Table of Contents

- 1. Diner Finds Unauthorized Tip Added to Credit Card Bill

- 2. Swift Resolution Through Bank Dispute

- 3. Declining Tipping Trends in the U.S.

- 4. Protecting Yourself from unexpected charges

- 5. The Rise of Service Fees and Their Impact

- 6. frequently Asked Questions About Credit Card Disputes

- 7. What factors might lead a customer to intentionally leave a $0 tip while simultaneously arranging a separate, larger form of financial assistance for a server?

- 8. Unexpected Generosity: Woman Leaves $0 Tip, but Bank Statement Reveals Surprising Gesture

- 9. The Initial Shock: A Zero-Dollar Tip

- 10. The Bank Statement Revelation: A $10,000 Deposit

- 11. Why Bypass the Customary Tip? Understanding the Limitations

- 12. The Impact of Generosity: Beyond the Financial Benefit

- 13. Real-World Examples of Extraordinary Tips

- 14. Practical Tips for Showing Server Appreciation

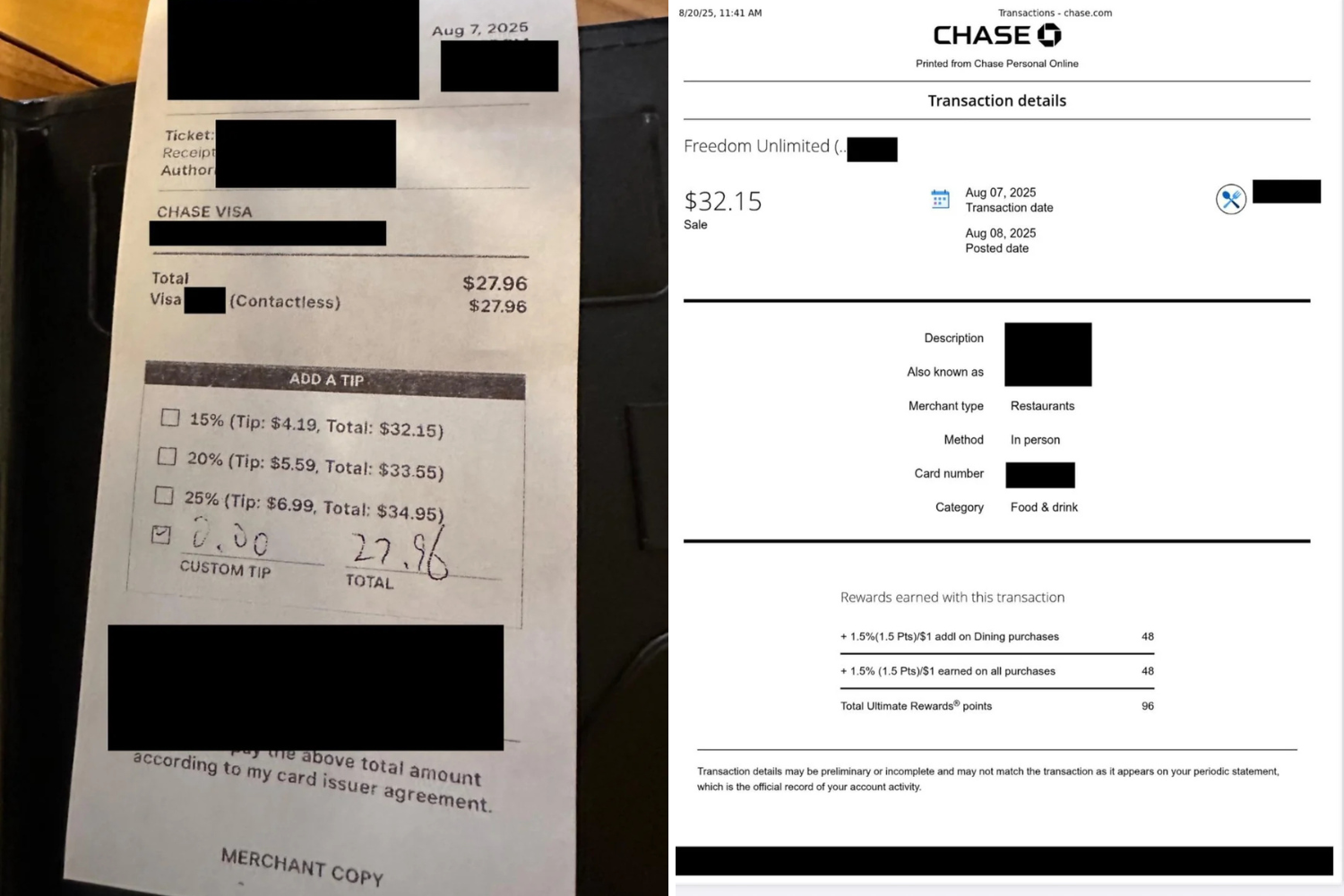

A woman, identified as Alice, was surprised to discover an extra $4.19 had been charged to her credit card after a recent restaurant visit. The total bill originally amounted to $27.96,but her credit card statement reflected a charge of $32.15, effectively adding a 15 percent tip without her explicit consent.

Alice noticed the discrepancy when her credit card statement arrived the following day. She immediately shared her experience on the Reddit forum r/EndTipping, prompting widespread discussion and concern among users. She stated she promptly filed a dispute with her bank and also contacted the restaurant through its website.

Swift Resolution Through Bank Dispute

Fortunately, Alice’s bank, Chase, swiftly addressed the situation. Within minutes, she received confirmation that the disputed $4.19 had been credited back to her account. Chase’s email stated the credit would fully post to her account within 24 to 48 hours, and no further action was needed from her.

“I feel very happy that this got so much attention and people responded positively,” Alice remarked, expressing relief at the speedy resolution and the support she received online.

Declining Tipping Trends in the U.S.

This incident comes amid a broader trend of declining tipping rates across the united states.Recent data from restaurant software company Toast indicates a subtle but noticeable decrease in average tips. In the first quarter of 2024, average tips at sit-down restaurants fell to 19.3 percent,down from 19.4 percent in the previous quarter.

