past three months and the forward rate curve is no longer trending up as future rate movements are priced in; we might see the end of central bank rate hikes by the middle of the year.

Given the improving rate environment, we believe there are growing short-term opportunities in longer duration (around 8-10 years) and higher quality (investment grade rated) credits. which tend to exhibit lower volatility and maintain their relationship to returns. We believe that this sub-section of corporate credit is likely to rebound in correlation with the fall in rates.

Graph. 1 – The market indicates that the Fed is near the end of the rate hike cycle.

- Source: Bloomberg as of January 23, 2023. For illustrative purposes only, not to be construed as investment advice

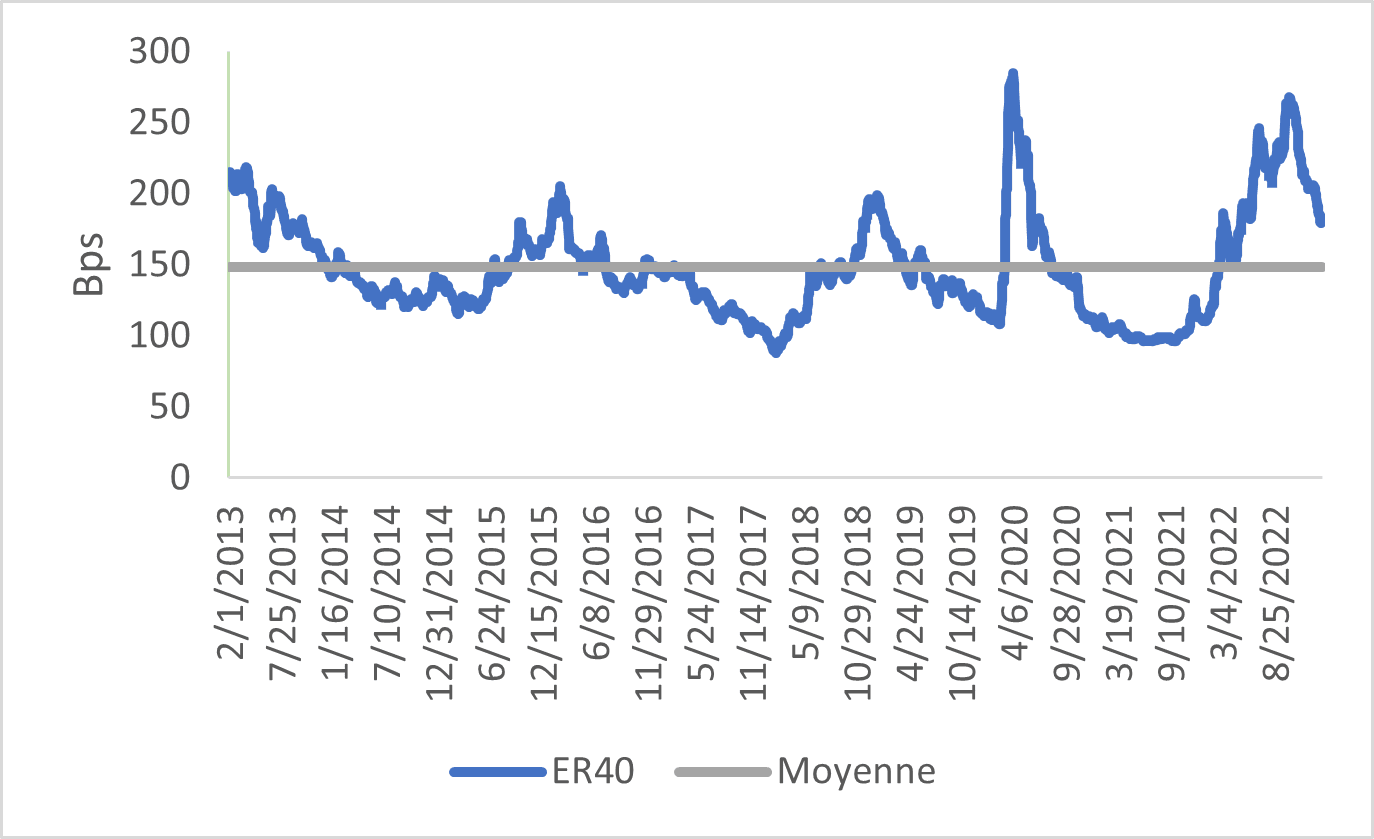

2. Opportunities in short duration high yield securities

Given the large swings in yields on the front end of the curve, we also see opportunities in higher yielding, short duration assets. Bonds of the BBB and BB categories have a very attractive yield per unit of duration. Due to the relatively flat yield curves, investors are compensated for taking the same level of risk in both short and long duration assets.

