Thailand aims for carbon neutrality by 2050, balancing energy security, affordability and sustainability. This transition impacts global supply chains, particularly in automotive and electronics, as investors seek stable, green manufacturing hubs amidst rising regional demand.

As an Editor-in-Chief who has tracked resource wars from the Caspian to the South China Sea, I witness Bangkok’s power struggle not just as domestic policy, but as a bellwether for emerging market stability. The Kingdom stands at a precipice. On one side lies the promise of a green economy. on the other, the risk of blackouts that could stall global production lines. Here is why that matters to you, regardless of where you sit.

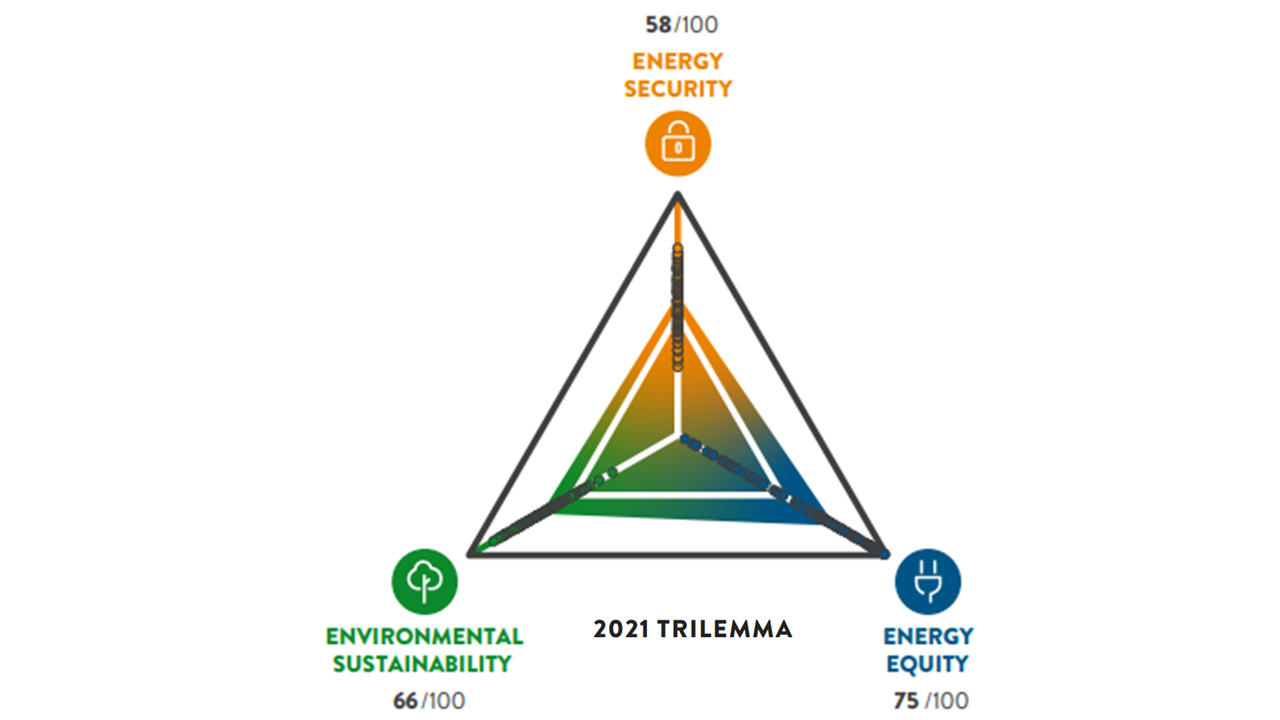

The Trilemma in the Tropics

Walk through the industrial estates of Rayong late on a Tuesday evening, and you will hear the hum of machinery that powers much of the world’s pickup truck and hard drive supply. But beneath that hum lies a tension known to energy insiders as the trilemma. Thailand must secure energy supply, keep it affordable for manufacturers, and decarbonize simultaneously. It’s a juggling act where dropping one ball risks dropping them all.

The government’s Long-Term Low Greenhouse Gas Emission Development Strategy (LT-LEDS) sets the stage, but the script is being rewritten by market forces. Natural gas, long the backbone of Thai power, is becoming increasingly volatile due to geopolitical shifts in the Gulf and domestic depletion. IEA Southeast Asia Energy Outlook data suggests the region must triple renewable capacity to meet climate goals. But there is a catch.