Quick-service restaurants also saw a slight dip, with tips decreasing from 16 percent to 15.9 percent during the same period. A 2023 Bankrate survey revealed generational differences in tipping habits, with Gen Z being least likely to leave a tip compared to older generations.

| Generation | Percentage Who Always Tip at Sit-Down Restaurants |

|---|---|

| Gen Z (1997-2012) | 35% |

| Baby Boomers | 83% |

Protecting Yourself from unexpected charges

Experts recommend several steps to safeguard against unauthorized charges on your credit card when dining out. These include carefully reviewing your receipt before signing, promptly checking your online statement for any discrepancies, and immediately disputing any incorrect charges with your bank.

Did You Know? Under the Fair Credit Billing Act, consumers generally have 60 days to dispute charges on thier credit card statements.

“Always double-check your receipt and your credit card statement,” Alice advised. “Even small charges matter.”

The Rise of Service Fees and Their Impact

The conversation around tipping is evolving, with more restaurants exploring alternative compensation models like service fees. While intended to provide stable wages for staff, these fees can sometimes lead to confusion and disputes if not clearly disclosed. Consumers should be aware of all charges on their bill, including service fees, taxes, and gratuity, to ensure clarity and avoid unexpected costs.

Additionally, the increasing use of digital payment methods, while convenient, requires heightened vigilance. Regularly monitoring your online bank and credit card statements is crucial for identifying and addressing any fraudulent activity promptly.

Do you think restaurants should move away from the conventional tipping model? what steps do you take to ensure accuracy when paying for meals?

frequently Asked Questions About Credit Card Disputes

- What is a credit card dispute? A credit card dispute is a process where you challenge a charge on your credit card statement that you believe is incorrect or fraudulent.

- How long do I have to dispute a charge? Typically, you have 60 days from the date of the statement containing the charge to file a dispute.

- What information do I need to dispute a charge? You’ll generally need your account number, the date and amount of the charge, and a clear explanation of why you’re disputing it.

- What happens after I dispute a charge? The bank will investigate the claim, and you might potentially be asked to provide supporting documentation.

- What if my dispute is denied? You may have the option to appeal the decision or pursue other legal remedies.