Graph. 2 – Short-duration investment grade yields look attractive

- Source: ICE Data Platform, as of January 31, 2022. ICE BofA Global Corporate Index (G0BC). For illustrative purposes only, not to be construed as investment advice.

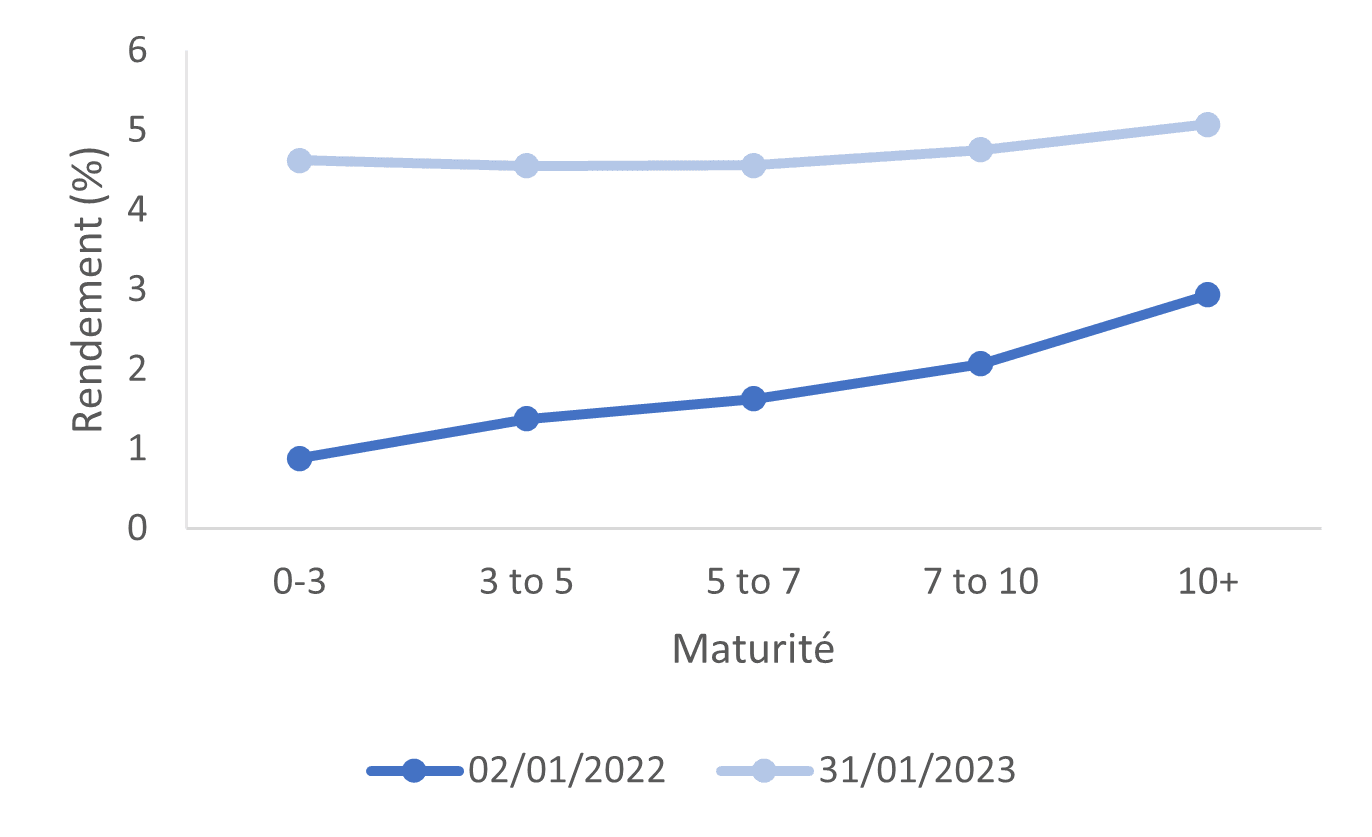

3. European credit

European and euro-denominated assets were hit hard by Russia’s invasion of Ukraine last year. However, we now see value in Euro assets and have increased our exposure in the shorter duration BBB segment. We also see value in European financials, both for senior bonds and subordinated debt (lower tier 2) because European banks are in good financial health in our view; they are backed by the European Central Bank and their securities have been significantly revalued, particularly in the subordinated segment where yields are very attractive.

Graph. 3 – European BBBs are approaching the 10-year average

- Source: ICE Data Platform, as of January 31, 2022. ICE BofA Global Corporate Index (G0BC). For illustrative purposes only, not to be construed as investment advice.

Conclusion

Multi-asset credit strategies can navigate between different credit asset subclasses, ratings and regions to find the most attractive valuations while reducing risk exposure during times of heightened volatility. Although valuations have tightened considerably in recent months, we remain constructive on credit.

Former Niti Aayog Vice Chairman Rajiv Kumar on Thursday said the Budget should have focused more on asset monetisation and privatisation, besides allocating more funds to the social sector schemes. Finance Mininster Nirmala Sitharaman presented the Union Budget 2023-24 in the Lok Sabha on February 1.

Participating in a discussion on ‘Union Budget 2023 and Beyond’ organised by Ananta Centre, Kumar said, “there should be (have been) a lot more focus on privatisation and asset monetisation, which I do not find reference to here (Budget)”.

He also said Rs 51,000 crore disinvestment target is way too low.

“And in some sense, I feel that the space for private investment, actually has been shrinking in the economy. And I think that’s something which can also be seen in the fact that we brought the commercial bank credit growth in double digits finally, but the commercial bank credit to industry is still in the very mid single digits, hardly any demand for credit at all,” he said.