Intermittency remains the ghost in the machine. Solar peaks at noon, but factories run 24 hours. Without massive battery storage or regional grid interconnection, the lights flicker. And in the high-stakes world of semiconductor manufacturing, a flicker is a disaster.

Supply Chains Hang in the Balance

Consider the automotive sector. Thailand is often called the Detroit of Asia. Major multinational corporations have anchored their EV transition strategies here. Even though, an unstable grid threatens the “green” credential of every vehicle exported to Europe or North America. If the electricity used to charge these cars comes from coal or unstable gas peakers, the carbon tariff penalties under mechanisms like the EU’s CBAM could erase profit margins.

This is where the geopolitical lens sharpens. Investors are no longer just looking at labor costs; they are auditing power purchase agreements. A shift in Thailand’s energy mix directly influences foreign direct investment flows across ASEAN. If Bangkok falters, capital flows to Vietnam or Indonesia. If it succeeds, it cements its role as the logistical heart of Southeast Asia.

We are seeing a divergence in investor sentiment. Some are hedging bets with onsite solar, while others demand grid guarantees. The ASEAN Centre for Energy has highlighted the need for derisking instruments to bridge this gap. Without them, the transition stalls.

Financing the Green Leap

Money is the oxygen of this transition. The capital expenditure required to overhaul Thailand’s generation fleet is staggering. Public funds alone cannot cover it. This necessitates a robust framework for private investment, yet regulatory uncertainty often spooks institutional capital.

Dr. Nuki Agya Utama, Executive Director of the ASEAN Centre for Energy, has previously noted the critical nature of financing mechanisms in the region. In recent discussions regarding ASEAN’s transition, the sentiment remains clear:

“Financing remains the biggest challenge for the energy transition in Southeast Asia. We need to unlock private capital through innovative instruments that share the risk between public and private sectors.”

This quote underscores the bottleneck. It is not a lack of technology, but a lack of financial architecture. The World Bank Energy Program continues to emphasize that emerging markets require tailored solutions, not one-size-fits-all mandates. Thailand’s ability to structure these deals will set a precedent for the rest of the developing world.

To visualize the scale of the challenge, consider the projected shifts in the country’s power generation mix. The following data illustrates the ambitious targets set against the reality of current infrastructure.

| Energy Source | 2023 Estimate (%) | 2037 Target (PDP Rev 1) | Strategic Implication |

|---|---|---|---|

| Natural Gas | 53% | 32% | Reduced reliance enhances security but requires import diversification. |

| Renewables | 21% | 38% | Requires massive grid modernization and storage investment. |

| Coal/Lignite | 13% | 11% | Slow phase-out balances affordability with carbon goals. |

| Imports | 13% | 19% | Increased regional interconnection boosts stability but adds dependency. |

These numbers tell a story of gradual evolution rather than revolution. The shift away from natural gas is significant, yet the reliance on imports highlights a vulnerability. Energy security is no longer just about domestic reserves; it is about diplomatic relationships with neighbors who supply power.

The Human Cost of Transition

Behind the megawatts and investment treaties are people. A just transition means ensuring that workers in traditional energy sectors are not left behind. As Thailand pivots, communities reliant on gas plants or coal mining face economic uncertainty. Thailand Business News reports often highlight the social license required for latest renewable projects, which can face local opposition if not managed with transparency.

Here is the reality: A green grid that alienates the populace is unsustainable. Policy makers must balance the macroeconomic gains with microeconomic pain. This involves retraining programs, social safety nets, and community engagement that goes beyond box-ticking.

The path to 2050 is not a straight line. It is a negotiation between technology, capital, and society. Thailand’s journey offers a blueprint for the Global South. If they navigate the trilemma successfully, they prove that development and decarbonization can coexist. If they stumble, the ripple effects will be felt in boardrooms from Detroit to Frankfurt.

As we move through this week, keep an eye on the regulatory announcements coming out of Bangkok. They will signal whether the Kingdom is ready to lead the region’s energy future or merely follow it. The world is watching, and the clock is ticking.