- How can I avoid credit card disputes? Always review your receipts and statements carefully,and be cautious when using your card at unfamiliar establishments.

- What are my rights regarding unauthorized credit card charges? the Fair Credit Billing Act protects consumers from unauthorized charges and provides a clear process for disputing them.

Share this article with friends and family to help them protect themselves from potential credit card fraud. leave a comment below to share your experiences and thoughts on this crucial issue.

What factors might lead a customer to intentionally leave a $0 tip while simultaneously arranging a separate, larger form of financial assistance for a server?

Unexpected Generosity: Woman Leaves $0 Tip, but Bank Statement Reveals Surprising Gesture

The Initial Shock: A Zero-Dollar Tip

The restaurant industry operates on a delicate balance, with tipping frequently enough forming a significant portion of a server’s income. So, when a server at a diner in Kansas City, Missouri, received a bill with a $0 tip, it understandably felt disheartening. The customer, identified as Sarah Weaver, had dined with her family and left without any additional gratuity on a $60 bill. While not uncommon, a zero-dollar tip often signals dissatisfaction or financial hardship. Though, this story took an unexpected turn, revealing a remarkable act of kindness hidden beneath the surface. The initial reaction, naturally, was disappointment – a common sentiment among service staff relying on restaurant tips for their livelihood.

The Bank Statement Revelation: A $10,000 Deposit

Days later, the server, identified only as “Alex,” checked the restaurant’s online tip-sharing platform. To their astonishment, a $10,000 deposit had been made, with the note: “Tip for Alex. You deserve it.” The server was stunned.It quickly became clear that Sarah Weaver’s $0 tip wasn’t a reflection of her service, but a deliberate act to bypass the platform’s limitations.

The online platform capped tips at a certain amount, which Weaver’s intended generosity far exceeded.

She opted to deliver the substantial tip directly thru a bank transfer, ensuring the full amount reached Alex.

This highlights a growing trend of customers seeking alternative ways to show gratitude, especially for exceptional service.

This story quickly went viral, sparking conversations about generous tipping, server gratitude, and the challenges of tip sharing apps.

Why Bypass the Customary Tip? Understanding the Limitations

Several factors can lead customers to bypass traditional tipping methods. These include:

Tip Caps: Many point-of-sale (POS) systems and digital tipping platforms impose limits on the maximum tip amount.

Fee Structures: Some platforms charge fees that reduce the amount received by the server.

Direct Connection: Customers may prefer a direct method to ensure the full amount reaches the intended recipient, fostering a stronger sense of customer appreciation.

Cashless Society: The increasing prevalence of cashless payments encourages alternative methods for larger gratuities.

The Impact of Generosity: Beyond the Financial Benefit

The $10,000 tip had a profound impact on Alex’s life. The server, a single parent, planned to use the money to pay off debt and secure a more stable future.This act of kindness underscores the power of random acts of kindness and the positive ripple effect they can create.

The story resonated with many, highlighting the financial struggles faced by service industry workers.

It prompted discussions about fair wages and the importance of supporting those who rely on tips.

The incident also served as a reminder that appearances can be deceiving, and a seemingly negative gesture can conceal a generous heart.

Real-World Examples of Extraordinary Tips

while Alex’s story is exceptional, it’s not isolated. Here are a few other examples of remarkable generosity:

- 2019, Michigan: A customer left a $10,000 tip on a $23 bill, specifically to help a waitress pay for her mother’s cancer treatment.

- 2020, Pennsylvania: A group of diners left a $4,800 tip during the height of the COVID-19 pandemic to support a struggling restaurant and its staff.

- 2021, Florida: A customer tipped a server $5,000 after learning about their aspirations to become a chef.

These instances demonstrate a growing trend of customers going above and beyond to express their gratitude and support service industry workers.

Practical Tips for Showing Server Appreciation

Beyond large sums, there are numerous ways to show appreciation for your server:

Leave a thoughtful note: A few kind words can brighten their day.

Be patient and understanding: Servers frequently enough handle multiple tables and can be under pressure.

Request them by name: If you receive exceptional service, ask to be seated in their section again.

Consider leaving a generous tip, even if it’s not a large amount: Every little bit helps.

* Advocate for fair wages: Support policies that improve the working conditions