He suggested that funds raised through asset monetisation should be used to retire public debt.

For the next fiscal 2023-24, the Budget has pegged disinvestment revenue at Rs 51,000 crore.

The government has also scaled down the disinvestment target for the current fiscal to Rs 50,000 crore, from Rs 65,000 crore budgeted last year. Further, regarding Rs 10,000 crore is expected to come from monetisation of government assets in the current year and well as in the next fiscal.

Expressing his views on the Budget during the discussion, Naushad Forbes, Chairman of Ananta Aspen Centre and Co-Chairman of Forbes Marshall, said the Budget is for India growing at 5, 6 or even 7 per cent.

“So having a budget that did no bad is a good thing. And it is an achievement and something that we should appreciate,” Forbes said.

According to him, the Budget talks regarding fiscal consolidation, shifts towards capex in spending, and continues transparency on bringing more and more expenditure items into the budget and not leaving them off budget.

Credit Suisse AG will face a capital shortfall of 8 billion Swiss francs ($8 billion) in 2024, according to Goldman Sachs, further evidence of the Swiss bank’s problems, Goldman Sachs analysts told Bloomberg. .

Analysts led by Chris Hallam have estimated the gap of at least CHF4 billion, and he says the equity increase would be “prudent”, given the need to restructure investment banking operations at a time of minimal capital generation.

Speculation regarding the position of the Swiss bank in terms of capital and liquidity levels has affected the stability of its shares this year, leading to calls from some analysts to increase the shares.

Chief Executive Ulrich Koerner is set to detail the bank’s second strategic overhaul in a year on October 27, which is generally seen as a critical opportunity to restore confidence in the bank following more than a year of losses and management errors.

Flora Pocahut, an analyst at Jefferies, clarified Goldman’s comments, stating in a note on Tuesday that Credit Suisse needs to generate regarding CHF9 billion of capital within two to three years. Given the dilutive nature of the capital increase, Pocahontas expects Credit Suisse to prioritize the disposal of assets.